Why choose enhanced HMO options for SMEs: 47% ROI

TL;DR:

- Enhanced HMO plans offer broader coverage and higher benefit limits than basic or PhilHealth options.

- Offering enhanced HMOs improves employee retention, reduces absenteeism, and boosts productivity.

- Once granted, HMO benefits are protected by Philippine law and cannot be reduced without employee consent.

Many SME owners in the Philippines assume that if employees have PhilHealth and a basic HMO card, they are covered. That assumption costs companies more than they realize. The Philippine HMO market is expanding fast, with revenue hitting PHP 73.12 billion in 2025, and the plans within it are not created equal. Enhanced HMO options go far beyond the basics, and for SMEs competing for skilled workers in tech, hospitality, and healthcare, the difference between a standard plan and an enhanced one can directly shape your ability to hire, retain, and grow your team.

Table of Contents

- What are enhanced HMO options for SMEs?

- How enhanced HMO options compare to PhilHealth and basic HMO plans

- Key business benefits: Talent attraction, productivity, and ROI

- What to know before choosing: Mechanics, limits, and compliance

- Why enhanced HMO is more than an upgrade: A hard-won SME perspective

- Explore better HMO options for your SME

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Enhanced HMO means more | Enhanced HMO plans cover more services and people than basic or PhilHealth, including outpatient, mental health, and dependents. |

| Boost talent and ROI | Investing in enhanced HMO options leads to higher retention, productivity, and measurable returns for SMEs. |

| Layering adds value | Enhanced HMOs work best alongside PhilHealth for comprehensive protection at lower out-of-pocket expense. |

| Mind compliance risks | Once you provide enhanced HMO, Philippine labor law protects these benefits so careful planning is key. |

| Choose plans smartly | Evaluate plan tiers, eligibility, and digital claim features before deciding on the right enhanced HMO for your employees. |

What are enhanced HMO options for SMEs?

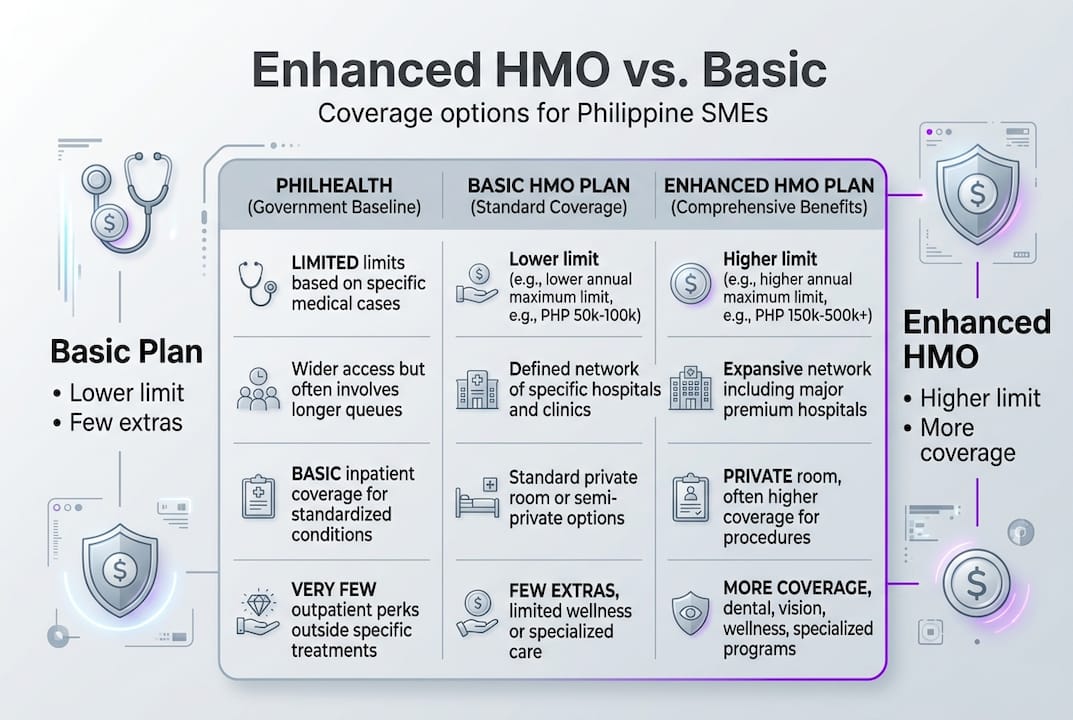

Not all HMO cards open the same doors. A basic plan might cover emergency room visits and a few outpatient consultations per year. An enhanced HMO plan is built on a fundamentally different logic: higher maximum benefit limits (MBL), a wider network of specialists, and coverage categories that standard plans simply exclude.

Enhanced HMO options for SMEs in the Philippines typically include a combination of the following:

- Outpatient and inpatient care with higher annual limits

- Preventive care, including annual physical exams

- Dental coverage as a built-in or modular add-on

- Mental health support, including counseling sessions

- Dependent coverage for spouses and children

- Specialist consultations with reduced or zero copay

Providers like MaxicarePlus offer tiered SME programs where enhanced HMO benefits include broader outpatient, inpatient, preventive care, dental, mental health, and dependent support compared to standard or basic plans. These tiers allow SMEs to match plan depth to their budget and workforce profile.

Here is a simplified look at how enhanced tiers differ from basic plans:

| Feature | Basic HMO plan | Enhanced HMO plan |

|---|---|---|

| Maximum benefit limit | PHP 50,000–100,000 | PHP 150,000–500,000+ |

| Outpatient visits | 3–5 per year | Unlimited or higher cap |

| Dental coverage | Not included | Optional or included |

| Mental health sessions | Not included | Included |

| Dependent coverage | Not standard | Available as add-on |

| Preventive care | Minimal | Annual physical exam included |

For eligibility, most providers require a minimum of 3 to 10 employees to qualify for group plans, though modular options exist for smaller teams. Some enhanced plans allow pre-existing condition coverage up to the MBL, which is a major differentiator for employees with chronic conditions.

Pro Tip: Before signing any group plan, always ask specifically whether annual dental, mental health, and chronic disease provisions are included or require a separate add-on. These are the three coverage areas employees value most and are most likely to use.

For a broader look at what makes an enhanced plan worth the investment, the enhanced HMO benefits overview from John Clements breaks down the business case clearly.

How enhanced HMO options compare to PhilHealth and basic HMO plans

PhilHealth is not an HMO. It is a social insurance program designed primarily around case rates for inpatient hospital admissions. That means your employees can walk into a private specialist clinic or diagnostic center and PhilHealth will cover little to nothing of that visit.

Here is where the gap becomes visible. Enhanced HMOs complement PhilHealth by covering outpatient consultations, diagnostics, and specialist visits with lower out-of-pocket costs and faster access through private networks, unlike PhilHealth’s inpatient-focused case-rate model.

| Coverage type | PhilHealth | Basic HMO | Enhanced HMO |

|---|---|---|---|

| Inpatient hospitalization | Yes (case rates) | Yes | Yes, higher limits |

| Outpatient consultations | Very limited | Limited | Broad coverage |

| Specialist access | Minimal | Partial | Full network |

| Mental health | No | Rarely | Yes |

| Dental | No | No | Yes (add-on or built-in) |

| Out-of-pocket costs | High | Moderate | Low to zero |

| Waiting periods | None | Some | Plan-specific |

So when should you use each? A useful way to think about layering HMO and PhilHealth is by matching the coverage type to the healthcare scenario:

- PhilHealth: Use for inpatient hospitalization, government hospital admissions, and PhilHealth-accredited procedures

- Basic HMO: Use for routine checkups, minor emergencies, and general outpatient visits within the network

- Enhanced HMO: Use for specialist referrals, chronic condition management, dental, mental health, diagnostics, and dependent coverage

SMEs that want to maximize SME health investment often layer all three, using PhilHealth as the statutory base, a basic HMO as the primary daily-use card, and enhanced HMO as the layer that handles everything else. The cost of the enhanced layer is often offset by what employees no longer pay out of pocket, which matters more to your retention numbers than you might think.

For a detailed breakdown of how these two systems interact day to day, the HMO and PhilHealth differences guide is a practical reference.

Key business benefits: Talent attraction, productivity, and ROI

Enhanced HMO is not a perk. It is a business tool. SMEs that offer enhanced HMOs improve employee retention, reduce absenteeism, and boost productivity by delivering comprehensive benefits that attract talent and support a healthier workforce.

Here are the four business gains that show up most consistently when SMEs upgrade their health benefits:

- Lower turnover costs: Replacing an employee costs 50 to 200 percent of their annual salary. When employees feel their health is protected, they stay longer.

- Reduced absenteeism: Access to preventive care and early diagnostics means health issues are caught before they become serious enough to pull someone off the floor or out of the office.

- Stronger recruitment positioning: In competitive hiring markets, enhanced HMO is a concrete differentiator. Candidates compare benefit packages, and dental and mental health coverage signal that you take employee welfare seriously.

- Measurable productivity gains: Healthy employees perform better. Studies on employee retention data show that organizational support, including health benefits, directly reduces turnover intention in competitive industries.

“Enhanced health programs generate ROI between 47 and 52 percent when you factor in reduced absenteeism, lower turnover, and productivity gains.”

The math becomes clearer when you consider the HMO ROI for small businesses at scale. Even for a 20-person team, the savings from retaining two employees who might otherwise leave over benefit dissatisfaction can easily cover the annual premium difference between a basic and an enhanced plan.

Pro Tip: When pitching an enhanced HMO upgrade internally, frame it as a retention tool, not a healthcare cost. Present the plan cost against the average cost of one replacement hire. That number almost always makes the case for you.

To stay ahead on what employees expect in 2026, keeping up with health trends for SMEs will help you benchmark your plan against what competitors are offering.

What to know before choosing: Mechanics, limits, and compliance

Choosing an enhanced HMO plan is not just a benefits decision. It is a legal and operational one. Here is what SME leaders need to understand before signing.

Plan mechanics and eligibility: Most providers require a minimum of 3 to 10 enrolled employees for group rates. Tiered plans with digital claims typically include app-based authorization, pre-existing condition coverage in select tiers, and modular add-ons like dental or life insurance. Mobile apps reduce claims processing delays significantly.

Edge cases to watch for:

- Waiting periods of 3 to 6 months may apply for certain conditions

- Some hospitals require pre-authorization before admission

- PhilHealth must be billed first for inpatient cases before HMO coverage applies

- Out-of-network hospital visits may require reimbursement rather than cashless access

The compliance issue most SMEs overlook: Under Labor Code Article 100, reducing benefits risks liability once an enhanced HMO plan is granted, because it becomes a protected company practice. You cannot quietly downgrade next renewal year without employee consent or a negotiated agreement. This is not a reason to avoid enhanced plans. It is a reason to choose carefully from the start.

Here is a quick compliance checklist before you finalize your plan:

| Compliance area | What to confirm |

|---|---|

| PhilHealth integration | Is PhilHealth billed first for inpatient? |

| Non-diminution | Are you prepared to maintain this benefit level? |

| Dependent deductions | Are salary deductions for dependents properly documented? |

| Digital claims | Does the provider offer app-based claims submission? |

| Pre-auth requirements | Which procedures need prior authorization? |

For detailed guidance on staying compliant, the PhilHealth compliance for SMEs guide walks through current obligations. For specifics on covering family members, the dependent coverage guidance resource covers deduction rules and enrollment requirements.

Why enhanced HMO is more than an upgrade: A hard-won SME perspective

Most SME owners we speak with acknowledge the value of enhanced HMO in theory. Then they defer it to the next budget cycle. That gap between knowing and acting is exactly where the competitive disadvantage grows.

Here is what most articles do not tell you: an enhanced HMO plan is sticky in two directions. It builds loyalty among employees who feel genuinely supported. And once you offer it, you are legally protected from taking it away without consequences under Labor Code Art. 100. That is not a trap. That is a commitment signal. The companies that treat it as one tend to build cultures where people stay.

The biggest missed opportunity we see is SMEs not using digital HMO features for remote and distributed teams. If you have employees working from Cebu, Davao, or Cagayan de Oro, an enhanced plan with nationwide network access and app-based claims is not a luxury. It is the only way to give those employees real coverage. Start modular if budget is tight. Add dental or mental health as your headcount grows. But start.

Explore better HMO options for your SME

If this article has shifted how you see your current health benefit setup, the next step is straightforward. You do not need to overhaul everything at once.

Start by reviewing the features of enhanced HMO plans available through HMO Plans, where you can compare coverage tiers, add-ons, and benefit limits side by side. If you want guidance on what makes sense for your team size and industry, the member services for SMEs team is available to walk you through your options. HMO Plans, backed by Purple Cow and Etiqa, is built specifically for SMEs who want real coverage without the fine-print traps. Better coverage starts with one conversation.

Frequently asked questions

What makes an HMO plan ‘enhanced’ for SMEs in the Philippines?

An enhanced HMO provides broader coverage, including higher benefit limits, outpatient, mental health, dental, and dependent support, beyond what basic HMO or PhilHealth alone can offer.

Why should SMEs offer enhanced HMO instead of just PhilHealth?

Enhanced HMO provides comprehensive outpatient, specialist, and preventive care with faster access and less out-of-pocket cost, complementing PhilHealth’s mostly inpatient, case-rate model.

What is the main ROI SMEs can expect from enhanced HMO coverage?

Studies show enhanced HMO adoption can reduce turnover, cut absenteeism, and improve productivity, with ROI up to 47–52% from employee health programs when all factors are counted.

Are enhanced HMO benefits guaranteed and can they be reduced by SMEs?

Under Philippine labor law, once granted, benefits become a protected company practice under Labor Code Art. 100, meaning SMEs cannot reduce them without employee agreement.

What is the Philippine HMO market outlook for SMEs?

The Philippine HMO sector is expanding strongly, with Q3 2025 net income tripling year-over-year to PHP 2.44 billion, making it a stable and growing sector for SME benefit investment.

Recommended

- Eumir

- The Better HMO Plans for SMEs | Purple Cow | Blog | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- Evaluating Vendors: How SMEs Can Choose the Right HMO Partner

- Understanding HMO Basics: A Guide for New HR Managers in SMEs

- Why Outsource Office Cleaning: Key Benefits for SMEs

- AXA: Infiltrating the SMB Market with an Integrated Insurance Solution with IBSuite - Digital Insurance Platform | IBSuite Insurance Software | Modern Insurance System