Health insurance compliance in the Philippines: SME guide

TL;DR:

- SMEs must register with PhilHealth from the first employee, no size exceptions.

- Accurate calculation and timely remittance of contributions are crucial to avoid penalties.

- Digital tools streamline compliance, reducing errors and audit risks for small businesses.

Many SMEs in the Philippines operate under a dangerous assumption: that health insurance compliance only kicks in once you hit a certain headcount. Some owners believe five employees is the threshold. Others guess ten. The reality is far simpler and far more serious. Your obligations begin the moment you hire your first employee, and the law does not make exceptions for small teams or early-stage businesses. This guide walks you through exactly what you need to do, when to do it, and how to protect your business from costly mistakes while building a health benefits program your team will actually value.

Table of Contents

- Mandatory health insurance for SMEs: PhilHealth essentials

- Calculating and remitting PhilHealth contributions

- Penalties, audits, and risk mitigation for SMEs

- Digital tools and strategies for hassle-free compliance

- What most SME guides miss about compliance in the Philippines

- How to go beyond compliance and boost employee benefits

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Compliance starts immediately | All SMEs must register for PhilHealth and remit contributions as soon as they hire their first employee. |

| Know your rates and deadlines | PhilHealth contributions are precisely calculated and should be paid monthly to avoid stiff penalties. |

| Digital tools simplify compliance | Automated systems like ePRS streamline remittance and reporting, reducing human error and saving time. |

| Non-compliance carries steep risks | Missing obligations may result in costly fines, lost permits, and even jail time for SME owners. |

| Go beyond bare minimum | Investing in robust health benefits helps attract talent and secures your business against hidden setbacks. |

Mandatory health insurance for SMEs: PhilHealth essentials

PhilHealth (Philippine Health Insurance Corporation) is the national health insurance program of the Philippines, and every employer in the country is legally required to participate. There is no grace period based on company size, revenue, or industry. If you have staff, you have obligations.

PhilHealth registration is mandatory for all employers, including SMEs with even one employee, within 30 days of starting operations or hiring. Missing this window is not a minor administrative slip. It puts you immediately at risk of penalties and can complicate your business permit renewals down the road.

Here is what the law actually requires from you as an employer:

- Register your business with PhilHealth using the Employer Registration Form (ER1)

- Enroll each employee using the Member Registration Form (PMRF)

- Collect and remit both the employer and employee shares of the monthly contribution

- Keep accurate payroll and remittance records for audit purposes

- Update PhilHealth whenever employees are added, separated, or their salary changes

A common misconception is that sole proprietors with informal or contractual workers are exempt. They are not. No exemptions exist for SMEs, even when a single employee triggers full obligations. Whether your team member is full-time, part-time, or on a fixed-term contract, the rules apply.

“Compliance is not a size issue. It is a hiring issue. The moment someone works for you and receives compensation, you are an employer under Philippine law.”

Documentation is your best protection. Keep copies of all enrollment forms, proof of remittance, and payroll records. These are exactly what auditors look for. If you want a deeper breakdown of your 2026 obligations, the 2025 PhilHealth compliance guide covers updated rules and timelines in detail.

Calculating and remitting PhilHealth contributions

Once you are registered, the next step is getting the numbers right. Errors in contribution amounts are one of the most common compliance problems SMEs face, and they can quietly accumulate into significant arrears.

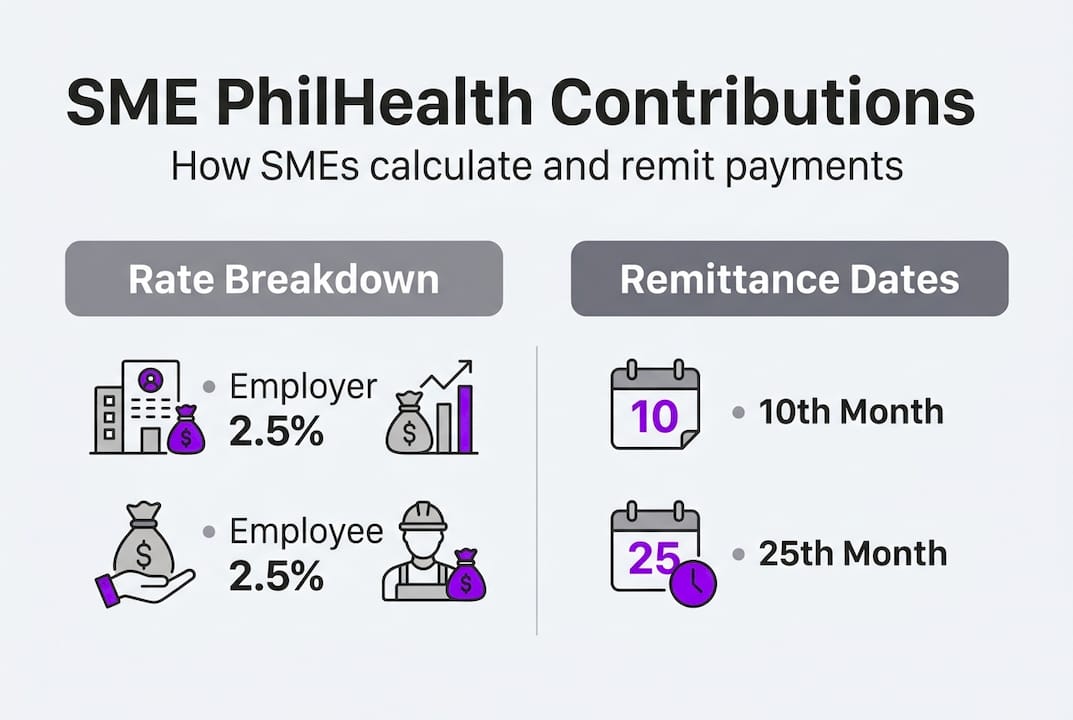

The current contribution rate for 2024 through 2026 is 5% of monthly basic salary, split equally between employer and employee at 2.5% each. There is a salary floor of P10,000 and a ceiling of P100,000, which means the minimum total monthly contribution is P500 and the maximum is P5,000.

| Monthly basic salary | Employee share (2.5%) | Employer share (2.5%) | Total contribution |

|---|---|---|---|

| P10,000 (floor) | P250 | P250 | P500 |

| P30,000 | P750 | P750 | P1,500 |

| P60,000 | P1,500 | P1,500 | P3,000 |

| P100,000 (ceiling) | P2,500 | P2,500 | P5,000 |

Here is how to handle remittance correctly:

- Compute each employee’s contribution based on their monthly basic salary

- Deduct the employee share from their paycheck

- Add your employer share on top

- Submit the combined amount by the due date

- File the required RF-1 report form to document all remittances

Remittance is due by the 10th or 25th of the following month, depending on your employer number. Larger employers use the Electronic Premium Remittance System (ePRS), a government platform that allows online payment and reporting. ePRS reduces manual errors and gives you a digital paper trail.

Pro Tip: Integrate PhilHealth contribution calculations directly into your payroll software. Most HR platforms in the Philippines support this natively. It eliminates manual math, reduces late payments, and keeps your records audit-ready automatically.

For SMEs thinking beyond basic compliance, understanding how HMO for SMEs supplements PhilHealth coverage is a smart next step. And if you want to understand the return on investing in employee health, maximizing SME health investment breaks down the business case clearly.

Penalties, audits, and risk mitigation for SMEs

Knowing the rules is one thing. Understanding what happens when you break them is what motivates real action. The penalties for non-compliance are not symbolic. They are serious, layered, and can threaten your entire operation.

Penalties for non-remittance include monthly interest of 2 to 3%, fines ranging from P5,000 to P100,000 per violation, imprisonment of 6 months to 6 years for responsible officers, and complications with business permit renewals. These are not worst-case scenarios reserved for large corporations. SME owners have faced all of them.

Here is what typically triggers an audit or investigation:

- Employee complaints filed directly with PhilHealth or DOLE (Department of Labor and Employment)

- Discrepancies between reported payroll and actual salaries

- Failure to update employee records after separations or salary changes

- Business permit renewal checks by local government units (LGUs)

- Random compliance audits by government agencies

Non-compliance risks DOLE audits and permit denials, and while grace periods or waivers for arrears are occasionally granted, they are not guaranteed. Do not plan your compliance strategy around the hope of a waiver.

The maximum combined exposure for a single violation can reach P100,000 in fines plus accumulated interest, on top of criminal liability for company officers. That is a significant financial and reputational hit for any SME.

Pro Tip: Schedule a quarterly internal compliance check. Pull your PhilHealth remittance records, cross-reference them with your payroll, and verify that all active employees are properly enrolled. Use the PhilHealth employer portal to confirm your account status. Thirty minutes every three months can save you from years of legal headaches.

For a fuller picture of what SME HMO compliance looks like when you layer private health coverage on top of your PhilHealth obligations, that resource covers both sides of the equation.

Digital tools and strategies for hassle-free compliance

Manual compliance is where most SMEs get into trouble. Spreadsheets get outdated. Deadlines get missed. Calculations contain errors that nobody catches until an auditor does. The good news is that digital tools have made PhilHealth compliance significantly easier, even for businesses with no dedicated HR team.

| Approach | Manual process | Digital process |

|---|---|---|

| Contribution calculation | Done by hand each payroll cycle | Auto-calculated in payroll software |

| Remittance submission | Bank visits or manual online filing | ePRS online portal, scheduled payments |

| Record keeping | Physical files, spreadsheets | Cloud-stored, audit-ready records |

| Error rate | Higher, especially with salary changes | Significantly reduced |

| Time investment | Several hours monthly | Minutes per cycle |

SMEs benefit from digital tools like ePRS and integrating them with payroll systems for consistent, error-free compliance. Here are the key platforms and tools worth knowing:

- ePRS (Electronic Premium Remittance System): PhilHealth’s official online remittance platform for employers

- RF-1 digital filing: Online submission of the monthly remittance report

- HR payroll software: Platforms like Sprout HR, KMC, and PayrollHero support PhilHealth integration

- PhilHealth employer portal: For checking contribution histories, employee enrollment status, and account updates

For SMEs tracking broader health trends and digital compliance strategies, the PhilHealth ePRS platform article covers what forward-thinking businesses are adopting in 2026. You can also explore accredited HMO platforms that connect seamlessly with your existing health benefits setup, and review digital HR tools that reduce administrative overhead across the board.

The shift from manual to digital is not just about convenience. It is about removing human error from a process where errors have legal consequences.

What most SME guides miss about compliance in the Philippines

Most compliance guides treat PhilHealth registration as a checkbox. Register, compute, remit, repeat. That framing misses something important: compliance is also a signal. It tells your employees, your clients, and government agencies that your business operates with integrity.

We have seen SMEs in tech, hospitality, and healthcare lose talented employees not because of low salaries, but because staff discovered their contributions were never remitted. That is a trust violation that no bonus can fix.

The SMEs that handle compliance best are not the ones who scramble before permit renewal season. They are the ones who treat documentation as an ongoing habit. They over-prepare for audits that may never come. They build relationships with their PhilHealth account officers. They maximize health investment by pairing mandatory contributions with supplemental HMO coverage, which also signals to employees that the company genuinely cares.

Digital adoption is not optional anymore. SMEs that resist it are not saving time. They are accumulating risk. The businesses that thrive long-term treat compliance infrastructure the same way they treat their accounting systems: as a foundation, not an afterthought.

How to go beyond compliance and boost employee benefits

Meeting your PhilHealth obligations is the floor, not the ceiling. The SMEs that attract and retain top talent treat health coverage as a competitive advantage, not just a legal requirement.

When you pair PhilHealth compliance with a well-structured HMO plan, you give employees cashless access to top hospitals, outpatient care, and emergency coverage that goes far beyond what PhilHealth alone provides. That combination drives morale, reduces absenteeism, and makes your company a place people want to stay. Explore best HMO plans for SMEs designed specifically for Philippine businesses like yours, or review the full range of SME HMO features to find the right fit. Our team is ready to help you build a benefits package that works for your headcount and your budget.

Frequently asked questions

Are SMEs with only one employee required to register with PhilHealth?

PhilHealth registration is mandatory for all employers, including SMEs with a single employee, and full compliance obligations apply from the first hire.

What is the PhilHealth contribution rate for 2026 and how is it shared?

The rate is 5% of monthly basic salary for 2024 through 2026, split equally at 2.5% each between employer and employee, with a salary floor of P10,000 and a ceiling of P100,000.

How can SMEs make PhilHealth remittances and reports more efficient?

Digital tools like ePRS and payroll software integrations automate contribution calculations, remittance submissions, and record keeping, reducing errors and saving time each month.

What are the penalties for late or non-remittance of PhilHealth contributions?

Penalties include 2 to 3% monthly interest, fines from P5,000 to P100,000 per violation, imprisonment of 6 months to 6 years, and potential loss of business permits.

Are there grace periods for SMEs that fall behind on contributions?

Grace periods or waivers for arrears are occasionally granted but are not guaranteed, so prompt action and proactive communication with PhilHealth is always the safer path.