How HMOs support SME health benefits in Philippines 2026

Many SME owners believe PhilHealth alone provides sufficient health coverage for their employees. This misconception leaves workers vulnerable to significant out-of-pocket expenses when serious illness strikes. Health Maintenance Organizations supplement mandatory PhilHealth coverage by filling critical gaps in employee healthcare. Understanding how HMOs work alongside PhilHealth helps you build a competitive benefits package that protects your team and strengthens your business. This guide explains how HMOs deliver comprehensive health insurance tailored specifically for Philippine SMEs in 2026.

Table of Contents

- How Hmos Complement Philhealth In Philippine Smes

- Tailored Hmo Plans Designed For Small And Medium Enterprises

- Navigating Legal And Operational Aspects Of Hmo Enrollment For Smes

- Benefits And Challenges Of Using Hmos For SME Health Management In 2026

- Explore Tailored Hmo Plans For Your Sme Today

Key takeaways

| Point | Details |

|---|---|

| Supplemental coverage | HMOs fill PhilHealth gaps by covering outpatient care, diagnostics, and procedures often excluded from basic government insurance. |

| SME flexibility | Specialized plans accommodate businesses with as few as one employee while including pre-existing conditions and dependent coverage. |

| Voluntary provision | Employers choose whether to offer HMO benefits, but once granted, coverage cannot be reduced without legal consequences. |

| Claims processing | Cashless access requires pre-authorization and accredited providers, with PhilHealth benefits deducted before HMO coverage applies. |

| Competitive advantage | Comprehensive health benefits attract skilled talent and reduce absenteeism, improving productivity despite rising healthcare costs. |

How HMOs complement PhilHealth in Philippine SMEs

PhilHealth provides basic inpatient case rates but excludes many essential services your employees need. The government program covers hospitalization at fixed rates, leaving gaps in outpatient consultations, diagnostic tests, and preventive care. HMOs provide prepaid healthcare via accredited networks supplementing PhilHealth to address these limitations.

Your employees access care through an HMO network of hospitals, clinics, and specialists without paying upfront. The HMO processes claims directly with providers after PhilHealth deducts its share. This cashless system eliminates the financial burden of medical emergencies and routine care. Most plans require pre-authorization for scheduled procedures, but emergency situations receive immediate coverage.

Understanding PhilHealth and HMO synergy helps you maximize value from both programs. PhilHealth acts as primary coverage, paying its portion first. Your HMO then covers remaining costs up to policy limits, dramatically reducing what employees pay from their own pockets.

Consider these coverage differences:

- PhilHealth covers basic ward accommodations while HMOs upgrade to private or semi-private rooms

- Government insurance excludes most outpatient care while HMOs include consultations and diagnostics

- PhilHealth limits prescription coverage while HMOs provide broader medication benefits

- Emergency care receives faster processing through HMO networks compared to standard PhilHealth claims

“The combination of PhilHealth and HMO coverage creates a safety net that protects employees from catastrophic medical expenses while maintaining access to quality healthcare facilities.”

Pre-existing conditions present unique challenges under standard insurance models. Many HMO plans now cover these conditions fully or with waiting periods, unlike traditional insurance that excludes them entirely. This protection proves especially valuable for SMEs hiring experienced professionals who may have existing health concerns.

Exclusions still apply to certain cosmetic procedures, experimental treatments, and services outside the provider network. Review policy documents carefully to understand what your plan covers and educate employees about proper utilization. The difference between PhilHealth and HMO structures affects how claims process and what out-of-pocket costs remain.

Tailored HMO plans designed for small and medium enterprises

SME-focused HMO plans accommodate businesses of all sizes with flexible enrollment requirements. Howden Prime offers coverage from one employee with 100% pre-existing condition coverage and dependent options, eliminating traditional barriers that excluded small companies from comprehensive health benefits.

Coverage limits typically range from PHP 100,000 to PHP 500,000 per member annually, with higher tiers available for executive teams. Your business selects benefit levels based on budget and employee needs. Most providers structure pricing around employee count, age demographics, and selected coverage maximums.

| Plan Feature | Basic Coverage | Enhanced Coverage | Premium Coverage | | — | — | — | | Annual Limit | PHP 100,000 | PHP 250,000 | PHP 500,000 | | Pre-existing | Partial after waiting period | Full coverage | Full immediate coverage | | Dependents | 50% cost share | 50% cost share | Included or reduced share | | Maternity | Basic delivery only | Prenatal through delivery | Comprehensive with complications | | Annual Checkup | Not included | Basic screening | Comprehensive executive physical |

Dependent coverage extends benefits to spouses and children, though most plans require employee or employer cost-sharing for family members. Typical arrangements cover employees fully while dependents receive 50% employer subsidy or full employee payment. This structure keeps premiums manageable while offering valuable family protection.

Maternity benefits deserve special attention when evaluating plans. Basic coverage includes normal delivery costs, while comprehensive plans cover prenatal care, complications, and newborn care. Female employees and their spouses benefit significantly from robust maternity coverage that reduces the financial stress of growing families.

Annual physical examinations promote preventive care and early disease detection. Enhanced plans include comprehensive health screenings, blood work, and specialist consultations. These checkups catch health issues before they become serious, reducing long-term costs and keeping your workforce healthy.

Pro Tip: Start with moderate coverage limits and upgrade as your business grows rather than overcommitting to premiums you cannot sustain during slower periods.

Premium calculations factor in multiple variables beyond simple headcount. Age distribution affects pricing since older employees typically require more healthcare services. Industry risk levels influence rates, with office workers costing less than those in physically demanding roles. Geographic location matters because urban areas offer more provider options while rural coverage may cost more.

Explore HMO plans for small businesses that scale with your growth. Flexible enrollment periods let you add new hires throughout the year rather than waiting for annual renewal. This agility supports rapid hiring and ensures every team member receives protection from day one.

Customization options enhance standard packages:

- Dental coverage for routine care and major procedures

- Vision benefits including eye exams and corrective lenses

- Mental health services and counseling sessions

- Alternative medicine like acupuncture or chiropractic care

- Life and accident insurance bundled with health coverage

Review HMO insurance for SMEs annually to ensure your plan evolves with workforce needs. Adding specialized benefits as you grow demonstrates commitment to employee wellbeing and strengthens retention.

Navigating legal and operational aspects of HMO enrollment for SMEs

Enrollment is voluntary with no law mandating full employer funding, but once granted, benefits cannot be diminished without violating employee rights. This legal protection means you must maintain or improve coverage levels after initial provision. Reducing benefits or eliminating HMO coverage entirely exposes your business to labor disputes and potential legal action.

Cost-sharing arrangements between employers and employees provide flexibility in funding health benefits. Many SMEs cover 100% of employee premiums while requiring staff to pay for dependent coverage. Others split costs 50-50 or use tiered structures where the company pays more for lower-wage workers. Document your cost-sharing policy clearly in employment contracts and company handbooks.

Regularization triggers full benefit eligibility in most SME policies. Probationary employees may receive limited coverage or none at all during their first few months. Once regularized, workers gain access to complete HMO benefits including dependent options. This phased approach controls costs while rewarding employees who successfully complete probation.

Claims processing involves cashless access at accredited providers where PhilHealth deductions apply first, followed by HMO coverage up to policy limits. Employees present their HMO card at the facility, which verifies eligibility and coverage. The provider submits claims directly to both PhilHealth and the HMO, eliminating out-of-pocket payments for covered services.

Pre-authorization requirements protect against unnecessary procedures and control costs. Non-emergency hospitalizations, surgeries, and expensive diagnostics require approval before treatment begins. Emergency cases receive automatic coverage, with documentation submitted after stabilization. Understanding these procedures prevents claim denials and ensures smooth processing.

Common claim issues include:

- Incomplete medical records or missing authorization forms

- Treatment at non-accredited facilities outside the network

- Services excluded under policy terms like cosmetic procedures

- Exceeding annual benefit limits before year end

- Pre-existing condition waiting periods not yet satisfied

Pro Tip: Designate an HR team member as HMO coordinator to handle pre-authorizations, answer employee questions, and resolve claim issues quickly.

Maintain PhilHealth compliance alongside HMO enrollment since both programs work together. Your business must remit PhilHealth contributions monthly regardless of HMO coverage. The government program remains primary insurance, with HMOs providing supplemental benefits.

Document retention proves critical during claim disputes or audits. Keep copies of policy documents, enrollment forms, premium payment records, and claim submissions for at least three years. Digital storage simplifies organization and retrieval when questions arise.

Employee education prevents misunderstandings about coverage limits and proper utilization. Conduct orientation sessions explaining how to access care, which providers accept the plan, and what services require pre-authorization. Provide written guides and contact information for the HMO customer service team.

Network directories list accredited hospitals, clinics, and specialists where employees receive cashless service. Encourage staff to verify provider participation before scheduling appointments. Out-of-network care may require upfront payment with reimbursement claims submitted later, creating cash flow challenges for employees.

Understanding legal aspects of employer HMO contributions protects your business from labor violations while ensuring employees receive entitled benefits. Consult with legal counsel when modifying existing plans or implementing new coverage to avoid unintended consequences.

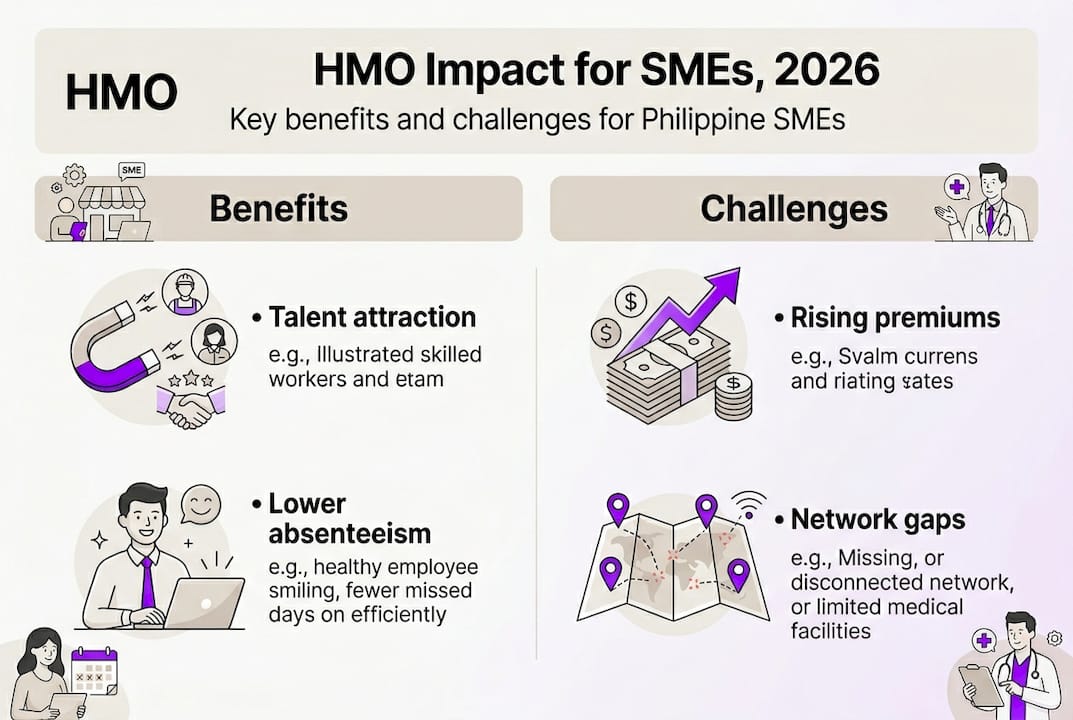

Benefits and challenges of using HMOs for SME health management in 2026

HMOs help SMEs attract and retain talent while reducing absenteeism and managing costs amid inflation, with premiums ranging from PHP 10,000 to PHP 47,000 annually per employee depending on coverage levels. Comprehensive health benefits differentiate your company in competitive labor markets where skilled workers evaluate total compensation packages beyond salary alone.

Talent acquisition improves significantly when you offer robust health coverage. Job candidates compare benefits between offers, and quality HMO plans tip decisions in your favor. Experienced professionals with families particularly value dependent coverage and comprehensive benefits that protect their loved ones.

Employee retention strengthens when workers feel protected against health emergencies. The cost of replacing skilled employees far exceeds HMO premiums. Turnover disrupts operations, reduces productivity, and requires expensive recruitment and training investments. Health benefits create loyalty and reduce voluntary departures.

Absenteeism decreases when employees access preventive care and early treatment. Workers with HMO coverage visit doctors promptly rather than delaying care until conditions worsen. This proactive approach keeps minor issues from becoming serious illnesses requiring extended leave. Annual checkups catch problems early, reducing sick days and maintaining workforce productivity.

| Benefit Category | Impact on SMEs | Measurable Outcome |

|---|---|---|

| Talent Attraction | Competitive advantage in hiring | Higher quality applicants, faster fills |

| Retention | Reduced turnover costs | Lower recruitment expenses, stable teams |

| Productivity | Fewer sick days | Consistent output, project continuity |

| Cost Management | Predictable healthcare expenses | Budgetable premiums versus unpredictable medical costs |

| Employee Morale | Increased job satisfaction | Higher engagement, better performance |

Cost management requires balancing comprehensive coverage against budget constraints. Medical inflation runs 3-4 times general inflation rates, pushing premiums higher annually. The Philippine HMO industry saw strong growth with PHP 74.64 billion in benefits disbursed in 2025, reflecting rising importance and utilization across all business sizes.

Premium increases average 10-15% annually as medical costs rise and utilization grows. Budget for these escalations when planning long-term benefit strategies. Some SMEs absorb increases entirely while others implement modest employee cost-sharing to maintain coverage sustainability.

Claims growth indicates both higher utilization and improved access to care. Your employees use benefits more frequently as they understand coverage and overcome hesitation about seeking treatment. This increased utilization validates your investment while demonstrating real value to your workforce.

“Strategic health benefit investments deliver measurable returns through improved retention, reduced absenteeism, and enhanced ability to compete for top talent in tight labor markets.”

Challenges include managing premium inflation while maintaining coverage quality. Some SMEs reduce benefit limits or increase employee cost-sharing to control expenses. Others shop annually for competitive rates, though frequent provider changes disrupt employee familiarity with networks and processes.

Claim denials frustrate employees and create administrative burdens. Common denial reasons include incomplete documentation, non-covered services, or out-of-network providers. Clear communication about proper utilization and pre-authorization requirements minimizes these issues.

Provider network limitations affect rural businesses where accredited facilities may be scarce. Employees in remote areas struggle to access cashless care, requiring reimbursement claims that delay payment and create cash flow stress. Evaluate network coverage in your operating locations before selecting a plan.

Pro Tip: Request detailed claims reports quarterly to identify utilization patterns, common denial reasons, and opportunities to improve employee education about proper benefit usage.

Explore maximizing health investments through strategic benefit design that balances cost and coverage. Tiered plans let employees choose coverage levels matching their needs, with higher earners selecting premium options while others opt for basic protection. This flexibility controls costs while offering choice.

Wellness programs complement HMO coverage by promoting healthy behaviors that reduce long-term claims. Simple initiatives like health screenings, fitness challenges, and nutrition education improve workforce health while demonstrating commitment to employee wellbeing beyond insurance coverage.

Understanding HMO benefits for companies helps you evaluate return on investment beyond simple cost analysis. Intangible benefits like improved morale, stronger company culture, and enhanced employer brand contribute to business success in ways that justify premium expenses.

Explore tailored HMO plans for your SME today

Comprehensive health coverage no longer remains exclusive to large corporations. Purple Cow HMO plans deliver enterprise-grade benefits designed specifically for Philippine SMEs, with flexible coverage options that scale with your business growth. Their 100% coverage of pre-existing conditions eliminates the exclusions that traditionally limited small business health insurance.

Explore HMO plan features including cashless access to premier facilities, comprehensive inpatient and outpatient care, and digital healthcare platforms that simplify benefit administration. Optional add-ons like dental coverage, annual physical exams, and life insurance let you customize packages matching your workforce needs and budget constraints. Access member services designed to streamline enrollment, claims processing, and ongoing support for your team.

FAQ

What is the role of an HMO in small and medium enterprises?

HMOs supplement PhilHealth by providing broader prepaid healthcare coverage for SME employees. They fill gaps in government insurance through cashless access to accredited providers, comprehensive outpatient care, and higher coverage limits. This supplemental protection reduces out-of-pocket medical expenses while improving access to quality healthcare facilities.

Are SMEs required to provide HMO coverage for their employees?

HMO coverage remains voluntary for SMEs with no legal mandate to provide or fund benefits fully. However, once you grant health benefits, you cannot reduce or eliminate them without violating employee rights. Many SMEs implement cost-sharing arrangements where employees contribute toward premiums or dependent coverage.

How do claim processes work with HMOs and PhilHealth?

Claims are first processed through PhilHealth deductions, then HMOs cover remaining costs up to policy limits. Employees present their HMO card at accredited facilities for cashless service. Pre-authorization is generally required for non-emergency procedures, while emergency care receives immediate coverage with documentation submitted afterward.

What challenges do SMEs face when using HMO services?

SMEs may encounter claim delays or denials due to incomplete documents or use of non-accredited providers. Premium inflation averaging 10-15% annually strains budgets, requiring careful cost management. Limited provider networks in rural areas create access challenges, and employee education about proper utilization requires ongoing effort to minimize claim issues.

Recommended

- Eumir

- The Better HMO Plans for SMEs | Purple Cow | Blog | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- HMO Health Insurance for Small and Medium Enterprises in the Philippines

- 2025 Health Trends for SMEs in the Philippines: Key Strategies for Smarter Benefits

- What is an HMO dental plan? Affordable care guide 2026