Optimize your employee benefits utilization process for SMEs

TL;DR:

- Proper understanding of PhilHealth pathways and documentation reduces claim denial risks for SMEs.

- Combining PhilHealth with HMO plans ensures comprehensive coverage, cost savings, and administrative efficiency.

- Proactive preparation and regular benefits reviews help SMEs maximize their employee health investment.

Managing employee health benefits should not feel like solving a puzzle with missing pieces. For many SME owners and HR managers in the Philippines, rising medical costs and confusing claim procedures create real headaches every year. Medical inflation keeps pushing healthcare expenses higher, squeezing budgets that are already stretched thin. The good news is that a clear, repeatable benefits utilization process can eliminate most of the confusion, prevent costly claim denials, and help your employees get the care they need without unnecessary delays. This guide walks you through every stage, from understanding PhilHealth pathways to layering HMO coverage for maximum impact.

Table of Contents

- Understanding the basic PhilHealth benefits utilization process

- Preparing essential requirements and ensuring eligibility

- Step-by-step guide: Filing and processing benefit claims

- Troubleshooting and optimizing: Common pitfalls and the case for HMO integration

- A smarter way forward: Expert perspective on benefits optimization

- Get the most from your employee benefits investment

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know the claim pathways | PhilHealth claims are processed through hospitals or direct member filing—understand which applies when. |

| Prepare the right documents | Accurate and complete documentation is key to quick, successful claims. |

| Avoid common mistakes | Missed deadlines and eligibility issues are the main reasons claims get denied. |

| Layer HMO for full coverage | Supplementing PhilHealth with HMO plans protects both your team and your budget. |

Understanding the basic PhilHealth benefits utilization process

The term “benefits utilization process” simply means the steps your employees and your organization follow to access and claim health coverage. For SMEs, getting this right is not optional. It directly affects your cash flow, your compliance standing, and how your team feels about working for you.

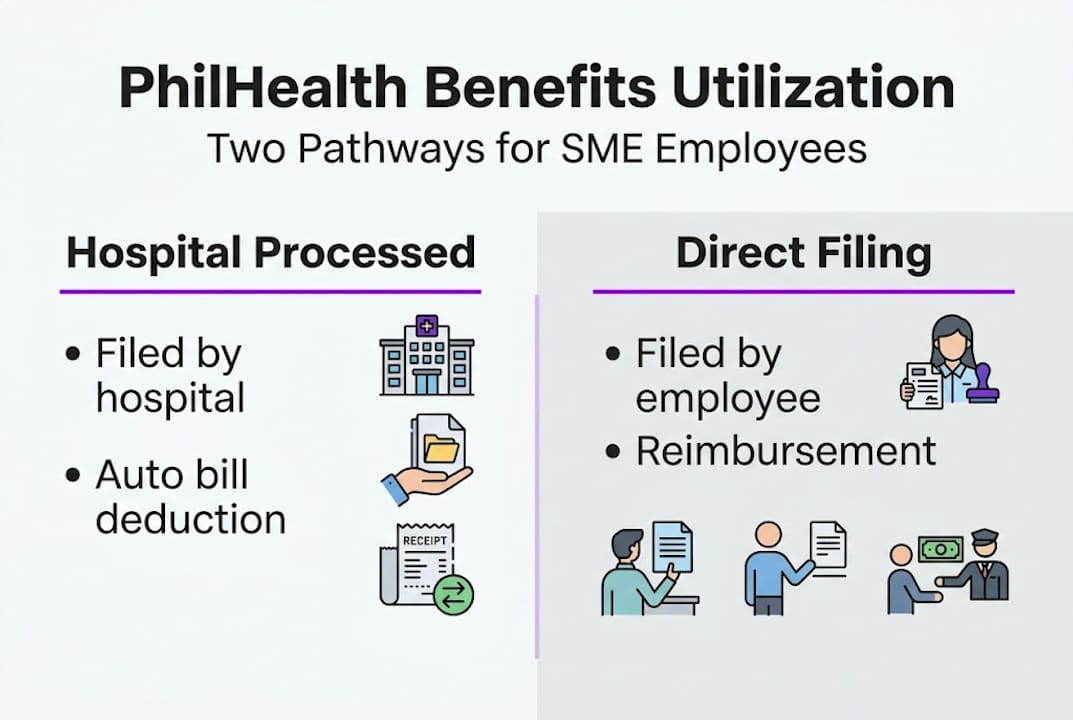

PhilHealth, the national health insurance program, operates through two distinct claim pathways. According to the two main pathways, hospital-processed claims are the default for accredited facilities, where the hospital deducts the applicable case rate directly from the patient’s bill before discharge. The second pathway is direct member filing, where the employee submits the claim personally at the PhilHealth Local Health Insurance Office (LHIO), typically used when the facility is not PhilHealth-accredited or when the hospital fails to process the deduction.

Here is a quick comparison of both pathways:

| Feature | Hospital-processed | Direct member filing |

|---|---|---|

| Who files | Accredited hospital | Employee or HR |

| When benefit is applied | Before discharge | After filing at LHIO |

| Documents needed | Minimal (hospital handles) | Full set required |

| Processing time | Immediate deduction | Days to weeks |

| Best for | Accredited facilities | Non-accredited or missed deductions |

The pathway your employee ends up using depends heavily on whether the hospital holds PhilHealth accreditation. This is why maximizing SME health investment starts with knowing which hospitals in your area are accredited before a medical emergency happens.

Key facts every HR manager should know:

- Case rates are fixed amounts PhilHealth pays per diagnosis, not per service item

- The hospital absorbs any costs above the case rate unless supplemental coverage applies

- Non-accredited hospitals cannot process PhilHealth deductions at all

- Outpatient and inpatient claims follow different forms and timelines

Medical costs in the Philippines have been rising steadily, making it critical for SMEs to use every peso of their PhilHealth coverage correctly. Missing a deduction or filing late is essentially leaving money on the table.

Preparing essential requirements and ensuring eligibility

Once you understand how the process works, the next priority is getting everything ready before a health issue arises. Scrambling for documents during a hospitalization is stressful and often leads to errors that cause denials.

For PhilHealth claims, required documents include the PhilHealth Claim Form 1, an updated Member Data Record (MDR), and a valid government-issued ID. Eligibility requires at least three monthly premium contributions within the last six months for most benefit packages. There is also a 45-day annual limit on inpatient confinement benefits, which many SME owners do not realize until it is too late.

Here is a document checklist organized by claim type:

| Document | Hospital-processed | Direct filing |

|---|---|---|

| PhilHealth Claim Form 1 | Hospital prepares | Employee fills out |

| Updated MDR | Required | Required |

| Valid government ID | Required | Required |

| Official receipts | Not needed | Required |

| Discharge summary | Hospital provides | Employee obtains |

To file correctly, follow these steps before any hospitalization:

- Confirm the employee’s PhilHealth number is active and linked to your company

- Verify that at least three monthly contributions are posted in the last six months

- Download and pre-fill Claim Form 1 where possible

- Keep a digital copy of the MDR updated at least quarterly

- Confirm the hospital’s accreditation status on the PhilHealth website

Pro Tip: Create a shared digital folder for each employee that contains their PhilHealth number, MDR, and a scanned valid ID. When a hospitalization happens, your HR team can access everything in minutes instead of hours. This one habit alone can prevent most document-related denials.

A solid benefits onboarding for SMEs program should include a walkthrough of PhilHealth requirements on day one. Pair that with a regular SME coverage check-up at least once a year to catch contribution gaps before they become eligibility problems.

Step-by-step guide: Filing and processing benefit claims

With your documents organized and eligibility confirmed, you are ready to move through the actual claims process. The steps differ depending on which pathway applies, so it helps to know both.

For hospital-processed claims (accredited facilities):

- Inform the admitting section that the patient is a PhilHealth member at check-in

- Present the PhilHealth ID or member number along with a valid ID

- The hospital’s PhilHealth coordinator prepares and submits the claim forms

- The case rate is deducted from the total bill before the patient settles the balance

- Request a copy of the PhilHealth Benefit Eligibility Form (PBEF) for your records

For direct member filing (non-accredited facilities):

- Pay the full hospital bill and collect all official receipts

- Obtain the discharge summary, medical certificate, and itemized statement of account

- Fill out PhilHealth Claim Form 1 completely

- Submit the full document set to the nearest PhilHealth LHIO within 60 days of discharge

- Track the claim status through the PhilHealth online portal or by visiting the office

The 60-day filing deadline for direct filing is strict. Missing it means forfeiting the benefit entirely. For Z Benefits, which cover catastrophic conditions like cancer and end-stage renal disease, pre-authorization from PhilHealth is required before treatment begins.

Important: Late submissions and incomplete forms are the top two reasons PhilHealth claims get denied. Set a calendar reminder the day after discharge to start the direct filing process if the hospital could not process it.

Pro Tip: Assign one HR staff member as the designated PhilHealth coordinator. This person tracks all active hospitalizations, monitors submission deadlines, and follows up on pending claims. Centralizing this responsibility reduces errors significantly.

For SMEs doing a reviewing SME health plans exercise, cross-checking your claim history against PhilHealth records can reveal patterns, like specific hospitals that frequently miss deductions, so you can adjust your accredited facility list.

Troubleshooting and optimizing: Common pitfalls and the case for HMO integration

Even when you follow every step correctly, claims can still hit roadblocks. Knowing the most common failure points helps you respond quickly and appeal effectively.

The top reasons PhilHealth claims get denied include:

- Eligibility lapses: Contributions were not posted in time or the three-month requirement was not met

- Coding errors: The diagnosis code on the claim form does not match the discharge summary

- Late submission: The 60-day direct filing window was missed

- Balance billing disputes: Private hospitals sometimes charge beyond the case rate without proper disclosure

- Incomplete documents: Missing receipts, unsigned forms, or outdated MDR copies

If a claim is denied, do not give up. You can file a formal appeal at the PhilHealth LHIO with a written explanation and supporting documents. Most coding errors and eligibility issues can be resolved with a correction letter and updated contribution records.

Here is where the bigger picture becomes important. PhilHealth provides a valuable baseline, but it was never designed to cover everything. SMEs optimize their health spending by supplementing PhilHealth with affordable group HMO plans, which cover primary care, outpatient consultations, and services that PhilHealth case rates do not include.

Pro Tip: Run a simple benefits gap analysis once a year. List what PhilHealth covers under each common diagnosis, then identify where your employees are paying out of pocket. Those gaps are exactly where an HMO plan adds measurable value.

For a deeper look at closing those gaps, explore maximizing health ROI and stay current on health trends for SMEs to see where group coverage is heading in 2026.

A smarter way forward: Expert perspective on benefits optimization

Here is something most benefits articles will not tell you: the biggest mistake SMEs make is not choosing the wrong plan. It is treating benefits as a compliance checkbox instead of a business tool.

We see it consistently. Companies spend energy worrying about premium costs while ignoring the administrative drag of unmanaged claims, repeated denials, and employee confusion during hospitalizations. That hidden cost is real, and it adds up faster than any monthly premium.

The sustainable path forward is straightforward: get PhilHealth compliance right first, then layer an HMO plan on top. Hospital accreditation ensures seamless deduction-at-source, which cuts your admin burden significantly. From there, an HMO fills the gaps PhilHealth was never meant to cover.

The concern about cost is understandable, but group HMO benchmarks consistently show ROI through reduced absenteeism, faster recovery, and stronger employee retention. The math works in your favor when you look at the full picture.

For SMEs exploring PhilHealth + HMO strategies, the combination is not a luxury. It is the most cost-effective way to protect your team and your business at the same time.

Get the most from your employee benefits investment

Streamlining your benefits process does not have to mean more paperwork or bigger budgets. It means choosing the right tools and the right partner.

At HMO Plans, we build HMO plan features specifically for SMEs in the Philippines, with 100% coverage for pre-existing and congenital conditions up to the Maximum Benefit Limit, cashless access to the Big 9 Hospitals, and flexible add-ons that fit your team’s real needs. Our member services team handles the complexity so your HR staff does not have to. Ready to close the gaps in your current coverage? Explore affordable HMO plans designed for businesses just like yours.

Frequently asked questions

What is the difference between hospital-processed and direct PhilHealth claims?

Hospital-processed claims deduct the benefit from your bill before discharge at accredited facilities; direct filing means the employee submits the claim personally at the PhilHealth LHIO when the hospital is not accredited or failed to process it.

What documents are required for PhilHealth benefits filing?

You need Claim Form 1, MDR, and valid ID at minimum; also confirm that at least three monthly contributions are posted within the last six months before filing.

How can SMEs avoid common PhilHealth claim denials?

Verify employee eligibility before hospitalization, submit complete and accurate documents, and file within the 60-day deadline to prevent the most common denial triggers.

Why should SMEs consider integrating HMO with PhilHealth?

Integrating HMO fills the coverage gaps PhilHealth does not address, and group HMO plans reduce out-of-pocket costs while improving employee retention and overall satisfaction.

Recommended

- Onboarding New Employees with Better Health Benefits: A Winning Hiring Strategy for SMEs

- 2025 Health Trends for SMEs in the Philippines: Key Strategies for Smarter Benefits

- How SMEs Should Review Health Plans

- Beyond PhilHealth: How SMEs Can Maximize Health Investments for Better ROI

- Affordable Virtual Care Plans for Employers & Teams | Chameleon