SME health insurance terms: 5 key concepts for smarter benefits

TL;DR:

- Medical inflation in the Philippines is rising 3 to 4 times faster than general inflation, straining SME budgets.

- Key health insurance terms like HMO, PhilHealth, MBL, and PECs are essential for informed coverage decisions.

- Combining PhilHealth with private HMO plans reduces out-of-pocket costs and enhances employee protection.

Medical costs in the Philippines are rising fast, and for SME owners, that pressure is real. Medical inflation is growing 3 to 4 times faster than general inflation, meaning a health benefit that felt affordable two years ago may already be straining your budget. Most business owners assume health insurance is either too expensive or too complicated to figure out. But the truth is, not understanding the terms is what makes it costly. When you know what HMO, MBL, PhilHealth, and pre-existing condition actually mean, you make sharper decisions, protect your team better, and stop overpaying for coverage gaps.

Table of Contents

- Core health insurance terms every SME must know

- Comparing main health insurance options: PhilHealth vs HMO

- Pre-existing conditions, exclusions, and underwriting for SMEs

- Cost control, group benefits, and recent trends for Philippine SMEs

- A fresh perspective: Focusing on value, not just price, in SME health insurance

- Get started: Flexible SME health plans that truly fit your team

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know key terms | Understanding crucial insurance terms helps you pick the best coverage for your SME team. |

| Combine PhilHealth and HMO | Using both PhilHealth and an HMO supplements gaps for truly comprehensive employee healthcare. |

| Review limits and exclusions | Always check waiting periods and pre-existing condition rules to avoid surprises. |

| Group plans save money | Pooling employees into group plans helps control costs and beat medical inflation. |

| Transparency prevents denial | Be honest about health history to ensure all claims are honored without unexpected denials. |

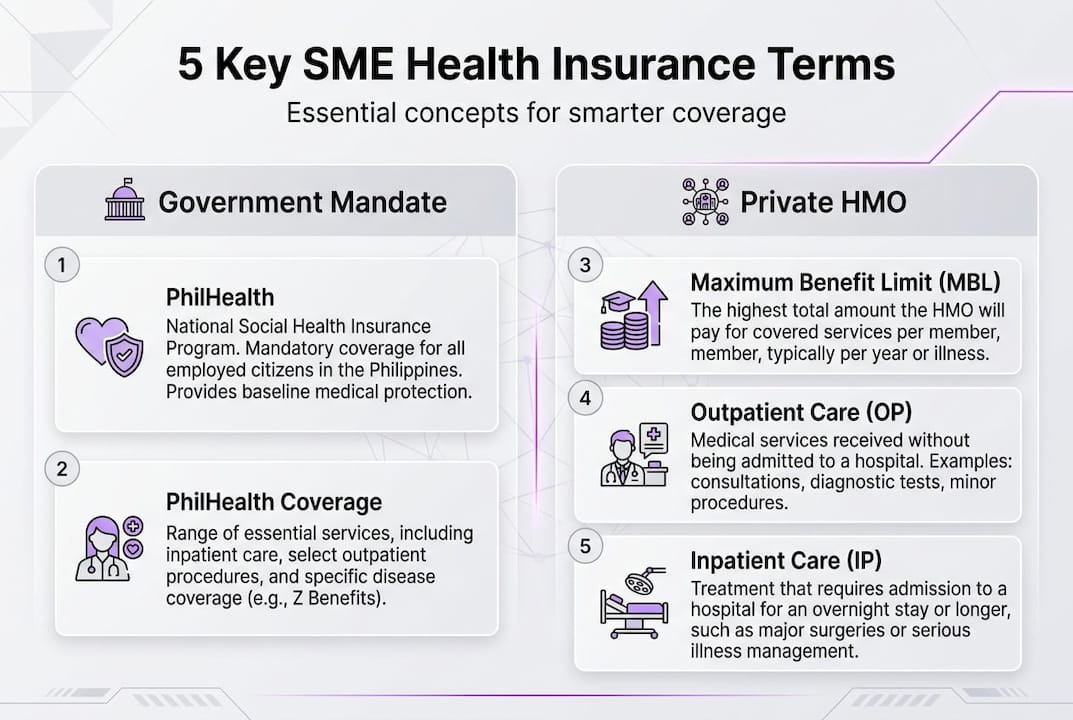

Core health insurance terms every SME must know

Now that you see why clear understanding matters, let’s break down the key terms you’ll encounter when reviewing SME health insurance options. These are not just definitions. They are the building blocks that determine what your employees actually get covered for and what comes out of your pocket.

HMO (Health Maintenance Organization): A private health plan that gives your employees access to a network of hospitals and clinics. Members pay a fixed premium, and the HMO covers medical costs up to a set limit. As noted in SME HMO insurance basics, HMOs control costs through a prepaid cap and network structure, which is key to SME financial stability.

PhilHealth: The government-mandated health insurance program. All employers in the Philippines must contribute. It covers basic hospitalization and certain outpatient procedures, but it has significant gaps for serious or chronic conditions.

MBL (Maximum Benefit Limit): The total amount your HMO will pay per member per year. Once this ceiling is reached, the employee pays out of pocket. Choosing the right MBL for your team size and health profile is one of the most important decisions you’ll make.

OP/IP (Outpatient/Inpatient): Outpatient means treatment without overnight hospital admission. Inpatient means the employee is admitted and stays at least one night. Most HMO plans cover both, but limits and procedures differ.

Pre-existing condition (PEC): Any illness or diagnosis that existed before the start of the insurance policy. This is where most SME owners get surprised. Many plans limit or delay coverage for PECs.

Waiting period: The time between policy start and when coverage for certain conditions kicks in. This is especially relevant for PECs.

Coverage exclusions: Specific conditions, procedures, or situations the plan will not pay for. Always read this section carefully in any policy document.

Here is a quick reference list of the most common terms:

- HMO: Private health plan with network access and a fixed annual premium

- PhilHealth: Government baseline coverage, mandatory for all employers

- MBL: The annual coverage ceiling per member

- OP/IP: Outpatient vs. inpatient treatment categories

- PEC: Pre-existing condition, often subject to waiting periods

- Exclusions: What the plan will not cover

- Waiting period: Delay before certain benefits activate

Understanding these terms also directly connects to employee productivity and retention. Employees who feel protected are more engaged and less likely to leave. You can explore more definitions in the health insurance glossary to keep building your knowledge.

Pro Tip: When reviewing any policy, go straight to the exclusions page first. It tells you more about what you are actually buying than the benefits summary ever will.

Comparing main health insurance options: PhilHealth vs HMO

With the basics covered, it is time to see how your main insurance options compare for your business. Both PhilHealth and private HMOs serve different roles, and using them together is where the real value lives.

| Feature | PhilHealth | Private HMO |

|---|---|---|

| Type | Government mandate | Private plan |

| Premium | Income-based contribution | Fixed annual rate |

| Core coverage | Basic hospitalization, select OP | Full IP/OP, emergency, dental (add-on) |

| Network | Government and accredited hospitals | Accredited clinics, Big 9 Hospitals |

| Exclusions | Many chronic and specialist services | Varies by plan and provider |

| SME value | Baseline, legally required | Fills gaps, boosts retention |

| Flexibility | None | High, customizable |

PhilHealth is foundational but has real gaps. As shown in integrating HMO and PhilHealth, private HMO plans are what fill those gaps for most SMEs. Relying on PhilHealth alone leaves your employees exposed to major out-of-pocket costs for specialist visits, advanced diagnostics, and extended hospital stays.

On cost, the HMO vs PhilHealth breakdown shows that individual HMO premiums typically range from ₱5,000 to over ₱80,000 per year. Group plans for SMEs bring that rate down considerably, making comprehensive coverage far more accessible than most owners expect.

Pro Tip: Stack PhilHealth and a private HMO together. PhilHealth handles the baseline, and your HMO picks up the rest. This layered approach cuts gaps and protects your team from surprise bills. Check out more health insurance guides to see how other SMEs are structuring their benefits.

Pre-existing conditions, exclusions, and underwriting for SMEs

Having weighed which plan fits your SME, you will want to dig into how coverage for existing health risks and exclusions actually works. This is the section most business owners skip, and it is exactly where costly surprises come from.

Typical waiting periods for pre-existing conditions run 12 to 24 months, and high-risk applicants may face outright denial. Here is a summary of how this plays out:

| Condition type | Typical waiting period | Coverage status |

|---|---|---|

| Diabetes | 12 to 24 months | Often limited or excluded |

| Asthma | 12 months | Usually covered after waiting period |

| Congenital conditions | 12 to 24 months | Varies by provider |

| Hypertension | 12 to 24 months | Covered after waiting period |

| Cancer (prior diagnosis) | May be permanently excluded | Depends on plan |

Understanding these timelines helps you set honest expectations with your team. Common reasons claims get denied include:

- Non-disclosure of a known health condition at enrollment

- Treatment for a condition still within the waiting period

- Procedures listed as permanent exclusions in the policy

- High-risk status flagged during underwriting

- Using out-of-network providers without prior authorization

“Non-disclosure can result in claim denial. Always discuss complete health history with your insurer before signing.”

For SME owners, the practical move is to ask your provider for a full list of inclusions and exclusions in writing before committing. Walk your employees through what is and is not covered so they do not find out the hard way. Explore beyond PhilHealth strategies to see how other businesses are managing PEC coverage gaps with smarter plan structures.

Cost control, group benefits, and recent trends for Philippine SMEs

With exclusions and definitions clear, SME owners are ready for actionable strategies to control costs and strengthen employee benefits. The good news is that smart planning, not bigger budgets, is what separates well-protected teams from underinsured ones.

Medical inflation is running 3 to 4 times higher than general inflation in the Philippines, which means doing nothing is actually the most expensive option. Group HMO plans spread that risk across your employee pool and unlock lower per-head rates.

Here are the top steps to take right now:

- Pool your employees. Even small teams of five or more can qualify for group rates. The larger the group, the better the premium.

- Evaluate your plan every year. Health needs change. A plan that worked in 2024 may leave gaps in 2026.

- Layer PhilHealth with a private HMO. This is the most cost-efficient structure for most SMEs.

- Communicate benefits clearly. Employees who understand their coverage use it better and value it more.

- Look at current SME health trends to stay ahead of rising costs and evolving employee expectations.

One trend worth noting: employees increasingly value strong HMO benefits over incremental salary increases. Retention and productivity evidence shows that robust health coverage ranks among the top drivers of employee loyalty in the Philippines. A well-structured plan is a recruitment tool, not just a compliance checkbox.

Pro Tip: Ask your HMO provider about multi-year rate locks or flexible packages. Locking in today’s rates protects your budget from future medical inflation and makes long-term planning far more predictable.

A fresh perspective: Focusing on value, not just price, in SME health insurance

Most SME owners approach health insurance the same way they approach buying office supplies: find the cheapest option that checks the box. That mindset is understandable, but it is also why so many businesses end up with plans their employees barely use or trust.

The real return on investment in health insurance is not the premium you save. It is the sick days avoided, the talent you keep, and the trust you build with your team. When employees know their employer chose a plan that actually covers them, including conditions they already have, that loyalty compounds over time.

We have seen this play out across industries. SMEs that invest in understanding their plan terms, and choosing coverage that reflects their team’s actual health profile, consistently outperform those that buy on price alone. How insurance boosts business ROI is not a theory. It shows up in lower turnover, higher morale, and a reputation that attracts better candidates.

“Smart SMEs don’t just save. They invest in lasting protection and happier, healthier teams.”

Insurance is not a cost center. It is a people strategy.

Get started: Flexible SME health plans that truly fit your team

Ready to apply these insights? Here’s where to find flexible SME health insurance solutions that match what you have just learned.

At HMO Plans, we work with SMEs across the Philippines to build plans that are clear, affordable, and actually cover what your team needs, including pre-existing conditions up to the MBL. No confusing fine print. No generic packages. Our HMO plan features are designed specifically for businesses like yours, with options to add dental, annual physical exams, and life insurance as your team grows. Onboarding is straightforward, and our team walks you through every term before you sign. Take the first step and get an SME HMO quote today.

Frequently asked questions

What is the typical cost of HMO coverage for Philippine SMEs?

HMO premiums range from ₱5,000 to over ₱80,000 per year per individual, but group coverage for SMEs can significantly lower the per-head rate depending on team size and plan tier.

How long is the waiting period for pre-existing conditions?

Most Philippine HMO plans carry a 12 to 24-month waiting period before pre-existing conditions are covered, though some providers offer earlier access with specific plan structures.

Are dependents and part-time employees covered under SME health insurance?

Most SME HMO plans allow minors and adult dependents to be added, and part-time staff may qualify for coverage with pro-rated benefits depending on the provider’s terms.

Why is it important to declare complete health history for employees?

Non-disclosure of health conditions can lead to outright claim denial, meaning your employee pays the full bill for a condition the plan would have covered if it had been properly declared at enrollment.

Recommended

- 2025 Health Trends for SMEs in the Philippines: Key Strategies for Smarter Benefits

- The Better HMO Plans for SMEs | Purple Cow | Features | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- SME Year-End Health Benefits Check-Up: Ensuring Coverage & Readiness for 2025

- The Better HMO Plans for SMEs | Purple Cow | Member Services | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- Insurance & Mental Health Access: 85% CA Telehealth Coverage - ReviveHealthTherapy