Protect your team: Why SMEs need supplemental accident cover

TL;DR:

- SSS EC only covers work-related injuries, leaving off-duty accidents financially unprotected.

- Supplemental accident insurance provides quick, lump-sum payouts for all accidents, regardless of location.

- Adding supplemental coverage enhances employee safety, morale, and business continuity beyond statutory requirements.

Most SME owners in the Philippines assume that SSS Employee Compensation (EC) has their workforce covered. It’s mandatory, the employer funds it, and it pays out when someone gets hurt on the job. That assumption feels safe — until an employee fractures a wrist in a weekend road accident, or slips at home the night before a major project deadline, and the claim gets denied. SSS EC only covers what happens at work or because of work. Everything else falls through the gap. This guide walks you through what that gap actually costs, what supplemental accident cover does to close it, and how to make a smart decision for your business.

Table of Contents

- Understanding SSS EC and its limitations

- What is supplemental accident cover and how does it work?

- Practical benefits for SMEs: Beyond the basics

- How to assess and implement supplemental accident coverage

- Our take: What most SME leaders miss about accident coverage

- Next steps: Protect your workforce with better plans

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SSS EC gaps | Statutory SSS EC only covers work-related injuries, leaving many risks unaddressed. |

| Wider protection | Supplemental accident cover pays out for off-the-job incidents, offering broader security. |

| Fast, simple claims | Supplemental policies provide lump sums quickly and don’t require proving a work connection. |

| Business continuity | Protecting employees with added coverage avoids costly disruptions and strengthens workforce morale. |

| Compliance is essential | Supplemental cover complements but does not replace statutory SSS EC obligations for SMEs. |

Understanding SSS EC and its limitations

Before you can fix a gap, you need to see it clearly. SSS Employee Compensation is a statutory benefit program in the Philippines, meaning the law requires every employer to fund it. Employees contribute nothing. The entire premium sits on the employer’s side, and in exchange, covered workers receive benefits when they suffer a work-related injury or illness.

The core benefits under SSS EC include:

- Temporary Total Disability (TTD): Daily cash allowance when an employee cannot work temporarily due to a covered injury.

- Permanent Partial Disability (PPD): A monthly pension or lump sum when an injury permanently reduces a worker’s capacity, such as the loss of a finger or partial hearing.

- Permanent Total Disability (PTD): A lifetime monthly pension for injuries that permanently prevent any gainful employment.

- Medical benefits: Reimbursement for hospitalization, surgery, and rehabilitation directly tied to the covered incident.

Here is a simplified look at how SSS EC benefit formulas and their key limitations compare:

| Benefit type | Basis of computation | Key exclusion |

|---|---|---|

| TTD | 90% of average daily salary credit | Non-work incidents |

| PPD | Based on injury grade schedule | Injuries outside work premises or hours |

| PTD | Monthly pension formula | Pre-existing conditions |

| Medical | Actual cost, subject to limits | Off-duty accidents |

| Death benefit | Pension for dependents | Non-occupational illness |

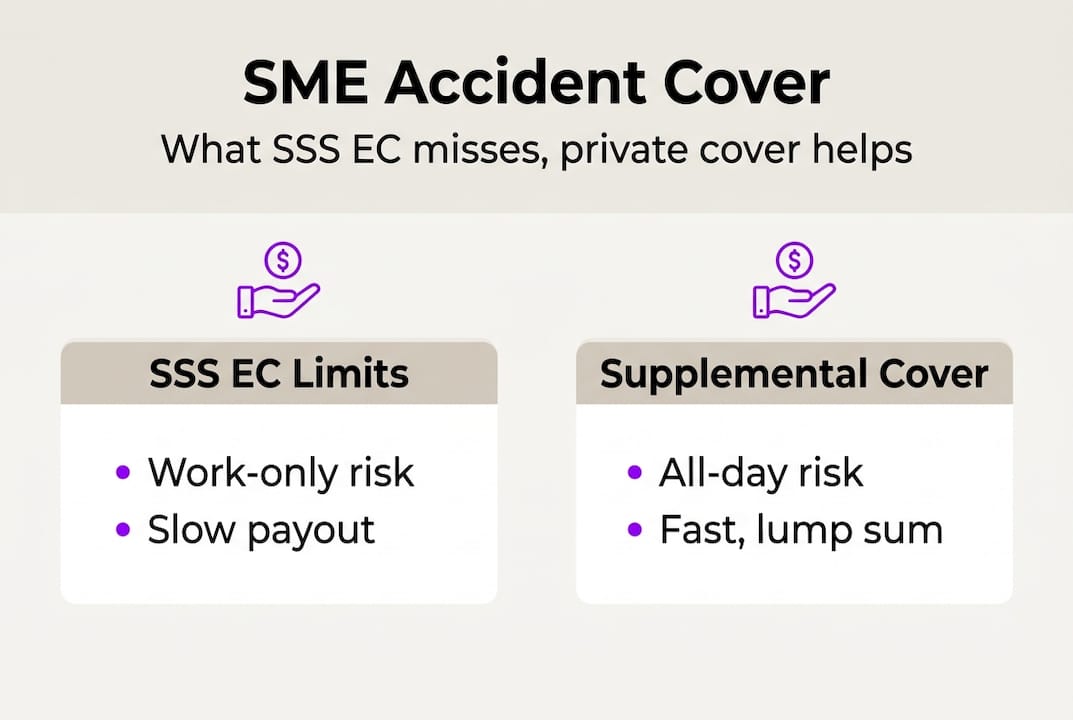

Key fact: SSS EC covers only work-related injuries and illnesses. Any accident that happens off the clock, off the premises, or outside a direct work function is simply not covered, no matter how serious.

This is where many SME owners get surprised. They see the EC deduction on the payroll register and assume it handles all accident scenarios. It does not. Non-compliance with SSS EC filing requirements also exposes SMEs to penalties and back payments, which is a separate risk entirely. But even full compliance with SSS EC leaves a wide-open door for accidents that happen during a commute, at home, or in the community.

For a broader look at SME health coverage basics, it helps to understand how statutory benefits like SSS EC fit alongside private plans. And if you want a deeper breakdown of private options, the life and accident insurance guide on our site explains the landscape well.

The honest reality is that non-work accidents are common. Road incidents, falls at home, sports injuries, and community accidents happen to working adults every single day. When they do, SSS EC pays nothing. Your employee is left to manage financially on their own, or worse, they come to you asking for help because there is no other safety net.

What is supplemental accident cover and how does it work?

Supplemental accident cover is a private insurance policy, usually purchased by the employer as a group plan, that pays out benefits when an employee is injured in an accident regardless of whether that accident happened at work or not. That single distinction changes everything.

Where SSS EC requires the incident to be directly connected to employment, supplemental private accident cover complements the statutory system by covering non-work accidents and providing lump sum payments without requiring proof of work connection. The claim process is simpler, faster, and does not involve the bureaucratic burden of proving the accident was job-related.

Here is how SSS EC and supplemental cover compare side by side:

| Feature | SSS EC | Supplemental accident cover |

|---|---|---|

| Scope | Work-related only | All accidents, work or personal |

| Funding | Employer-funded, mandatory | Employer-funded, voluntary |

| Payout type | Pension or scheduled benefit | Lump sum |

| Claim speed | Weeks to months | Days to weeks |

| Proof required | Must prove work connection | Accident documentation only |

| Coverage for commute | Limited | Usually included |

Making a supplemental accident claim is generally straightforward. Here is the typical process:

- Report the accident to your HR team or designated insurance coordinator as soon as possible after the incident.

- Gather documentation including the medical certificate, hospital receipts, and an accident report or police report if applicable.

- Submit the claim form provided by your insurer, along with the supporting documents.

- Await assessment by the insurance provider, which typically takes a few business days for straightforward claims.

- Receive the lump sum directly into the employee’s account or through the employer, depending on the policy structure.

Pro Tip: When comparing supplemental accident policies, prioritize ones with a streamlined digital claims process. A policy that requires weeks of back-and-forth paperwork defeats the purpose for your employees who need fast financial support after an accident.

For SMEs, the speed of payout matters enormously. An employee who receives a lump sum within a week of an accident can focus on recovery instead of worrying about rent or family expenses. That financial stability translates directly into faster return to work and reduced disruption to your operations. If you are managing complex coverage needs across a diverse team, supplemental accident cover is one of the cleaner add-ons to layer in.

The right accident insurance for SMEs should feel like a natural extension of your existing HMO plan, not a separate administrative burden.

Practical benefits for SMEs: Beyond the basics

So what does adding supplemental accident cover actually achieve for real SMEs day to day? The business case goes well beyond just “doing the right thing.”

Here are the core operational benefits:

- Reduced absenteeism: Employees who receive fast financial support after accidents recover with less stress and return to work sooner.

- Better employee morale: Knowing the company has their back outside of work hours builds genuine loyalty.

- Talent retention: In competitive hiring markets, group accident coverage is a visible differentiator that candidates notice.

- Business continuity: When key staff are injured, a fast payout reduces the chance they leave permanently due to financial pressure.

- Reduced informal requests: Employees are less likely to approach management for emergency loans or advances when they have insurance support.

The gap in SSS EC becomes very real when you look at actual claim scenarios. Consider a delivery coordinator at a Manila-based SME who is injured in a motorcycle accident on a Saturday afternoon. SSS EC denies the claim because the incident was not work-related. The employee misses three weeks of work. Without supplemental cover, that employee absorbs the entire financial burden alone. With a group accident policy, a lump sum arrives within days, the employee focuses on recovery, and the business retains a trained team member.

A second scenario: a sales executive slips and fractures an ankle while attending a community event on a Sunday. Again, SSS EC does not apply. The recovery takes six weeks. Without supplemental cover, this employee may look for a new employer that offers better protection. With it, the company demonstrates real commitment to workforce welfare.

Supplemental cover mitigates risk but does not replace the employer’s statutory duty under SSS EC. Both are necessary. Supplemental is an enhancement, not a compliance shortcut.

Pro Tip: Schedule an annual audit of your insurance portfolio to check for gaps that SSS EC’s limits expose. A quick review of denied claims from the past year often reveals patterns that supplemental cover could address.

It is also worth noting that offering supplemental accident coverage sends a message to prospective hires. In industries like tech, logistics, and hospitality, where talent competition is fierce, group accident coverage signals that your company invests in people, not just productivity. If you want to review your health plans with fresh eyes, that annual audit is the best starting point.

How to assess and implement supplemental accident coverage

Knowing the benefits, how do you decide if and when to add supplemental accident cover and make it work for your business?

Start with a structured evaluation:

- Review your injury history for the past three years. Look at what types of incidents occurred and whether SSS EC covered them. If you see a pattern of off-duty or commute-related injuries, the gap is already costing you.

- Read your current policy documents carefully. Most SME owners have not read their existing coverage in detail. Identify exclusions explicitly.

- Survey your employees. Ask whether they feel protected outside of work hours. The answers will surprise you and give you data to justify the investment.

- Benchmark with industry peers. Talk to other SME owners in your sector about what accident coverage they carry. If competitors offer supplemental cover and you do not, that gap affects your hiring.

- Consult an insurance specialist. A broker or HMO advisor can model the cost of a group accident policy against the estimated cost of uninsured incidents.

When comparing accident policies, look for these specific features:

- Coverage breadth: Does it cover road accidents, home accidents, sports injuries, and community incidents?

- Exclusion list: Are there carve-outs for pre-existing conditions or specific activities your employees commonly do?

- Claim process: Is it digital? How many days does payout typically take?

- Reimbursement speed: Fast payment matters more than a high benefit limit that takes months to arrive.

- Group pricing: Per-employee costs drop significantly with group plans, making this accessible even for teams of ten to thirty people.

Aligning coverage with your workforce type also matters. Field workers, delivery riders, and construction staff face dramatically higher accident exposure than office-based employees. You might choose a tiered approach where field roles carry higher benefit limits, while office staff receive a standard group plan. Both groups benefit, and the cost remains manageable.

For implementation, follow this checklist:

- Select a provider with clear group accident policy terms and a responsive claims team.

- Brief employees on what the policy covers, how to file a claim, and who to contact.

- Distribute a one-page claims process handout so employees are not scrambling for information during a stressful moment.

- Integrate the policy into your employee onboarding materials so new hires understand their coverage from day one.

To maximize SME health investments, supplemental accident cover works best when it is part of a layered strategy that includes your HMO plan, PhilHealth, and SSS EC. Explore the full range of key HMO features to understand how these layers fit together.

Supplemental private cover complements but does not replace SSS EC. Compliance with the statutory system remains mandatory. The goal is to build on top of it, not around it.

Our take: What most SME leaders miss about accident coverage

Here is the uncomfortable truth most insurance articles skip over. Many SME owners treat workforce coverage as a compliance exercise. They fund SSS EC because the law says so, and they stop there. The logic is understandable: keep costs low, stay compliant, move on. But this framing misses the actual business risk.

The real cost of an uncovered accident is not just the employee’s medical bill. It is the lost productivity, the recruitment cost if that employee leaves, the morale dip when colleagues see a coworker struggle financially after an injury, and the reputational damage in your industry’s talent pool.

The most resilient SMEs we see treat workforce coverage as a business continuity investment. They ask not “what is the minimum we must provide?” but “what would an uncovered accident actually cost us?” When you run that number honestly, supplemental accident cover almost always pays for itself.

Integrating supplemental coverage also sets your business apart in recruitment. Candidates talk. When your employees tell their networks that your company covered them after a weekend accident, that story spreads. Visit comprehensive protection for SMEs to see how a layered approach to coverage can become a genuine competitive advantage.

“Supplemental accident cover isn’t just an employee perk — it’s smart risk management for SMEs determined to thrive.”

Next steps: Protect your workforce with better plans

You now understand the gap between SSS EC and real-world accident risk. Closing that gap with supplemental accident cover is one of the most cost-effective workforce investments an SME can make. When paired with a comprehensive HMO plan, it creates a protection layer that handles everything from routine medical care to unexpected accidents at any hour of the day.

At HMO Plans, we design coverage specifically for SMEs in the Philippines. Our group plans include optional life and accident insurance add-ons that integrate seamlessly with your existing HMO. Explore the full range of SME HMO features to see what is available, connect with our team through SME member support for personalized guidance, or visit HMO Plans to review SME-specific health solutions built around your workforce’s real needs.

Frequently asked questions

What does SSS EC actually cover for employees?

SSS EC covers only work-related injuries or illnesses, paying benefits like disability pensions or medical reimbursements tied directly to job-related incidents.

Can supplemental accident insurance replace SSS EC requirements?

No. Supplemental cover mitigates risk but does not remove the employer’s legal obligation to comply with SSS EC, which remains mandatory for all registered businesses.

How do supplemental accident policies pay out claims?

Most pay lump sums rapidly and do not require proof that the accident was work-related, making the claims process significantly faster and simpler than SSS EC.

Are supplemental plans expensive for SMEs?

Group accident policies are generally affordable, particularly when compared to the uninsured costs of a single serious accident, but pricing varies by provider, team size, and coverage scope.

Do all employees need supplemental accident cover?

Ideally yes, but SMEs with limited budgets often prioritize field staff, delivery roles, or any positions with higher daily accident exposure as a practical starting point.

Recommended

- The Better HMO Plans for SMEs | Purple Cow | Home | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- Special Procedures & Complex Coverage Explained: Protecting Every Employee’s Health Needs

- Health Coverage for SMEs in the Food & Beverage Industry

- Life & Accident Insurance: Securing Your Team’s Future with Smarter Coverage