Step-by-step HMO enrollment guide for SMEs: 5 key steps

Enrolling your employees in an HMO plan sounds simple until you’re buried in document checklists, provider jargon, and compliance questions with no clear starting point. For SME owners and HR managers in the Philippines, the stakes are real: a missed requirement delays coverage, a wrong plan tier wastes budget, and poor communication triggers employee disputes. Getting this right matters for retention, legal compliance, and your team’s wellbeing. This guide walks you through every step of the process, from eligibility checks to plan activation, so you can move forward with confidence and avoid the costly mistakes that slow most SMEs down.

Table of Contents

- What you need before you start: eligibility, documents, and options

- The HMO enrollment process: a clear step-by-step walkthrough

- PhilHealth and HMO: optimal coordination for higher coverage and compliance

- Adding employees, dependents, and special enrollment cases

- What most SMEs miss about HMO onboarding: practical truths from the field

- Find the right HMO plan for your SME

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Prepare documents early | A complete masterlist and company papers speed up the HMO enrollment process. |

| Coordinate PhilHealth and HMO | Activating PhilHealth first ensures full coverage and compliance for your employees. |

| Communicate dependent rules clearly | Explain eligibility and costs for dependents upfront to avoid employee disputes. |

| Leverage digital tools | Using HMO digital enrollment and HR platforms reduces errors and improves efficiency. |

What you need before you start: eligibility, documents, and options

Before you request a single quote, you need to confirm your company qualifies and that your paperwork is in order. Skipping this step is the number one reason SMEs experience delays during enrollment.

To qualify for a group HMO plan, your business must have a minimum headcount. SME HMO requirements typically start at 5 to 10 principal employees, and enrollment relies on an official employee masterlist rather than informal records. This matters because providers verify your headcount before issuing a formal proposal.

Standard documents you’ll need to prepare:

- SEC or DTI business registration certificate

- BIR certificate of registration

- Complete employee masterlist with full names, birthdates, and positions

- Proof of PhilHealth membership for all enrollees

- Dependent information sheets (for employees adding family members)

For a smoother intake process, review the intake documentation steps to understand how providers organize and verify submitted records.

Once documents are ready, you’ll choose a plan tier. Most providers offer tiered structures with annual benefit limits ranging from roughly ₱70,000 at the entry level up to ₱250,000 at premium tiers. Here’s a quick summary of what each tier typically covers:

| Plan tier | Annual benefit limit | Best for |

|---|---|---|

| Bronze | ₱70,000 | Startups, tight budgets |

| Silver | ₱100,000 | Growing SMEs |

| Gold | ₱150,000 | Mid-size teams |

| Platinum | ₱250,000 | Full coverage priority |

Pro Tip: Use digital HMO enrollment tools to build and manage your masterlist digitally from day one. Errors in employee data are the most common source of enrollment delays, and a digital record reduces manual mistakes significantly.

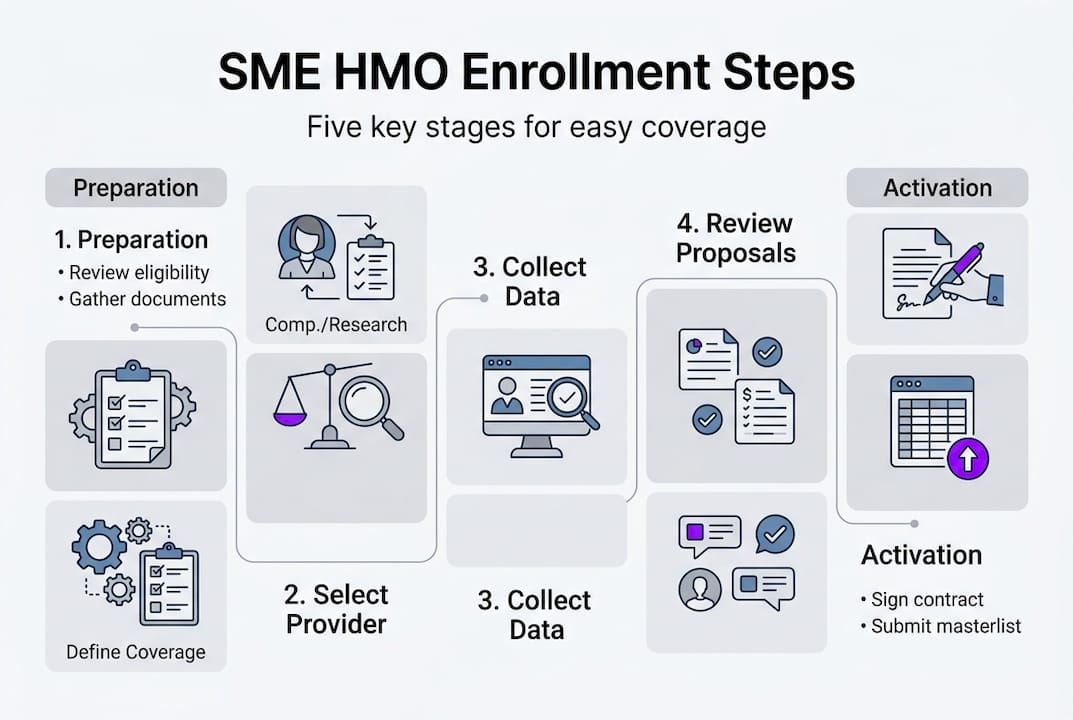

The HMO enrollment process: a clear step-by-step walkthrough

With your requirements in hand, you’re ready to move through the enrollment. Here’s exactly how each step unfolds.

The detailed SME HMO process follows a consistent pattern across most providers: contact, submit, verify, sign, pay, and activate. Failure to submit complete data is the top cause of SME enrollment delays, so treat each step as a checkpoint rather than a formality.

- Request quotes from at least two or three providers. Share your headcount, preferred tier, and any add-ons like dental or annual physical exams.

- Finalize your employee and dependent lists. Confirm all names, dates of birth, and relationships are accurate before submission.

- Confirm minimum principal count. Providers will verify you meet the 5 to 10 employee minimum before issuing a formal proposal.

- Sign the formal proposal. Review coverage terms, exclusions, and benefit limits carefully before signing.

- Process payment. Most providers require full or partial upfront payment before coverage activates.

- Receive HMO kits. Members get physical or digital ID cards, benefit guides, and accredited hospital lists.

Provider timelines vary. Here’s a general comparison:

| Provider | Typical activation time | Digital enrollment |

|---|---|---|

| Maxicare | 7 to 10 business days | Yes |

| Medicard | 5 to 7 business days | Partial |

| iCare | 10 to 14 business days | Limited |

To activate company coverage, providers require signed agreements, complete masterlists, and dependent hierarchy documentation before issuing member IDs.

Pro Tip: Platforms built around HR automation tools let you track submission status in real time, flag missing documents, and send reminders to employees who haven’t submitted dependent forms. This alone can cut your enrollment timeline by several days.

Reviewing the enrollment intake process used by healthcare providers also helps you understand what happens on the receiving end when your documents arrive.

PhilHealth and HMO: optimal coordination for higher coverage and compliance

Understanding each step is one thing, but SMEs must also work smart by integrating PhilHealth with HMO for seamless coverage and compliance.

PhilHealth is mandatory for all employed workers in the Philippines. It covers case rates first, meaning it pays a fixed amount toward specific diagnoses and procedures before any other insurer steps in. HMO supplements PhilHealth by covering the excess costs and requires proof of PhilHealth membership as a condition of enrollment. This is not optional. If your employees’ PhilHealth contributions are not current, your HMO enrollment can stall.

In 2026, PhilHealth contributions are set at 5% of the monthly basic salary, with a minimum of ₱500 and a maximum of ₱5,000 per month, split equally between employer and employee.

Cost-saving tips for SMEs using both programs:

- Keep PhilHealth contributions updated monthly to avoid enrollment holds

- Choose HMO plans that explicitly coordinate with PhilHealth to avoid paying for duplicate coverage

- Use PhilHealth plus HMO strategies to map out which costs each program covers before finalizing your plan tier

- Review your maximize SME health ROI options annually as your headcount grows

- Assign one HR point person to monitor both PhilHealth and HMO compliance deadlines

HMO is not a statutory benefit in the Philippines, but it has become a baseline expectation for talent retention. Companies that skip it often pay more in turnover costs than they save on premiums.

This coordination mindset is what separates SMEs that get real value from their health benefits budget from those that overpay for overlapping coverage.

Adding employees, dependents, and special enrollment cases

With the basics set, you’ll need to handle additions and special situations. Here’s how to do it correctly and avoid costly HR mistakes.

Adding new hires mid-year and enrolling dependents are the two scenarios that create the most confusion for HR teams. The rules are specific, and getting them wrong can lead to disputes or uncovered claims.

Steps for adding a new hire after initial rollout:

- Confirm the employee’s regularization status. Dependent HMO benefits often begin only after regularization, and salary deductions require written consent from the employee.

- Submit the new hire’s information to your HMO provider within the enrollment window (usually 30 days from hire date).

- Collect dependent documents: birth certificates for children, marriage certificate for spouse.

- File a formal enrollment amendment with the provider.

- Confirm the updated member ID has been issued before the employee’s first clinic visit.

Key rules to keep in mind:

- Probationary employees may have limited or no dependent coverage depending on your plan terms

- The dependent hierarchy typically follows: legal spouse, then legitimate children up to age 21

- Salary deductions for dependent premiums must be documented with a signed authorization form

- Pre-existing conditions are covered under some SME plans, particularly those with 100% MBL coverage commitments, so always verify this before choosing a provider

- HMO premiums paid by the employer are generally tax-deductible as a business expense

For guidance on communicating benefits to employees, especially around dependent eligibility rules, clear written policies prevent most disputes before they start. Reviewing your employee benefits planning calendar annually also helps you anticipate enrollment windows and budget for dependent additions.

For dependent-specific intake documentation, confirm what each provider accepts as proof of relationship to avoid rejected submissions.

Pro Tip: Send a simple one-page benefits summary to every new hire on their first day. Include dependent eligibility rules, enrollment deadlines, and who to contact with questions. This single step eliminates the majority of HR follow-up calls.

What most SMEs miss about HMO onboarding: practical truths from the field

Processes aside, there are lessons that only show up after you’ve been through a few enrollment cycles. These are the ones worth knowing before you start.

The biggest time drain we see is SMEs waiting to finalize their employee masterlist. Teams hold off because a few hires are still pending or a resignation is expected. That delay adds weeks to your onboarding timeline and pushes your coverage start date further out. Submit what you have, then add employees through the amendment process.

Dependent policy clarity is another area where vague rules become legal headaches. Digitalization and uniform procedures boost efficiency, while unclear eligibility rules and data privacy lapses create disputes that are expensive to resolve. Write your dependent policy into your employment contracts, not just your HR handbook.

The ROI of using a single digital process shortcut platform for both PhilHealth and HMO tracking is consistently underestimated. HR teams that manage both programs through one dashboard spend significantly less time on compliance follow-ups and almost never miss a contribution deadline.

Finally, uniform eligibility rules across your workforce lower your legal risk. When one department gets faster dependent enrollment than another due to inconsistent HR practices, you create grounds for grievances. Standardize the rules, document them clearly, and apply them consistently from day one.

Find the right HMO plan for your SME

You now have the roadmap. The next step is choosing a plan that fits your team size, budget, and coverage priorities without getting lost in complicated terms or unnecessary add-ons.

At HMO Plans, we work specifically with SMEs in the Philippines to make this decision straightforward. Our plans, backed by Purple Cow and Etiqa, include 100% coverage for pre-existing conditions, access to the Big 9 Hospitals, and flexible add-ons like dental and life insurance. You can review all SME HMO plan features in one place, or reach out directly through our HMO member services team for personalized guidance. No complicated terms. No guesswork. Just the right plan for your people.

Frequently asked questions

What are the minimum requirements for SME HMO enrollment?

SME HMO plans require 5 to 10 principal employees at minimum, along with company registration documents and a complete, verified employee masterlist. Missing even one document typically delays the entire enrollment process.

How is PhilHealth related to HMO enrollment for SMEs?

PhilHealth proof is required before most HMO providers will activate coverage, since HMO acts as supplemental insurance that kicks in after PhilHealth case rates have been applied to a claim.

Are HMO benefits for dependents automatic?

Dependent benefits require regularization in most cases, and salary deductions for dependent premiums must be supported by a signed written consent form from the employee before they can be processed.

Can HMO plans cover pre-existing conditions for SME employees?

Some SME HMO plans do cover pre-existing conditions up to the Maximum Benefit Limit, so it’s worth confirming this specific detail when comparing providers before you sign any agreement.