Step by step SME health coverage guide for PH businesses

Securing affordable, comprehensive health coverage for your employees shouldn’t feel like solving a puzzle with missing pieces. Many Philippine SME owners struggle with hidden exclusions, pre-existing condition denials, and coverage gaps that leave both employer and employee frustrated. This guide breaks down a clear, systematic approach to selecting and implementing health plans that truly protect your team without breaking your budget.

Table of Contents

- Introduction To SME Health Coverage In The Philippines

- Prerequisites: What You Need Before Starting Your SME Health Coverage Journey

- Stepwise Process For Selecting And Implementing SME Health Coverage

- Common Mistakes And How To Avoid Them

- Expected Results And Success Metrics For SME Health Coverage

- Conclusion And Next Steps For Philippine SME Business Owners

- Discover Flexible HMO Plans Designed For Philippine SMEs

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Comprehensive coverage boosts retention | Plans covering pre-existing conditions increase employee satisfaction and reduce turnover by addressing real healthcare needs. |

| Stepwise selection ensures fit | A structured approach to assessing needs, comparing providers, and customizing add-ons prevents costly mismatches and coverage gaps. |

| Common mistakes cost claims | Over 40% of SME claim denials stem from overlooked pre-existing condition exclusions and inadequate needs assessment. |

| Regular reviews maximize value | Annual plan adjustments based on employee feedback and usage data keep coverage relevant and cost-effective. |

Introduction to SME health coverage in the Philippines

Philippine SMEs face unique challenges when selecting employee health insurance. Your workforce likely spans multiple generations, each with different healthcare priorities. Younger employees might prioritize outpatient and preventive care, while older team members need robust inpatient coverage and medication support.

The unique healthcare landscape and SME challenges require tailored health coverage solutions in the Philippines. Common obstacles include:

- Affordability constraints that force compromises on essential benefits

- Complex provider networks that confuse employees and limit access

- Pre-existing condition exclusions that leave vulnerable employees unprotected

- Hidden policy terms that create surprise claim denials

- Limited transparency around actual coverage limits and out-of-pocket costs

Effective HMO health insurance for SMEs directly impacts your ability to attract and retain talented employees. When your team knows their health needs are genuinely covered, productivity increases and turnover drops. The key is selecting a plan that balances comprehensive benefits with realistic budget constraints while avoiding the traps that plague poorly chosen coverage.

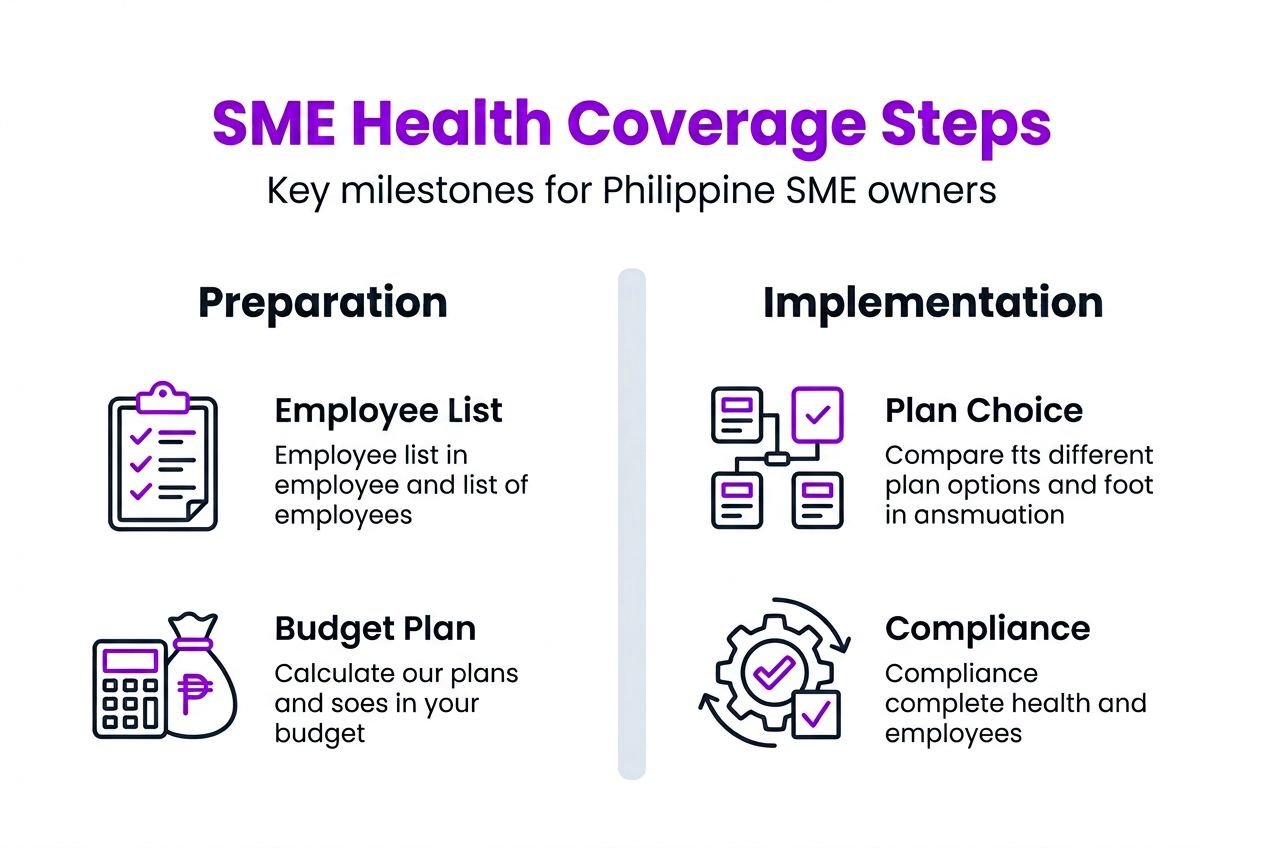

Prerequisites: what you need before starting your SME health coverage journey

Before comparing providers or signing contracts, gather critical information that shapes your decision. Rushing this stage leads to mismatched plans that disappoint employees and waste resources.

Start with an employee health demographics survey. Collect anonymous data on age ranges, chronic conditions, family size, and typical healthcare usage patterns. This snapshot reveals whether your team needs strong maternity benefits, pediatric care, or specialized chronic disease management.

Next, understand basic insurance terminology to avoid confusion:

- Maximum Benefit Limit (MBL): The total amount your plan pays per member annually

- Pre-existing conditions: Health issues diagnosed or treated before plan enrollment

- Exclusions: Specific treatments or conditions the plan doesn’t cover

- Co-payment: Fixed amount members pay per service

- Out-of-network reimbursement: Coverage for non-accredited providers

Pro Tip: Create a simple budget calculator multiplying your employee count by estimated per-head annual premiums, then add 15% for potential add-ons like dental or life insurance.

Assessment of employee health demographics and budget estimation are essential preparation steps before choosing health plans. Prepare enrollment documents including employee lists with birthdates, beneficiary information, and government IDs. Having these ready accelerates the application process once you select a provider.

Finally, establish your decision criteria. Rank priorities like pre-existing condition coverage, hospital network quality, digital access tools, and premium affordability. This framework keeps your selection process objective and aligned with actual employee needs. When you review and adjust health plans later, these same criteria help evaluate performance.

Stepwise process for selecting and implementing SME health coverage

Follow this structured approach to choose and launch health coverage that actually works for your business and employees.

-

Conduct detailed needs assessment: Survey employees about current health concerns, preferred hospitals, and desired benefits. Analyze demographics to predict future healthcare trends in your workforce.

-

Research and compare HMO providers: Evaluating providers on coverage inclusions, networks, and add-ons helps tailor plans matching employee demographics. Create a comparison spreadsheet tracking MBL amounts, hospital networks, exclusions, and premium costs across at least three providers.

-

Verify pre-existing condition coverage: This is your most critical checkpoint. Confirm in writing whether the plan covers pre-existing conditions, congenital issues, and special procedures up to the MBL. Many SMEs discover coverage gaps only when claims get denied.

-

Customize with essential add-ons: Based on your needs assessment, select relevant supplemental benefits. Dental HMO addresses a common employee request. Annual physical exams catch health issues early. Life and accident insurance provides family protection beyond medical care.

-

Complete enrollment documentation: Submit all required paperwork promptly with accurate employee information. Errors delay coverage start dates and frustrate your team.

-

Monitor usage and gather feedback: Track claim volumes, denial rates, and employee satisfaction quarterly. This data drives improvements when you evaluate HMO providers for renewal or changes.

| Evaluation Factor | Weight | Provider A | Provider B | Provider C |

|---|---|---|---|---|

| Pre-existing coverage | 30% | Full | Limited | None |

| Hospital network | 25% | Big 9 + 200 | Big 6 + 150 | Big 9 + 180 |

| Premium cost | 20% | ₱8,500 | ₱7,200 | ₱9,100 |

| Digital tools | 15% | Full app | Basic portal | No digital |

| Add-on options | 10% | 5 choices | 3 choices | 2 choices |

Pro Tip: Request sample policy documents before committing. Read the exclusions section carefully as this reveals what the plan won’t cover, which matters more than marketing promises.

Ensure your selection aligns with PhilHealth compliance requirements to avoid regulatory issues. Many HMO plans supplement PhilHealth coverage, so understanding how they work together maximizes total employee protection.

Common mistakes and how to avoid them

Even well-intentioned SME owners fall into predictable traps when selecting health coverage. Learning from these errors saves money and employee trust.

Ignoring pre-existing condition details: Over 40% of claim denials among SME employees stem from misunderstood pre-existing condition terms. Always get explicit written confirmation about what qualifies as pre-existing and how the plan handles these cases. Some providers exclude pre-existing conditions entirely, while others cover them fully up to the MBL.

Underestimating employee healthcare diversity: Choosing plans based only on healthy young employees ignores the reality that health needs change. One serious illness among staff can reveal massive coverage gaps. Conduct thorough needs assessments that account for both current and potential future healthcare requirements.

Skipping the fine print: Exclusions buried in policy documents often contradict marketing materials. Read every exclusion, limitation, and special condition clause. If something seems unclear, demand written clarification before signing.

Setting and forgetting: Health plans require annual evaluation. Employee demographics shift, medical costs rise, and better options emerge. Schedule regular reviews to ensure your coverage remains optimal. When you’re ready to adjust SME health plans, having usage data makes decisions easier.

Pro Tip: Create a simple one-page summary of your plan’s key coverage points and exclusions. Share this with employees during onboarding so they understand exactly what’s covered before they need care.

Many SMEs also fail to communicate plan details effectively to employees. Your team can’t appreciate benefits they don’t understand. Hold enrollment meetings, provide clear written materials, and designate an internal point person for health plan questions. Following health plan review tips prevents these communication breakdowns.

Expected results and success metrics for SME health coverage

Knowing what success looks like helps you evaluate whether your health coverage investment delivers value. Track these concrete metrics to measure your plan’s effectiveness.

| Metric | Target Benchmark | Measurement Period |

|---|---|---|

| Enrollment completion | 95%+ of eligible employees | 4 weeks from launch |

| Employee satisfaction score | 8/10 or higher | Quarterly survey |

| Claim approval rate | 90%+ first submission | Monthly tracking |

| Average claim processing time | Under 7 business days | Monthly tracking |

| Benefits utilization rate | 60-75% of employees | Annual review |

| Employee turnover rate | 10% reduction year over year | Annual comparison |

Typical enrollment approval timelines run under four weeks from documentation submission to active coverage. Delays usually indicate incomplete paperwork or provider processing backlogs.

Employee benefits utilization typically increases 15 to 20% when you add relevant supplemental options like dental or annual checkups. This jump reflects employees actually using benefits that match their needs rather than avoiding care due to coverage gaps.

Digital claim submission tools improve processing speeds by roughly 30% compared to paper-based systems. Faster approvals mean employees get care sooner and experience less financial stress from medical bills.

Quality HMO health coverage reduces coverage gaps and claim denials by more than 50% when plans explicitly include pre-existing conditions and special procedures. This translates directly to employee trust and satisfaction.

Employee retention often stabilizes or improves within 12 months of implementing comprehensive health coverage. While multiple factors affect turnover, quality healthcare benefits consistently rank among top reasons employees stay with SME employers.

Conclusion and next steps for Philippine SME business owners

Selecting the right health coverage for your SME doesn’t require guesswork or luck. The stepwise approach outlined here provides a clear roadmap from initial needs assessment through implementation and ongoing optimization.

Start by gathering employee health data and establishing your budget parameters. Compare providers systematically using objective criteria that reflect your team’s actual healthcare needs. Verify pre-existing condition coverage explicitly, as this single factor determines whether your plan truly protects vulnerable employees or leaves them exposed.

Customize your base plan with add-ons that address specific gaps revealed by your needs assessment. Monitor usage and satisfaction continuously rather than treating health coverage as a set-it-and-forget-it benefit.

The Philippine SME health insurance landscape continues evolving with new providers and innovative coverage options. Plans like those from Purple Cow demonstrate how comprehensive benefits including full pre-existing condition coverage can fit SME budgets when structured thoughtfully.

Take action now rather than waiting for open enrollment periods or employee complaints to force decisions. Your team’s health and your company’s success both benefit from proactive, informed health coverage choices. The preparation work feels substantial upfront but pays dividends through reduced claim denials, higher employee satisfaction, and genuine peace of mind that your people are protected when they need care most.

Discover flexible HMO plans designed for Philippine SMEs

Your employees deserve health coverage that actually covers their needs without surprise exclusions or denied claims. HMO Plans offers comprehensive protection specifically designed for Philippine SMEs, including 100% coverage for pre-existing conditions, congenital issues, and special procedures up to the maximum benefit limit.

Explore customizable options through our plan features that let you add dental HMO, annual physical exams, and life insurance based on your team’s priorities. Access our extensive network through accredited providers including the Big 9 Hospitals and Healthway Clinics nationwide. Our member services include digital platforms that streamline claims and provide 24/7 support when your employees need assistance. Get straightforward, cost-effective coverage that eliminates complicated terms and delivers real protection.

Frequently asked questions

What documents do I need to enroll my SME in an HMO plan?

You’ll need a complete employee roster with full names, birthdates, and positions. Include photocopies of valid government IDs for each member and beneficiary information forms. Some providers also require your business registration documents and DTI or SEC certificates. Having these ready accelerates approval and prevents enrollment delays.

Why is employee health needs assessment so important?

Assessments reveal the specific healthcare priorities and risks within your workforce. Without this data, you might select plans that don’t match actual usage patterns, wasting money on unused benefits while leaving critical needs uncovered. A simple anonymous survey about chronic conditions, family size, and preferred hospitals guides smarter plan customization. This preparation ensures you review and adjust plans based on real information rather than assumptions.

How much should SMEs budget for comprehensive health coverage?

Plan for ₱6,000 to ₱12,000 per employee annually for quality HMO coverage, with costs varying based on age, coverage levels, and add-ons. Multiply your employee count by your target per-head premium, then add 15% for supplemental benefits like dental or life insurance. Factor in annual increases of 8 to 12% when projecting multi-year costs. Balance affordability with adequate coverage since extremely cheap plans often have exclusions that trigger expensive out-of-pocket costs later.

What key insurance terms should SME owners understand?

Maximum Benefit Limit (MBL) sets the total annual coverage per member. Pre-existing conditions refer to health issues diagnosed or treated before enrollment. Exclusions list specific treatments or conditions not covered by your plan. Room and board accommodation defines hospital room types covered during confinement. Out-of-network reimbursement determines if you get partial payment for non-accredited providers. Understanding these terms prevents surprise denials and helps you compare plans accurately.

How do I verify a plan truly covers pre-existing conditions?

Certain SME health plans offer 100% coverage for pre-existing conditions up to the maximum benefit limit. Request written confirmation in the policy document specifically stating pre-existing condition inclusion. Ask providers to clarify any waiting periods or limitations that might apply. Compare this language across multiple providers since coverage varies dramatically. Don’t rely on verbal assurances during sales calls, demand explicit documentation before signing any agreement. This verification step when evaluating coverage for pre-existing conditions prevents the most common source of claim denials.

What defines adequate hospital network coverage?

Your plan should include at least 150 accredited hospitals and clinics nationwide, with representation in all regions where your employees live and work. Verify access to reputable facilities like the Big 9 Hospitals for serious cases. Check that primary care clinics are conveniently located near your office and residential areas. Out-of-network reimbursement options provide backup when employees need care outside the accredited network, especially important for those in provincial areas with limited facility choices.

What’s the biggest mistake SMEs make with health plans?

Failing to verify exclusions and pre-existing condition coverage leads to devastating claim denials when employees face serious illness. Many SMEs choose plans based solely on premium cost without reading policy details. This creates false security until employees discover their conditions aren’t covered. Always prioritize comprehensive coverage terms over marginal premium savings. Conducting annual reviews to avoid health plan mistakes ensures your coverage remains relevant as your workforce and their needs evolve.

How often should I review and update our SME health plan?

Conduct formal reviews annually before renewal periods, plus informal check-ins quarterly. Track claim volumes, denial reasons, and employee satisfaction through simple surveys. Significant workforce changes like expansion or demographic shifts warrant immediate evaluation. Markets evolve with new providers and better coverage options emerging regularly. Regular assessment ensures your plan adapts to changing needs rather than becoming outdated and ineffective.

Recommended

- PhilHealth Updates & Compliance in 2025: A Guide for SMEs in the Philippines

- The Better HMO Plans for SMEs | Purple Cow | Features | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- The Better HMO Plans for SMEs | Purple Cow | Blog | Rai dela Cruz | Best HMO Plans Philippines - Purple Cow

- Eumir

- Step by Step Diabetes Management: Achieve Daily Control | Diacontext