Supplemental benefits for SMEs in the Philippines: 2026 guide

TL;DR:

- Many Philippine SMEs underestimate the gaps in employee protection beyond mandatory contributions like PhilHealth, SSS, and Pag-IBIG.

- Supplemental benefits such as HMO, life insurance, and de minimis items enhance retention, productivity, and legal compliance.

- Proper structuring, documentation, and regular review of benefits are crucial to avoid legal pitfalls and maximize investment.

Most SME owners in the Philippines assume their PhilHealth, SSS, and Pag-IBIG contributions are enough to keep employees healthy and protected. They’re not. Mandatory contributions cover the legal baseline, but they leave real gaps in hospital costs, specialist visits, and emergency care. Meanwhile, HR teams often blur the line between what the law requires and what the company is voluntarily providing, which creates budget waste, compliance exposure, and frustrated employees. This guide cuts through that confusion. You’ll walk away with a clear definition of supplemental benefits, a practical framework for structuring them, and the legal guardrails every Philippine SME needs to know.

Table of Contents

- What are supplemental benefits?

- Why supplemental benefits matter for SMEs

- Structuring and funding supplemental benefits for your SME

- Compliance, legalities, and common pitfalls for SMEs

- Our hard-won lessons: What most SME benefit plans miss

- How Purple Cow helps SMEs build better supplemental benefits

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Supplemental vs. mandatory | Supplemental benefits go beyond government-mandated contributions and include HMO, group life, and other perks. |

| Strategic advantage | Investing in supplemental benefits helps SMEs win talent, boost retention, and improve compliance. |

| Start cost-effectively | Begin with targeted riders or de minimis perks and scale as your SME grows. |

| Avoid legal pitfalls | Respect the non-diminution rule, document eligibility, and update compliance as regulations change. |

| Partner with experts | Working with trusted providers simplifies plan design, funding, and legal compliance. |

What are supplemental benefits?

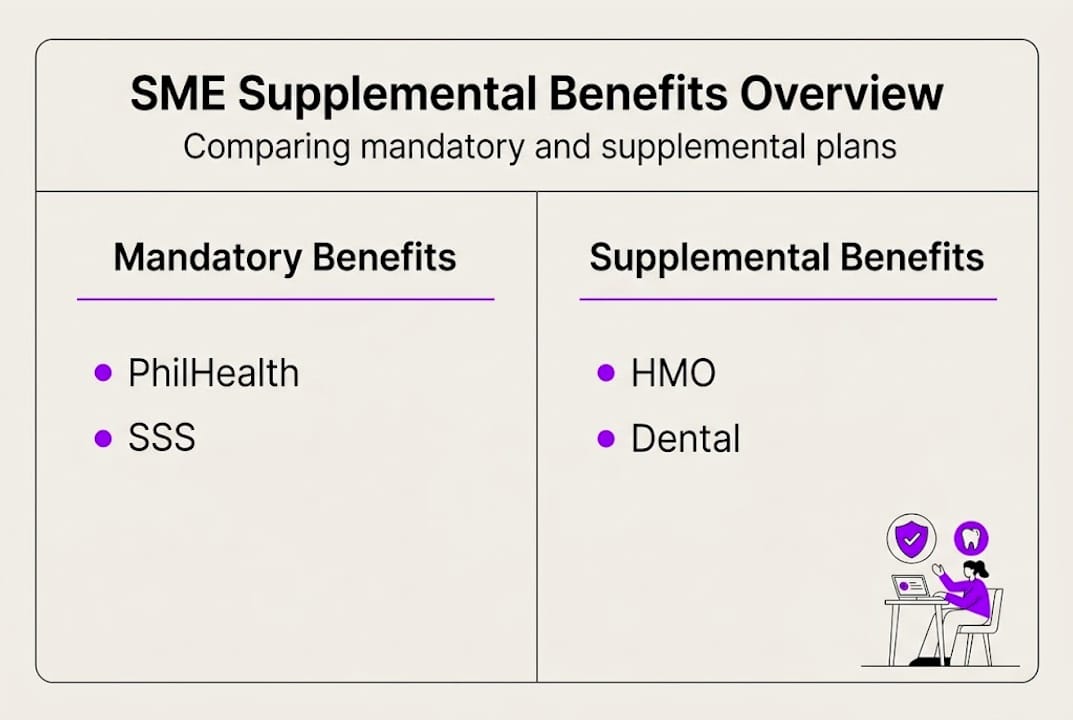

Supplemental benefits are any employee benefits your company provides beyond what the law mandates. In the Philippines, the mandatory floor includes PhilHealth (health insurance), SSS (social security), and Pag-IBIG (housing fund). Everything above that floor is supplemental.

Common supplemental benefits include:

- HMO coverage (private health insurance with cashless access to hospitals and clinics)

- Group life insurance and accident coverage

- De minimis benefits such as rice subsidies (up to PHP 2,000 per month) and meal allowances (up to PHP 25,000 per year)

- Dental HMO plans, which you can explore through HMO dental plans explained

- Annual physical exams and wellness programs

Eligibility typically follows employment status. Most group plans activate after the probationary period, though some SMEs extend limited coverage from day one to attract competitive talent. Dependents, including a spouse, children under 21, and parents over 60, are often covered under group HMO plans with written consent for salary deductions. If you’re new to this space, HMO basics for SMEs is a solid starting point.

Here’s how mandatory and supplemental benefits compare:

| Category | Mandatory benefits | Supplemental benefits |

|---|---|---|

| Required by law | Yes | No |

| Examples | PhilHealth, SSS, Pag-IBIG | HMO, group life, de minimis |

| Tax treatment | Taxable contributions | HMO tax-exempt if broad-based |

| Employer control | Fixed by law | Fully customizable |

| Reduction allowed | No | Only if not yet established |

The mechanics matter here. Employers contract with HMOs or insurers as the policyholder, offering benefits through group plans with eligibility tied to probation or a minimum service period. PhilHealth coordination is required, meaning employees must file PhilHealth claims first before the HMO steps in as secondary coverage.

One legal point every HR manager must know: the non-diminution rule under Labor Code Art. 100 prevents you from unilaterally reducing or removing a benefit once it’s been established by company policy, a collective bargaining agreement (CBA), or consistent practice. This rule also applies to contractors if they are later found to be misclassified as employees, which is a real compliance risk for SMEs that rely heavily on freelancers or project-based workers. Going beyond PhilHealth is smart strategy, but it requires careful planning from the start.

Key takeaway: Once you establish a supplemental benefit through consistent practice, removing it without legal basis can trigger labor complaints. Design your benefits program intentionally.

Why supplemental benefits matter for SMEs

Here’s a reality check: SMEs compete for talent against large corporations that offer full benefit suites. Offering only the mandatory minimum puts you at a structural disadvantage in recruitment. But the case for supplemental benefits goes well beyond hiring.

Consider these strategic reasons:

- Retention. Employees who feel protected by their employer’s health plan are less likely to leave for a marginal salary increase elsewhere.

- Tax efficiency. De minimis benefits like meal allowances up to PHP 25,000 per year and rice subsidies are excluded from taxable income, letting you add real value without inflating the salary base used for SSS and PhilHealth contributions.

- Productivity. Employees with access to outpatient care and preventive health programs take fewer unplanned sick days. Joining health programs consistently links preventive coverage to reduced absenteeism.

- Legal risk reduction. A well-structured supplemental package, documented in your employee handbook, reduces exposure to DOLE complaints and NLRC claims.

- Culture. Benefits communicate values. An SME that invests in employee wellness signals stability and care, which matters enormously in a tight labor market.

For combining PhilHealth and HMO coverage effectively, the key is treating PhilHealth as the foundation and HMO as the structure built on top. The HMO fills gaps like room and board upgrades, specialist fees, and outpatient consultations that PhilHealth does not fully cover.

Pro Tip: Start with a broad-based HMO plan that covers inpatient and outpatient care, then layer in targeted riders like dental or accident coverage as your budget grows. This phased approach, recommended by insurance and CBA benefit specialists, keeps costs manageable while scaling protection meaningfully. You can also explore health benefit strategies tailored to the Philippine SME market.

The ROI on supplemental benefits is real. Even a modest HMO plan that costs PHP 8,000 to PHP 15,000 per employee per year can prevent a single hospitalization from draining your team’s morale and productivity for weeks.

Structuring and funding supplemental benefits for your SME

Knowing why supplemental benefits matter is one thing. Building a plan that actually works for your size, budget, and workforce is another.

Here’s what a well-structured SME supplemental program typically looks like:

| Plan element | Details |

|---|---|

| Eligibility trigger | After probationary period (usually 6 months) |

| Dependents | Spouse, children under 21, parents over 60 |

| Primary coverage | PhilHealth (mandatory, file first) |

| Secondary coverage | Group HMO plan |

| Optional add-ons | Dental, life insurance, accident coverage |

| De minimis items | Rice subsidy, meal allowance, uniform |

| Deduction consent | Written authorization required for salary deductions |

Employers contract with HMOs as the group policyholder, with eligibility typically starting after the probation period. Dependents are often included, but written consent for salary deductions is legally required before any premium sharing arrangement.

For sourcing your plan, you have several options:

- Direct HMO contracts with accredited providers

- Insurance brokers who can compare group plans across multiple carriers

- CBA negotiation if your workforce is unionized

- Group enrollment programs like PhilHealth’s group enrollment, which streamlines administration for small employers

Cost control is where many SMEs stumble. The smartest lever is group buying power. Even a team of 10 to 15 employees qualifies for group HMO pricing, which is significantly lower than individual plan rates. Pair that with de minimis benefits to add non-cash value without increasing the salary base for mandatory contributions.

Pro Tip: Review your benefit structure annually, not just when renewals come up. Use your year-end health plan review to check utilization data, identify unused benefits, and adjust coverage before the next enrollment cycle. You can also check SME HMO features to see what a modern group plan should include. For PhilHealth compliance for SMEs, keeping up with contribution rate updates is essential to avoid penalties.

Also consider dental membership programs as a cost-effective add-on. A dental membership guide can help you understand how these plans work before committing to a group dental HMO.

Compliance, legalities, and common pitfalls for SMEs

Supplemental benefits come with legal strings attached. Ignoring them is how SMEs end up facing DOLE complaints or NLRC claims that cost far more than the benefit itself.

The two most important legal concepts are:

Non-diminution rule. Under Labor Code Art. 100, once a benefit is established through company policy, a CBA, or consistent practice, you cannot unilaterally reduce or remove it. This is not just about formal written policies. If you’ve given a Christmas HMO upgrade three years in a row, employees may have a legal expectation of it continuing.

PhilHealth premium sharing. As of 2026, PhilHealth premiums are set at 5% of the monthly basic salary, with a minimum of PHP 500 and a maximum of PHP 5,000 per month, shared equally between employer and employee. HMO coverage is tax-exempt when it is broad-based, meaning it covers all employees rather than just selected executives.

Here are the four most common SME compliance pitfalls:

- Misclassifying contractors as employees (or vice versa). If a contractor is later ruled an employee, your SME may owe retroactive benefits, including HMO coverage and SSS contributions. Review contractor agreements regularly.

- Failing to document established benefits. Verbal promises or informal practices can become legally binding. Put every benefit in writing in your employee handbook.

- Ignoring Insurance Commission (IC) circulars. HMO regulations change. Staying current with IC updates protects you from inadvertent non-compliance.

- Not coordinating PhilHealth and HMO properly. Employees must file PhilHealth claims first. Skipping this step can invalidate HMO reimbursements.

Pro Tip: Update your CBA or employee handbook every time you add or modify a benefit. This protects you under the non-diminution rule and gives employees clear expectations. For a deeper look at maximizing health ROI within compliance boundaries, and for practical HMO for SME legal tips, both resources are worth bookmarking.

Dispute resolution, if it comes to that, runs through DOLE’s SEnA (Single Entry Approach) process first, then escalates to the NLRC. Neither is cheap in time or money, which is exactly why prevention is the only smart strategy.

Our hard-won lessons: What most SME benefit plans miss

After working with SMEs across tech, hospitality, and healthcare, we’ve noticed a consistent pattern. Companies spend on visible perks, team events, or one-off bonuses, while leaving core risk-protection gaps wide open. An employee who can’t afford a specialist visit because their HMO doesn’t coordinate with PhilHealth correctly is not a well-protected employee, regardless of how many free lunches the company provides.

The most effective SME benefit programs we’ve seen share three traits. They start with a broad-based HMO that covers both inpatient and outpatient care. They layer in targeted de minimis benefits for tax efficiency. And they conduct annual reviews with a compliance checklist, not just a cost review.

The biggest blind spot? Regulatory changes. PFRS 17 accounting standards are reshaping how insurers price group plans, and recent labor rulings on misclassification are tightening. SMEs that don’t anticipate these shifts end up scrambling to restructure benefits mid-year. Our expert insights for SMEs cover these developments as they happen, so you’re never caught off guard.

How Purple Cow helps SMEs build better supplemental benefits

Building a compliant, competitive supplemental benefit package is not something most SME HR teams should figure out alone. There are too many moving parts, from PhilHealth coordination to IC compliance to plan customization.

Purple Cow, through HMO Plans, offers curated group HMO plans designed specifically for Philippine SMEs, with 100% coverage for pre-existing conditions, congenital conditions, and special procedures up to the Maximum Benefit Limit. Our HMO member services include compliance support, plan reviews, and access to premier facilities including the Big 9 Hospitals and Healthway Clinics. Explore our Purple Cow HMO features to see how a straightforward, cost-effective plan can close the gaps your current setup may be leaving open. Reach out for a tailored quote today.

Frequently asked questions

What counts as a supplemental benefit for SME employees in the Philippines?

Supplemental benefits include HMO health insurance, group life, accident coverage, and de minimis items like meal or rice allowances beyond mandatory government contributions. They are voluntary but become legally protected once established through consistent practice.

How do SMEs coordinate PhilHealth with private HMO benefits?

SMEs must ensure employees claim from PhilHealth first, then use HMO coverage for any remaining gaps, coordinating with both providers to avoid reimbursement issues.

What is the non-diminution rule for employee benefits?

The non-diminution rule under Art. 100 means SMEs cannot reduce or remove a benefit once it has become established by policy, CBA, or consistent past practice.

Are dependents covered under SME supplemental benefits?

Dependents such as a spouse, children under 21, and parents over 60 are usually covered under group HMO plans, provided the employee gives written consent for any corresponding salary deductions.

What happens if a contractor is misclassified regarding SME benefits?

If misclassified as an employee, a contractor may become entitled to the same benefits retroactively, creating significant financial and legal liability for the SME.

Recommended

- 2025 Health Trends for SMEs in the Philippines: Key Strategies for Smarter Benefits

- PhilHealth Updates & Compliance in 2025: A Guide for SMEs in the Philippines

- Beyond PhilHealth: How SMEs Can Maximize Health Investments for Better ROI

- HMO Health Insurance for Small and Medium Enterprises in the Philippines