Why emergency medical coverage matters for SMEs: 67% stay

TL;DR:

- PhilHealth and SSS provide mandatory emergency coverage but often leave gaps in real emergencies.

- Adding an HMO plan offers cashless, broader outpatient and inpatient protection, boosting employee retention.

- Comprehensive, layered health benefits protect SMEs legally, financially, and competitively in a growing medical inflation environment.

Most SME owners in the Philippines assume that paying PhilHealth and SSS contributions checks every box on employee health protection. Then a real emergency happens. A staff member collapses on-site, gets rushed to a non-accredited hospital, and the bills arrive with gaps that neither PhilHealth nor SSS will fill. Suddenly, that “covered” employee faces five-figure out-of-pocket costs, and you face potential liability. Emergency medical coverage for SMEs in the Philippines is primarily provided through PhilHealth and SSS, with optional HMO plans strongly recommended. This article breaks down your legal obligations, compares every coverage option, and shows you how to build a plan that actually protects your team.

Table of Contents

- What emergency medical coverage means for SMEs

- Comparing PhilHealth, SSS, and HMO plans: Key differences for SMEs

- How comprehensive coverage enhances employee retention and productivity

- Common pitfalls, edge cases, and how SMEs can improve emergency coverage

- Why the bare minimum isn’t really enough: Our perspective

- Take the next step: Strengthen your SME emergency medical program

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Statutory coverage basics | PhilHealth, SSS, and ECC provide required emergency medical support, but often do not cover all potential employee needs. |

| HMO benefits add value | Supplemental HMO plans offer cashless, broader coverage and help SMEs attract and retain quality staff. |

| Legal and practical compliance | Compliance with DOLE OSH rules and contribution documentation reduces costly liability risks for business owners. |

| Layered strategies work best | Combining statutory and voluntary emergency medical coverage gives robust protection and business resilience. |

| Continuous improvement | Regularly review and update your emergency medical coverage to keep pace with medical inflation and changing risks. |

What emergency medical coverage means for SMEs

Emergency medical coverage refers to the financial and logistical support that kicks in when an employee needs urgent medical care, whether that’s a cardiac event, a workplace accident, or a sudden severe illness. For SMEs in the Philippines, this coverage is built on two mandatory government programs and one highly recommended voluntary layer.

PhilHealth is the national health insurance program. Every employer must register employees and remit monthly contributions based on the employee’s basic salary. In 2026, the contribution rate is 5% of monthly basic salary, shared equally between employer and employee, with a salary ceiling of ₱100,000. PhilHealth covers inpatient emergencies through case rates and now extends to outpatient emergencies through the Outpatient Emergency Care Benefit (OECB).

SSS and the Employees’ Compensation Commission (ECC) cover work-related injuries and illnesses. If an employee is injured on the job, the ECC provides medical reimbursement, sickness allowance, and disability benefits. Employer contributions to SSS are mandatory regardless of company size.

Beyond contributions, the Department of Labor and Employment (DOLE) Occupational Safety and Health (OSH) Law requires SMEs to maintain:

- First-aid trained personnel on-site

- A first-aid kit accessible to all employees

- A designated clinic or hospital tie-up for emergencies

- An OSH officer (part-time for smaller firms, full-time for larger ones)

Here’s a quick look at the statutory requirements:

| Requirement | Governing body | Penalty for non-compliance |

|---|---|---|

| PhilHealth contributions | PhilHealth | Surcharges plus legal action |

| SSS/ECC contributions | SSS | Penalties plus criminal liability |

| OSH first-aid and clinic tie-up | DOLE | ₱40,000 to ₱100,000 per day |

For a deeper look at staying current with contribution rates, the PhilHealth compliance guide is a solid starting point. You can also review labor law insights for employer liability specifics.

Pro Tip: Keep a dedicated folder, physical or digital, with all remittance receipts, OSH documentation, and hospital tie-up agreements. If a DOLE inspection or a legal claim ever surfaces, this paper trail is your first line of defense.

The statutory minimums protect you legally. But they rarely protect your employees fully in a real emergency. That gap is exactly where the next section becomes critical.

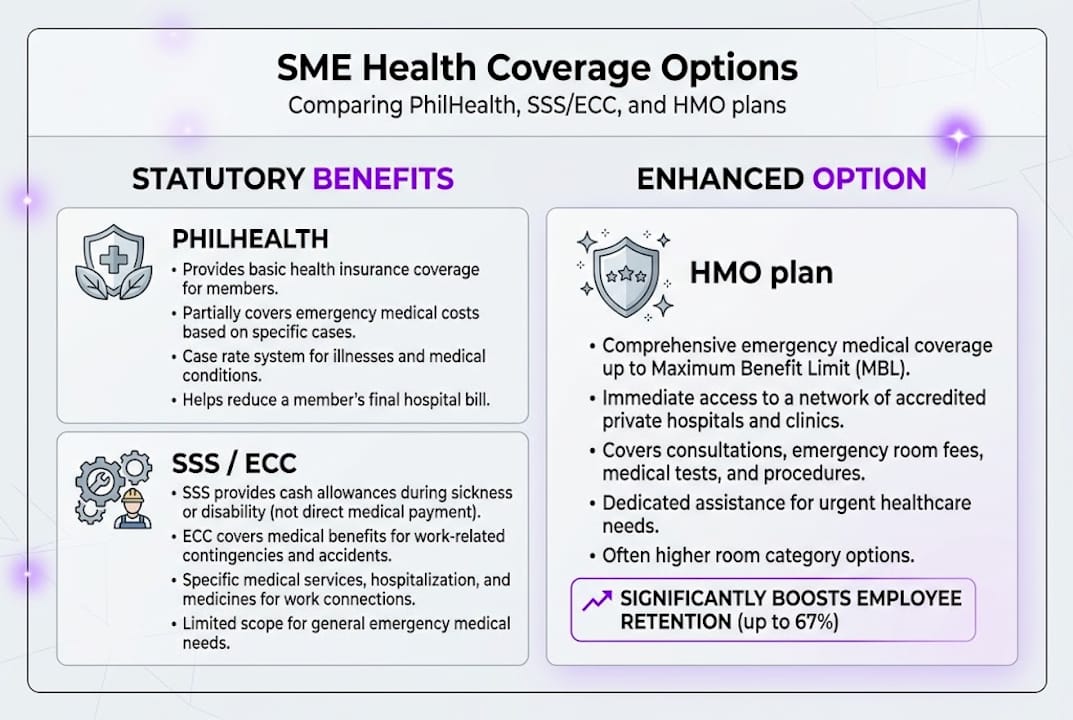

Comparing PhilHealth, SSS, and HMO plans: Key differences for SMEs

Understanding what’s mandatory is just the start. Knowing how each coverage option works side by side is how you make informed, cost-effective decisions.

PhilHealth covers inpatient emergencies via case rates and outpatient emergencies through the OECB, SSS/ECC handles work-related accidents, and HMOs provide cashless and non-accredited facility cover. Here’s how they stack up:

| Feature | PhilHealth | SSS/ECC | HMO plan |

|---|---|---|---|

| Coverage type | Universal health insurance | Work-related injury/illness | Comprehensive health plan |

| Emergency ER cover | Yes, via OECB and case rates | Yes, if work-related | Yes, cashless at accredited hospitals |

| Non-accredited hospitals | Partial reimbursement | Limited | Up to 80% reimbursement |

| Outpatient cover | OECB only | No | Yes, broad outpatient benefits |

| Dental, APE, life add-ons | No | No | Optional add-ons available |

| Claims process | Hospital files directly | Employee files with SSS | Cashless or reimbursement |

The PhilHealth OECB is a meaningful upgrade, covering ER consultations and fixed-fee services. But it operates on per-service rates, not a benefit ceiling, so complex emergencies can still leave large unpaid balances.

Here’s how claims typically work under each program:

- PhilHealth inpatient claim: Hospital files the case rate directly with PhilHealth. Employee pays the balance beyond the case rate.

- SSS/ECC claim: Employee or employer files within 5 days of the accident. Medical reimbursement follows after review.

- HMO cashless claim: Employee presents HMO card at an accredited hospital. The HMO settles directly with the provider, no upfront payment needed.

- HMO reimbursement claim: Employee pays at a non-accredited facility, submits receipts and documents to the HMO, and receives reimbursement, typically up to 80%.

HMO benefits for SMEs go well beyond the cashless convenience. The real advantage is speed and certainty. When your employee is in the ER, the last thing anyone needs is a billing dispute. Cashless HMO access eliminates that friction entirely.

Retention data makes this concrete: 67% of employees stay with an SME specifically because of health benefits. That single statistic reframes HMO costs from an expense to a retention investment. For more on optimizing health ROI and combining PhilHealth and HMO coverage, both resources offer practical frameworks.

How comprehensive coverage enhances employee retention and productivity

Once you know what’s covered and what isn’t, the next big question is: Why bother with more than the basics? The business upside is bigger than many assume.

67% of employees stay with SMEs for health benefits, and HMOs reduce absenteeism while boosting overall productivity. Those aren’t soft metrics. They translate directly into lower recruitment costs, fewer sick days, and a more stable workforce.

Here’s what comprehensive emergency coverage actually delivers for your business:

- Reduced absenteeism: Employees with fast access to care recover faster and return to work sooner.

- Higher morale: Staff who feel protected perform better and refer quality candidates to your company.

- Lower turnover costs: Replacing one mid-level employee can cost 50% to 200% of their annual salary. Health benefits are a fraction of that.

- Competitive hiring edge: In industries like tech and hospitality, HMO coverage is now an expected benefit, not a bonus.

- Legal risk reduction: Comprehensive coverage reduces the chance of costly employer liability claims after workplace incidents.

“SME HMO premiums are now scaled for groups of 5 or more, making it easier than ever for small businesses to combat medical inflation without breaking the budget.”

Philippine HMOs lifted healthcare benefits by 20% in the first half of 2025, which means the value of your HMO investment is growing even as premiums remain manageable. Medical inflation in the Philippines consistently outpaces wage growth, so locking in a group HMO rate now protects your budget over time.

Pro Tip: Choose an HMO package that scales with your headcount. Some providers, including those catering specifically to SMEs, allow you to add or remove members as your team grows, so you’re never paying for coverage you don’t need.

For a forward-looking view, the health trends for SMEs in 2026 report outlines how leading businesses are structuring their benefits to stay competitive.

Common pitfalls, edge cases, and how SMEs can improve emergency coverage

Of course, it’s not all smooth sailing. SMEs face unique risks and exceptions. Here’s how to navigate coverage blind spots and strengthen your emergency medical program.

Workplace emergencies not covered due to negligence can expose employers to serious liability. Proper documentation and voluntary HMO coverage are your strongest protections. Many SMEs discover this only after a claim is disputed.

Common compliance pitfalls:

- Missing or late PhilHealth and SSS remittances, which trigger surcharges and legal exposure

- No written hospital tie-up agreement on file for DOLE OSH compliance

- Inadequate first-aid training records or expired certifications

- Failure to update employee enrollment when new staff join

Common edge cases and exclusions to know:

- HIV, STDs, and elective procedures are excluded from most HMO plans

- Non-trauma ER visits during the initial HMO eligibility period may not be covered

- Pandemics and epidemic-related conditions may have specific sub-limits

- Non-accredited hospital visits require reimbursement claims, which take time

Here’s a practical audit checklist to strengthen your coverage:

- Pull your last 12 months of PhilHealth and SSS remittance records. Confirm no gaps.

- Review your DOLE OSH documentation: first-aid training certificates, clinic tie-up agreements, and OSH officer designation.

- List all current employees and confirm they are enrolled in both government programs and your HMO if applicable.

- Identify which hospitals near your office are accredited by your HMO provider.

- Review your HMO policy for exclusions and document a reimbursement process for non-accredited emergencies.

- Set calendar reminders for annual policy renewals and contribution rate updates.

For HR managers navigating this for the first time, the HMO guide for HR managers covers enrollment, documentation, and claims in plain language. Additional employer safety duties under Philippine law are worth reviewing before your next DOLE inspection.

Why the bare minimum isn’t really enough: Our perspective

Here’s what most guides and consultants won’t tell you about true SME preparedness: statutory compliance is a floor, not a ceiling.

Most SMEs treat PhilHealth and SSS remittances as a box-ticking exercise. That works fine until a real emergency exposes the gaps. An employee hospitalized for three days in a non-accredited facility can face bills that PhilHealth covers only partially, leaving both the employee and the employer in an uncomfortable position.

Layering PhilHealth with a right-sized HMO is not just about better benefits. It’s about controlling legal, business continuity, and reputational risks simultaneously. One unresolved workplace medical claim can damage trust across your entire team.

The best-performing SMEs we work with treat employee health as a strategic asset, not a cost center. Medical inflation consistently outpaces wage growth in the Philippines, which means the cost of not having comprehensive coverage grows every year. Maximizing your health investment through a layered approach is what separates resilient SMEs from reactive ones.

“Future-ready SMEs invest in layered health programs, not just for compliance, but for growth.”

Compliance protects you from penalties. Comprehensive coverage is what makes your business genuinely attractive in a competitive hiring market.

Take the next step: Strengthen your SME emergency medical program

Ready to put this into action? Here’s how you can quickly upgrade protection for your business and employees.

If this article has made one thing clear, it’s that relying solely on PhilHealth and SSS leaves real gaps in your team’s protection and your business’s risk profile. The good news is that upgrading your coverage doesn’t have to be complicated or expensive.

At HMO Plans, we specialize in building right-sized emergency medical programs for SMEs across the Philippines, starting with groups as small as five employees. From cashless access to the Big 9 Hospitals to 100% coverage for pre-existing conditions up to the Maximum Benefit Limit, our plans are built to close the gaps that government programs leave open. Compare SME HMO plans and find the right fit for your team, or explore HMO features to see exactly what’s included before you commit.

Frequently asked questions

Are SMEs in the Philippines required to provide emergency medical coverage?

Yes, SMEs must remit PhilHealth and SSS/ECC contributions and comply with DOLE OSH emergency aid rules, but supplemental HMO coverage remains optional though strongly advisable.

What is the PhilHealth Outpatient Emergency Care Benefit (OECB)?

The OECB covers ER consultation and fixed-fee services for PhilHealth members in emergencies, applying per-service rates rather than an overall benefit cap.

How do HMO plans benefit SME employees beyond PhilHealth or SSS?

HMO plans offer cashless hospital access and 80% reimbursement for non-accredited facilities, supplementing PhilHealth inpatient coverage and SSS work injury benefits with faster, broader protection.

What are common exclusions in emergency coverage for SME employees?

Typical exclusions include HIV, STDs, and elective surgery, along with non-trauma ER visits during initial eligibility periods and claims from non-accredited facilities that require reimbursement instead of cashless settlement.

What penalties do SMEs face for non-compliance with DOLE OSH medical requirements?

DOLE OSH non-compliance can result in penalties ranging from ₱40,000 to ₱100,000 per day until violations are corrected, making proactive compliance far less costly than the alternative.