Why flexible health plans benefit Philippine SMEs and employees

TL;DR:

- Losing skilled employees to competitors with better health coverage often goes unnoticed until it impacts business.

- Flexible health plans allow SMEs in the Philippines to scale coverage based on workforce needs, budget, and roles, instead of rigid, one-size-fits-all options.

Losing a skilled employee to a competitor offering better health coverage is a problem most SME owners don’t see coming until it’s too late. Many small and medium enterprises in the Philippines still rely on standard, one-size-fits-all HMO plans that look good on paper but fail to meet the real, varied needs of a diverse workforce. The result? Employees feel undervalued, HR teams face constant complaints, and business owners end up spending more on replacement hiring than they would have on upgraded coverage. This article breaks down how flexible health plans actually work, what to compare, why they matter beyond basic care, and the legal risks you must avoid when managing them.

Table of Contents

- What makes health plans ‘flexible’ for SMEs?

- Comparing flexible health plans: What to look for

- Benefits beyond coverage: Why flexibility matters

- Legal and implementation risks SMEs must avoid

- Our expert perspective: What most SMEs miss about ‘flexible’ plans

- Ready to design a flexible health plan for your team?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Flexibility means choice | Flexible health plans let SMEs tailor coverage and add options as workforce needs evolve. |

| Smart comparisons matter | Analyze network reach, limits, add-ons, and claims process before choosing any plan. |

| Boost retention | Workers stay longer when their health plan fits their life stage and needs. |

| Legal compliance is critical | Downgrading existing health benefits without proper planning can put SMEs at legal risk. |

| Expert advice pays off | Benchmark with business goals and seek guidance to avoid common pitfalls in plan implementation. |

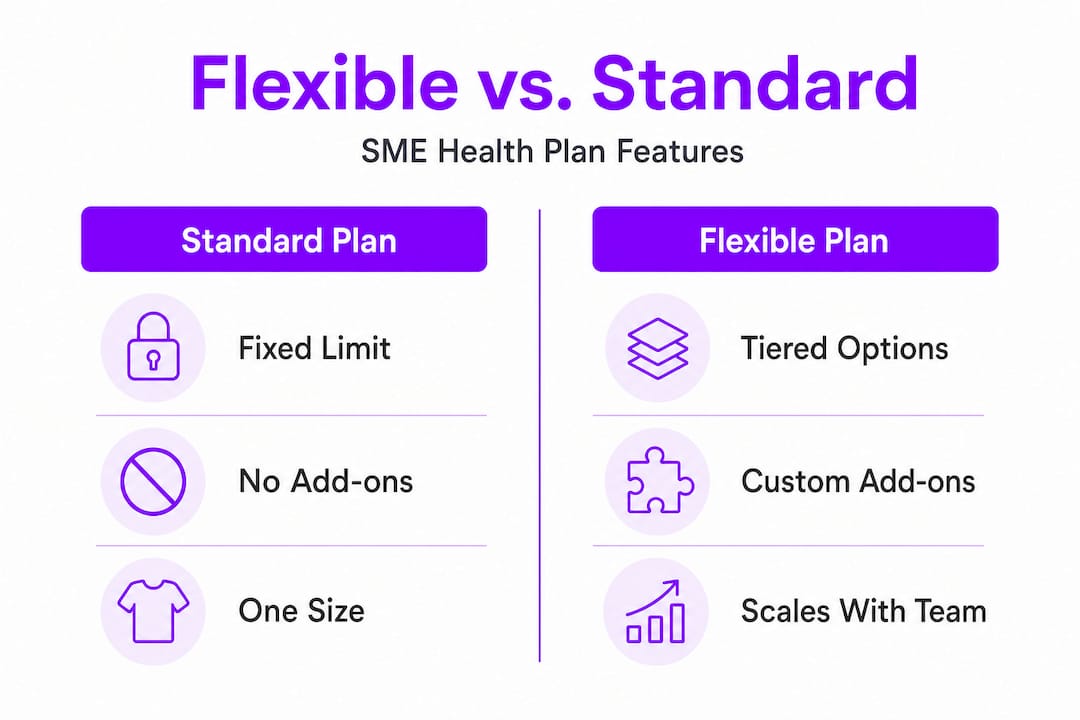

What makes health plans ‘flexible’ for SMEs?

With the key challenge established, let’s unpack what “flexible” actually means in the local workplace insurance context.

A flexible health plan is not just a plan with a lot of features. It’s a structured health program that lets employers scale coverage to fit their workforce size, budget, and the varying needs of different employee groups. For Philippine SMEs, this means choosing a plan architecture that grows with your business and adapts to your people, rather than locking every employee into the same rigid benefits package regardless of their role or life stage.

In practice, flexible HMO plans for SMEs typically appear in a few different structures. The most common is a tiered program, where each tier (often labeled Bronze, Silver, Gold, and Platinum) offers progressively higher Maximum Benefit Limits (MBL), broader hospital network access, and more generous room and board allowances. Employers can assign tiers based on seniority, department, or salary band, giving senior staff more comprehensive coverage while keeping costs manageable for entry-level positions.

Customizable HMO programs are used by Philippine employers specifically to scale benefits with business size and employee needs, which means the plan adjusts as your headcount grows or your budget changes. Flexibility also shows up through optional riders and add-ons: dental HMO, annual physical exams, maternity benefits, and life and accident insurance can be layered on top of a base plan rather than bundled into a single expensive package that everyone pays for whether they need it or not.

According to industry research on HMO plan design, flexibility in Philippine employer plans typically shows up as three mechanics: employee choice among benefit tiers, scaling of MBL and network access, and optional riders. Understanding all three is what separates a well-designed plan from one that just looks flexible on a brochure.

Here’s what elements are usually adjustable in a flexible SME health plan:

- Maximum Benefit Limit (MBL): The annual cap per employee, typically ranging from PHP 50,000 up to PHP 500,000 or higher depending on the tier

- Room and board allowance: Private, semi-private, or ward accommodation options tied to tier level

- Hospital network size: Access to a smaller local network or expanded access to premier facilities like the Big 9 Hospitals

- Optional add-ons: Dental care, annual physical exams, life and accident insurance

- PhilHealth coordination: Whether the plan supplements PhilHealth or functions independently

- Out-of-network reimbursements: Some plans allow employees to seek care outside the accredited network and file for reimbursement

| Feature | Basic plan | Flexible tiered plan |

|---|---|---|

| MBL range | Fixed (e.g., PHP 100,000) | PHP 50,000 to PHP 500,000+ |

| Add-ons | None or bundled | Optional and customizable |

| Network access | Limited local facilities | Scalable, including Big 9 Hospitals |

| Role-based tiers | No | Yes |

| PhilHealth integration | Standard | Flexible or independent |

Pro Tip: Think of flexibility not as “more features” but as a tool to match the right level of coverage with the right employee group. A junior staff member and a department head don’t have the same healthcare needs, and your plan design should reflect that.

Comparing flexible health plans: What to look for

Now that you know the elements of plan flexibility, it’s essential to understand which features actually matter most in a head-to-head evaluation.

When HR managers sit down to compare flexible health plans, the volume of options can quickly become overwhelming. The key is to build a structured evaluation framework rather than reacting to whichever plan has the most impressive brochure. Every flexible HMO plans overview will highlight its strengths, but your job is to identify which plan aligns best with your actual workforce data and budget constraints.

Cost and flexibility tradeoffs are a core reason this comparison matters: employers must weigh premium cost against coverage limits, network size, and the ability to tailor benefits for different employee demographics and roles. A plan with a low premium per head might seem like a win until you realize the network excludes the nearest hospital to your main office, or the MBL is so low that a single hospitalization wipes out the entire annual benefit.

Here’s a comparison of what tiered plan structures typically look like in the Philippine market:

| Plan tier | Typical MBL | Room & board | Network type | Add-ons available |

|---|---|---|---|---|

| Bronze | PHP 50,000 to PHP 100,000 | Ward or semi-private | Basic local network | Limited |

| Silver | PHP 150,000 to PHP 200,000 | Semi-private | Mid-tier network | Dental optional |

| Gold | PHP 250,000 to PHP 300,000 | Private room | Expanded network | Dental, APE optional |

| Platinum | PHP 400,000 and above | Private room | Premier (Big 9 access) | Full suite available |

When comparing plans, the variables HR teams must scrutinize include network reach (how many hospitals and clinics are covered and where), room and board limits (since ward vs. private room affects employee satisfaction significantly), the MBL relative to average healthcare costs in your industry, and the specific add-ons available at each tier. You also need to look at how customizing HMO benefits works in practice: can you adjust coverage mid-year if your headcount changes, or are you locked in?

Follow these steps when benchmarking plans:

- Set your per-employee budget first. Know what you can spend before entering any conversation with a provider. Premiums vary widely based on tier, add-ons, and employee demographics.

- Map your workforce profile. Consider average age, family situation, existing health conditions, and common roles. A mostly young workforce may prioritize outpatient coverage; a senior team may need higher MBLs.

- Compare on four dimensions: accredited network reach, room and board allowances, annual benefit limits, and available add-ons. Don’t let any single factor dominate your decision.

- Ask about claims and approval processes. How easy is it to file a claim? Are there pre-authorization requirements that could delay emergency care? This is where many plans quietly underperform.

- Review exclusions and limitations carefully. Some plans exclude pre-existing conditions or congenital conditions entirely, which can be a serious gap for employees with chronic health issues.

Pro Tip: A low premium is only a good deal if the coverage is actually usable. Before signing any contract, ask your provider for a sample claims scenario and walk through exactly how the approval process works from a member’s perspective.

Benefits beyond coverage: Why flexibility matters

Looking beyond the technical comparison, it’s crucial to see why flexibility delivers more strategic value than static, fixed-benefit approaches.

The business case for flexible health plans goes well beyond simply checking a compliance box. When employees feel that their health benefits actually reflect their individual needs, engagement and loyalty follow. This is especially true for SMEs competing against larger corporations for talent. A tech startup with 30 employees may not be able to match the salary of a multinational, but a genuinely well-designed health plan sends a clear message: we care about you as an individual, not just as a headcount.

Flexible SME-focused corporate health solutions are directly positioned to address rising healthcare costs and workforce stability concerns, which means they’re built for the pressures your business actually faces right now. With healthcare costs in the Philippines rising year over year, a rigid plan that doesn’t scale or adapt becomes more expensive over time, either because it fails to meet employee needs (leading to turnover) or because you’re paying for coverage that doesn’t align with your workforce’s actual usage patterns.

Key business impacts of offering a flexible health plan include:

- Improved retention rates: Employees who feel their health needs are met are less likely to leave for competitors

- Scalable cost management: Tiered plans let you control spending while still offering meaningful coverage at every level

- Better recruitment positioning: Flexible benefits are a competitive differentiator when attracting talent in tight labor markets

- Reduced absenteeism: Employees with access to proper outpatient care address health issues earlier, reducing long-term sick leaves

- Support for optimizing healthcare spending: Plans that match coverage to actual usage patterns reduce waste and improve ROI on your benefits budget

“Flexible health benefits are no longer a bonus for Philippine SMEs. They are a retention tool, a recruiting asset, and a cost management strategy all at once. Businesses that treat health coverage as a fixed cost rather than a strategic investment will consistently lose their best people to those who don’t.”

The ability to scale benefits as your business grows is another often-overlooked advantage. When you hire your 10th employee, your needs are different from when you hire your 50th. A flexible plan framework means you’re not renegotiating from scratch every time your headcount crosses a threshold.

Legal and implementation risks SMEs must avoid

With benefits outlined, it’s equally vital to address the responsibilities and legal risks that come with making changes to health plan design.

This is the part most SME owners skip, and it’s where the most serious problems arise. Once you establish an HMO plan for your employees in the Philippines, changing or downgrading it carries real legal exposure. Established HMO benefits may be legally protected as supplemental or fringe benefits, meaning that reducing or materially downgrading coverage after it has been implemented can create significant legal risk for employers under Philippine labor law.

This protection applies even when a business faces financial pressure. Simply switching to a lower-tier plan without proper employee consultation and documentation can be treated as a unilateral reduction of benefits, which employees may legally contest.

The most common mistakes SMEs make when managing HMO plan changes:

- Cutting network access without notice: Switching to a plan with a narrower hospital network mid-year without informing employees creates immediate dissatisfaction and potential legal complaints.

- Reducing the MBL during renewal: Lowering the annual benefit limit when renewing a contract, even by a small amount, can be considered a benefits reduction that employees may challenge.

- Removing established add-ons: If dental coverage or annual physical exams were part of the original plan, removing them without agreement from affected employees carries compliance risk.

- Failing to document plan changes: Any modification to health benefits must be communicated in writing, with employees acknowledging the change.

- Ignoring PhilHealth coordination rules: Mismanaging the relationship between your HMO plan and PhilHealth contributions can create compliance gaps with government-mandated health coverage requirements.

“The danger isn’t just coverage gaps. It’s ‘unusable’ coverage: plans where approval delays, inaccessible providers, or poorly communicated processes mean that employees technically have coverage but can’t effectively access it when they need it most. That’s a legal and reputational risk no SME can afford to ignore.”

Lean on SME healthcare best practices to build a governance process around your plan. This means scheduling annual reviews, consulting employees before making changes, and keeping written records of every modification.

Pro Tip: Before changing any element of your health plan, consult with a labor law professional and document everything in writing. Communicate changes at least 30 days in advance and get written acknowledgment from your team.

Our expert perspective: What most SMEs miss about ‘flexible’ plans

After reviewing what works and what can go wrong, here’s some hard-earned perspective for getting the most value from flexibility.

The conventional wisdom is that any flexible plan is automatically better than a rigid one. It’s not. Flexibility is only valuable when it’s matched to what your workforce actually needs and what your business can realistically support. We see SME owners get excited about a plan with 10 add-on options and then realize six months in that they’re paying for features nobody uses, while the two features employees actually need most are buried under approval friction or a narrow hospital network.

The most common benchmarking mistake is focusing entirely on the menu of benefits and ignoring the operational experience of using the plan. Claims processing speed, pre-authorization complexity, member support quality, and the clarity of plan communication matter just as much as the benefit ceiling. A plan that looks generous on paper but requires three business days of pre-authorization for an outpatient procedure is not actually flexible. It’s a bureaucratic obstacle with good marketing.

When customizing plans wisely, the most valuable thing you can do is survey your employees before you finalize any plan structure. Ask them what healthcare services they actually used in the past 12 months. Ask what they wish their current plan covered. That data is more valuable than any provider’s default tier structure.

True flexibility is about alignment, not abundance. The best plan for your SME is the one that covers the right things for the right people at a price that keeps your business financially healthy.

Ready to design a flexible health plan for your team?

Choosing the right flexible health plan is one of the most impactful HR and financial decisions your SME will make this year. Done well, it protects your employees, strengthens your retention, and positions your business as a place where people genuinely want to work.

HMO Plans makes this process straightforward for Philippine SMEs. Whether you’re setting up a plan for the first time or reviewing an existing one that no longer fits your team, the right guidance can help you avoid the common pitfalls covered in this article. From comparing tiered benefit structures to understanding 100% coverage commitments for pre-existing conditions, find SME health plans that fit your workforce size, budget, and goals without the confusing fine print. Take the next step and explore your options today.

Frequently asked questions

What does a flexible health plan typically include for Philippine SMEs?

A flexible health plan usually includes tiered benefit levels, optional add-ons like dental and annual physical exams, and adjustable MBLs to match varying employee needs and business size.

How can flexible health plans help retain employees?

Flexible SME health solutions allow employers to tailor coverage to individual workforce needs, directly addressing concerns about healthcare costs and workforce stability that drive employees to seek better benefits elsewhere.

What legal risks do employers face when changing HMO benefits?

Reducing established HMO benefits may be treated as an illegal unilateral reduction of fringe benefits under Philippine labor law, exposing employers to employee complaints and compliance issues.

How do I evaluate which flexible health plan is right for my business?

Start with your budget and workforce profile, then compare plans on four key dimensions: accredited network reach, room and board limits, annual benefit levels, and optional add-ons, while also factoring in claims and approval process quality.