Explaining Health Insurance Eligibility for SME Owners

TL;DR:

- Offering health coverage without understanding eligibility and compliance can lead to costly IRS penalties.

- Employers with 50+ FTEs must provide minimum essential coverage to avoid penalties, while smaller businesses may qualify for tax credits; employee classification and affordability standards are critical in managing compliance.

Most business owners assume that offering a health plan automatically means their employees are covered and compliant. That assumption can cost you thousands in IRS penalties. Explaining health insurance eligibility properly means understanding a layered system of employer mandates, employee classifications, affordability thresholds, and how those rules intersect with Marketplace subsidies and Medicaid. Whether you have 15 employees or 150, these rules shape your legal obligations and your team’s access to care. This guide cuts through the complexity so you can manage compliance and build a benefits program your employees actually value.

Key Takeaways

| Point | Details |

|---|---|

| Employer mandate threshold | Businesses with 50 or more full-time equivalent employees must offer minimum essential coverage or face IRS penalties. |

| Affordability standard in 2026 | Employee-only premium must not exceed 9.96% of household income for the plan to qualify as affordable. |

| Employee classification matters | Full-time, part-time, and dependent status each carry distinct eligibility rules that affect enrollment and cost-sharing. |

| Verification prevents denials | Running electronic eligibility checks before services reduces costly claim denials and billing errors. |

| Marketplace and Medicaid overlap | Employees offered unaffordable employer coverage may still qualify for subsidized Marketplace plans or Medicaid. |

Explaining health insurance eligibility: what it really means

Health insurance eligibility is the formal term for determining who qualifies for coverage and under what conditions. From the employer side, eligibility means meeting specific thresholds that trigger legal obligations. From the employee side, it means satisfying criteria set by both the employer’s plan and federal rules.

The dividing line for most SMEs sits at 50 full-time equivalent employees. Employers with 50 or more FTEs must offer minimum essential coverage (MEC) to at least 95% of their full-time workforce and their dependents. About 75% of all workers were eligible for employer-sponsored insurance in 2025, which reflects how dominant this channel remains.

If your business has fewer than 50 FTEs, the federal mandate does not apply to you. However, small businesses under 25 FTEs may qualify for tax credits covering up to 50% of premiums through SHOP marketplace plans. That is a meaningful financial incentive even when coverage is optional.

Understanding health insurance criteria on the employee side breaks down into three categories:

- Full-time employees work 30 or more hours per week and are the primary group employers must cover under the mandate.

- Part-time employees (fewer than 30 hours per week) are not required to be offered coverage, though many employers extend benefits voluntarily.

- Dependents include children up to age 26 and must be offered coverage, though spouses are not federally required to be included.

One point that trips up many HR managers: eligibility for coverage is an offer, not a guarantee of enrollment. An employee can decline coverage even when eligible. But if the offer itself doesn’t meet federal standards, the employer faces exposure regardless of whether the employee accepted.

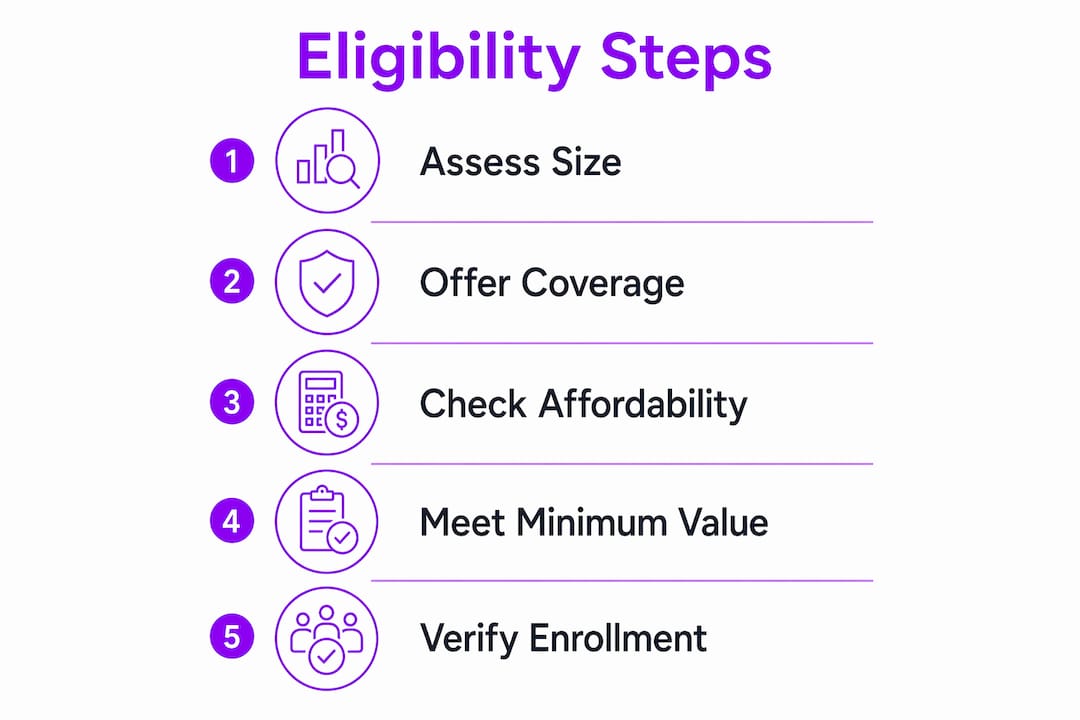

Affordability and minimum value: two tests you cannot ignore

Offering health insurance is not enough on its own. The coverage must pass two federal tests to protect you from penalties and to determine whether your employees can access Marketplace subsidies.

The affordability test checks whether the employee’s share of the premium for employee-only coverage exceeds a set percentage of their household income. For 2026, that threshold is 9.96% of household income. If the employee’s contribution is higher, the plan is deemed unaffordable and the employer may face a penalty if that employee seeks a subsidized Marketplace plan.

The minimum value test requires that the plan pay at least 60% of total allowed costs for a standard population. Think of it as a floor for how much financial protection the plan actually delivers. A plan that technically exists but covers almost nothing fails this test.

Here is what non-compliance looks like in real numbers:

- Employers with 50 or more FTEs who fail to offer coverage at all face a penalty starting at $3,340 per full-time employee beyond the first 30.

- Employers who offer coverage that is unaffordable or fails minimum value face a lower per-employee penalty, but only triggered when an employee actually receives a Marketplace subsidy.

- Both penalty types are assessed by the IRS and can accumulate significantly over a plan year.

Pro Tip: Since affordability is calculated against household income (not W-2 wages), and employers typically only know the employee’s W-2 income, the IRS provides three safe harbor methods: the W-2 safe harbor, the rate of pay safe harbor, and the federal poverty line safe harbor. The federal poverty line safe harbor is the simplest because it sets a fixed dollar amount each year regardless of the employee’s actual income.

Verifying coverage eligibility: the operational side

Understanding the eligibility rules is one challenge. Confirming active coverage status for every employee in real time is another. This is where electronic data interchange (EDI) transactions become critical, particularly for HR teams managing benefits at scale.

The 270/271 transaction set is the healthcare industry’s standard for eligibility verification. Here is how the workflow runs:

- Submit a 270 inquiry to the insurance carrier or clearinghouse with the member’s identifying information.

- Receive a 271 response containing benefit details including coverage type, copays, deductibles, and the all-important coverage status indicator.

- Check the EB01 segment first. An EB01=‘1’ indicates active coverage; EB01=‘6’ signals inactive coverage, which is one of the most common sources of claim denials.

- Extract cost-sharing data only after confirming active status. Pulling deductible or copay information from an inactive record leads to billing errors that are expensive to correct.

Poor eligibility verification practices carry real costs. Reworking a single denied claim costs approximately $25, and most denials are preventable. The operational best practice is to run batch eligibility checks one to three days before scheduled services for high-volume workflows, and real-time checks at the point of scheduling and check-in for lower-volume settings.

| Verification method | Best use case | Timing |

|---|---|---|

| Real-time 270/271 | Individual scheduling and check-in | At point of service |

| Batch 270/271 | High-volume multi-patient workflows | 1 to 3 days before service |

| Manual payer portal | Low-volume or exception handling | As needed |

Pro Tip: Do not treat a 271 response as a simple yes or no answer. The EB segments contain structured data on multiple benefit types. Parse them in order, confirm active status first, and then map the cost-sharing fields. Skipping that sequence is what causes billing teams to quote patients incorrect out-of-pocket amounts.

How Marketplace subsidies and Medicaid change the picture

Here is where eligibility for health coverage gets genuinely complicated for SME owners and HR managers. Your employees do not exist in a vacuum. They interact with a broader ecosystem that includes the ACA Marketplace and Medicaid, and your plan’s quality directly affects their access to subsidized options.

Marketplace premium tax credits are available to employees whose household income falls between 100% and 400% of the federal poverty level. However, an employee who is offered affordable, minimum-value employer coverage is generally not eligible for those subsidies. That creates a direct link between the quality of coverage you offer and the financial options your employees have.

The “family glitch” was a significant policy gap for years. Under the original ACA rules, affordability was measured only against the cost of employee-only coverage. If an employee’s self-only premium was affordable but the family premium was not, dependents still could not access Marketplace subsidies. A 2023 regulatory fix addressed this by allowing dependents to qualify for subsidies when the family tier of employer coverage is unaffordable.

Medicaid adds another layer of variation:

- Expansion states have raised the income threshold for Medicaid eligibility to 138% of the federal poverty level, covering many low-income workers who would otherwise depend on employer plans.

- Non-expansion states maintain lower income cutoffs, leaving some employees in a gap where employer coverage is unaffordable and Medicaid is unavailable.

- Household size matters significantly. A single employee earning $30,000 has a different subsidy eligibility profile than an employee earning the same amount with two dependents.

A practical example: an employee earning $35,000 annually with two children in an expansion state may qualify for CHIP or Medicaid for those children even if the employee themselves takes the employer plan. HR managers who understand this can guide employees toward the right resources during open enrollment rather than leaving them to figure it out alone.

Practical steps to manage eligibility in your SME

Getting eligibility right is less about mastering every regulatory detail and more about building reliable processes. Here is where to focus:

- Classify employees accurately from day one. Track hours worked weekly for anyone near the 30-hour threshold. Misclassification is a recurring source of compliance problems for growing SMEs.

- Enforce the 90-day waiting period rule. Coverage must begin by the 91st day of employment. Pushing it to 120 days because it feels administratively simpler is an ACA violation.

- Document affordability calculations each plan year. Use one of the IRS safe harbor methods consistently, and retain the documentation in case of an audit.

- Communicate eligibility windows clearly during onboarding. New hire enrollment, special enrollment periods triggered by qualifying life events, and open enrollment each have specific timelines that employees must understand to use their benefits.

- Run eligibility audits at least annually. Life changes like marriage, divorce, or a dependent aging off the plan affect coverage status. A mid-year audit catches these before they become claim problems.

Pro Tip: Use the KFF Health Insurance Marketplace Calculator as a free tool to estimate whether your plan meets affordability standards for employees at different income levels. It takes less than five minutes and can flag a potential compliance gap before the IRS does.

Employee healthcare best practices suggest that SMEs with clear enrollment communication see higher plan participation rates, which improves the overall risk pool and can stabilize premiums over time.

My take on where SMEs consistently get this wrong

I have seen two recurring mistakes that cost SME owners more than they realize. The first is treating affordability as a one-time calculation. Business owners set the employee contribution rate in year one, then never revisit it as their workforce demographics change or as the IRS adjusts the affordability threshold. The 2026 threshold is 9.96%. That number shifts every year. A plan that was compliant in 2024 may not be compliant today.

The second mistake is underestimating how much employee classification decisions ripple outward. I have watched companies try to manage benefit costs by keeping workers below 30 hours per week, only to find that the administrative burden of tracking hours and the turnover costs from dissatisfied part-time staff exceeded whatever they saved on premiums. The math rarely works out the way employers hope.

What I have found actually works is treating eligibility as an HR infrastructure problem, not a compliance checkbox. When you build the right classification, verification, and communication workflows from the start, the regulatory requirements mostly take care of themselves. The companies I have seen struggle are the ones that try to manage eligibility reactively, responding to audits and denied claims rather than preventing them.

The intersection with Marketplace and Medicaid rules is where I think most guides shortchange SME readers. Your employees will make enrollment decisions based on the full picture of options available to them. When you understand that picture, you can have more honest conversations with your team about what the benefits package actually delivers. That kind of transparency builds more loyalty than any perks program.

— Eumir

HMO coverage for SMEs that actually meets the standard

If you are looking for a plan that satisfies minimum essential coverage requirements without the administrative headache of deciphering complicated policy language, Hmoplans’ Purple Cow HMO plans are built specifically for SMEs like yours.

Hmoplans offers cashless access to accredited hospitals including the Big 9 Hospitals and Healthway Clinics, comprehensive inpatient and outpatient care, and 100% coverage for pre-existing conditions up to the Maximum Benefit Limit. Optional add-ons include dental, annual physical exams, and life and accident insurance, so you can customize coverage to fit your workforce. Flexible PhilHealth-independent options mean you are not locked into a single compliance structure.

Explore the full plan features or visit Hmoplans to find the right coverage tier for your team size and budget.

FAQ

What does health insurance eligibility mean for employers?

Health insurance eligibility defines which employees must legally be offered coverage and whether that coverage meets federal standards for minimum essential coverage and affordability. Employers with 50 or more full-time equivalents must offer qualifying coverage to at least 95% of their full-time employees or face IRS penalties.

How do you qualify for health insurance as an employee?

Employees generally qualify for employer-sponsored coverage by working 30 or more hours per week. Eligibility also extends to dependents under age 26, and some employers voluntarily extend coverage to part-time workers below the 30-hour threshold.

What is the 2026 affordability threshold for employer health plans?

For 2026, a plan is considered affordable if the employee’s premium for self-only coverage does not exceed 9.96% of household income. If a plan exceeds this threshold, affected employees may qualify for Marketplace subsidies and the employer may face penalties.

Can employees still get Marketplace subsidies if their employer offers insurance?

Yes, but only if the employer’s plan is unaffordable or fails the minimum value test. Employees offered a qualifying, affordable plan are generally not eligible for premium tax credits through the Marketplace, regardless of their household income.

What is the maximum waiting period before coverage must begin?

Employers must offer coverage no later than the 91st day of employment. Coverage must start by day 91, including weekends and holidays. Extending the waiting period beyond 90 days is an ACA violation.