How to Claim Accident Coverage: A Step-by-Step Guide

TL;DR:

- Filing an accident claim involves promptly reporting the incident and submitting complete, finalized documentation. Active cooperation with the insurer and timely responses to requests are crucial to ensure a faster settlement process. Preparing in advance and understanding policy details significantly reduce the risk of claim delays or denials.

An accident coverage claim is a formal request to your insurance company for reimbursement or payment following an injury or vehicle accident. Knowing how to claim accident coverage correctly separates a fast payout from a months-long dispute. The process involves three core actions: reporting the accident promptly, gathering the right documents such as police reports and medical records, and working with an assigned insurance adjuster through each stage of review. Get any one of those wrong, and your claim stalls.

How to claim accident coverage: documents you need first

The most common reason claims get delayed is missing paperwork. Gather everything before you make your first call to the insurer.

Core documents for any accident claim

Every accident coverage process starts with the same foundational records. You need the police report number, photos of the accident scene and any damage, and contact information for all witnesses. For personal injury claims, attending physician’s statements, diagnostic reports, and finalized hospital invoices are required. Some insurers do not accept interim invoices. That means a bill marked “estimated” or “pending” can get your claim rejected outright.

You also need your policy number, the exact date, time, and location of the accident, a written description of what happened, and the insurance information of any third parties involved. If you are filing auto accident benefits, include the other driver’s license plate, insurer name, and policy number.

| Document | Purpose | Source |

|---|---|---|

| Police report | Confirms incident details and parties involved | Local police department |

| Photos of damage or injury | Visual evidence for adjuster review | You or a witness |

| Physician’s statement | Proves medical necessity and injury extent | Your treating doctor |

| Hospital invoices (finalized) | Documents actual medical expenses | Hospital billing office |

| Witness contact info | Corroborates your account of the accident | Collected at the scene |

| Policy number and ID | Links claim to your coverage | Your insurance card |

Pro Tip: Call your insurer before submitting anything and ask specifically which document versions they accept. Some require finalized police reports rather than preliminary ones, and submitting the wrong version restarts the clock on your claim.

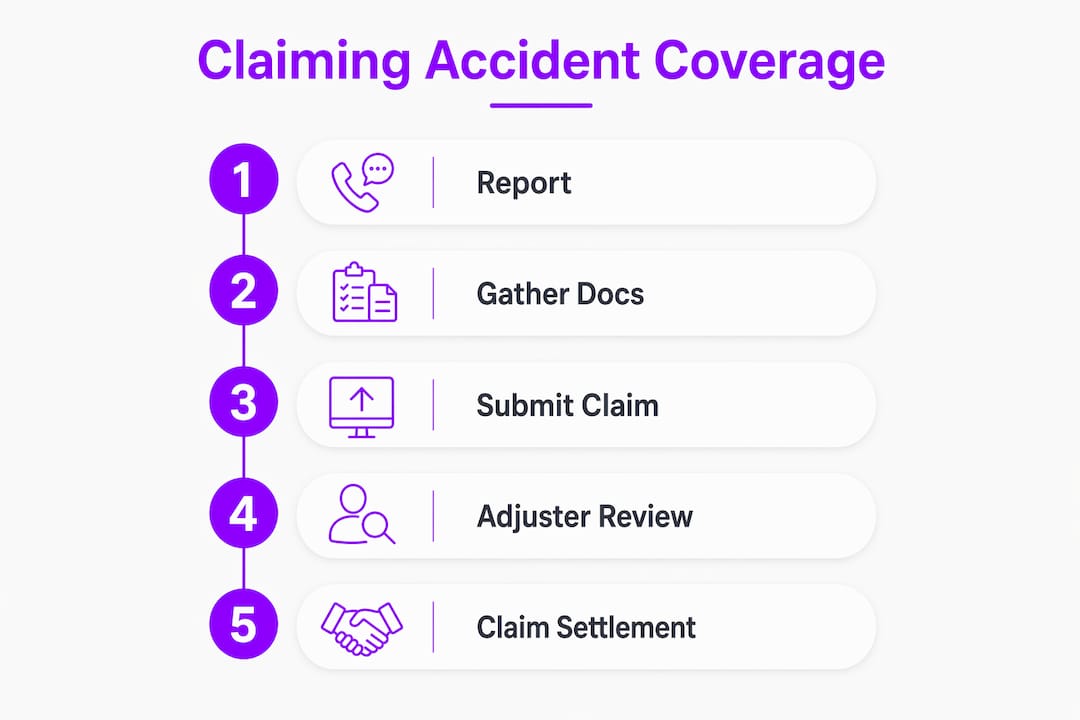

What are the steps to file an accident claim?

Filing accident claims follows a two-phase structure. The first phase covers immediate notification. The second covers formal documentation submission. Confusing the two is one of the most common mistakes claimants make, and it can trigger processing delays or outright denial.

Here is the full sequence:

-

Report the accident to your insurer within 24 hours. Most policies require reporting “as soon as reasonably possible.” Filing within 24 hours is the standard expectation. You can report by phone, through the insurer’s mobile app, or via their online portal.

-

Provide initial incident details. During your first contact, share the date, time, and location of the accident, a description of what happened, the police report number, and the names and insurance details of any other parties involved.

-

Receive your claim number. The insurer assigns a claim number immediately after notification. Write it down. Every follow-up call, email, and document submission should reference this number.

-

An adjuster is assigned to your case. Adjusters typically contact claimants within 1–3 business days. They will review your initial report and identify what additional documentation they need.

-

Submit your full claim form and supporting documents. This is the formal filing step. Attach all finalized documents: police report, medical records, bills, photos, and witness statements. Submit everything the adjuster requests promptly.

-

Cooperate with the investigation. The adjuster may schedule a vehicle inspection, request additional medical records, or ask follow-up questions. Respond quickly. Delays on your end extend the timeline.

-

Receive the coverage decision and settlement offer. Once the investigation closes, the insurer issues a decision. If approved, they present a settlement amount. Review it against your policy limits before accepting.

Pro Tip: Keep a dedicated folder, physical or digital, for every document, email, and phone call related to your claim. Log the date, time, and name of every insurer representative you speak with. This record protects you if a dispute arises later.

Common mistakes that derail accident claims

Most claim denials trace back to a handful of avoidable errors. Knowing them in advance puts you ahead of the process.

- Treating notification as filing. Calling your insurer to report an accident is not the same as submitting a formal claim. Notification and formal filing are separate steps with separate deadlines.

- Submitting incomplete medical records. Interim hospital invoices or preliminary physician notes often fail insurer review. Always confirm you are submitting finalized documents.

- Missing the reporting window. Waiting days or weeks to report an accident gives insurers grounds to question your account. Most policies require prompt reporting, and late notification weakens your position.

- Failing to photograph the scene. Photos taken at the accident site are among the strongest evidence an adjuster can review. Skipping this step forces the claim to rely solely on written accounts.

- Not reviewing your policy before filing. Reviewing your policy for coverage limits, exclusions, and submission deadlines before filing prevents surprises that lead to denials.

- Ignoring adjuster requests. Every unanswered request from your adjuster adds days or weeks to your timeline. Treat each request as urgent.

“Early reporting, detailed records, and full cooperation with insurer requests are the three factors that most directly influence whether a claim gets approved and paid on time.”

The accident coverage process rewards preparation. Claimants who document everything from the scene forward and respond to adjuster inquiries without delay consistently see faster resolutions. Those who wait, guess, or submit incomplete paperwork face the longest timelines.

How do you track and manage your claim after filing?

Filing your claim is not the finish line. Active follow-up is what moves a claim from “under review” to “settled.”

Understanding what your adjuster does

The adjuster’s job is to verify your account, assess the damage or injury, and determine what your policy covers. Insurers process claims in two stages: initial intake with basic incident details, then a deeper documentation review. During the second stage, the adjuster may request additional medical records, a second vehicle inspection, or clarification on specific expenses. Respond to every request within 48 hours when possible.

Tools for staying on top of your claim

Most major insurers now offer online portals and mobile apps where you can check claim status, upload documents, and message your adjuster directly. Use them. Waiting for a callback adds unnecessary delays. Keep the following on hand at all times:

- Your claim number

- Your adjuster’s direct phone number and email

- A log of every communication with dates and summaries

- Copies of every document you submitted

Early vs. delayed reporting: what the outcomes look like

| Factor | Early Reporting (within 24 hours) | Delayed Reporting (3+ days) |

|---|---|---|

| Adjuster assignment | Within 1–3 business days | May be delayed pending review |

| Document verification | Faster, scene evidence is fresh | Harder to verify, photos may be unavailable |

| Claim approval timeline | Typically shorter | Often extended due to gaps in evidence |

| Risk of denial | Lower | Higher, especially with policy deadline conflicts |

| Negotiation position | Stronger with complete records | Weaker without contemporaneous documentation |

If the insurer’s settlement offer is lower than expected, you have the right to appeal. Gather additional supporting documents, such as independent repair estimates or a second medical opinion, and submit a formal written dispute. Timely reimbursements depend on both sides moving efficiently, and knowing your appeal rights keeps you from accepting less than your policy allows.

Key takeaways

Claiming accident coverage successfully requires prompt reporting, complete documentation, and active cooperation with your insurer’s adjuster from day one.

| Point | Details |

|---|---|

| Report within 24 hours | Most policies require prompt notification; late reporting weakens your claim position. |

| Separate notification from filing | Calling your insurer is not the same as formally submitting your claim with documents. |

| Use finalized documents only | Interim invoices and preliminary reports are often rejected; confirm accepted versions first. |

| Engage your adjuster quickly | Responding to adjuster requests within 48 hours keeps your claim moving forward. |

| Review your policy before filing | Check coverage limits, exclusions, and deadlines before submitting anything to avoid denials. |

What i’ve learned from watching claims go wrong

I have reviewed enough accident claims to spot the pattern immediately. The people who struggle are almost never the ones with complicated cases. They are the ones who assumed the process would be simple and did not prepare.

The single biggest mistake I see is treating the insurer’s first phone call as the end of the task. You report the accident, you get a claim number, and you think you are done. You are not. That call is the start of a documentation process that requires your active participation for days or weeks afterward. The claimants who understand this from the beginning move through the process with far less stress.

What actually works is building a paper trail from the moment the accident happens. Take photos before you move your vehicle. Get the other party’s information even if the accident seems minor. Call your insurer the same day. These are not complicated steps, but most people skip at least one of them because they are shaken up or in a hurry.

The other thing I would tell anyone filing a claim: read your policy before you need it. The accident insurance options available to you are only useful if you know what they cover. Discovering an exclusion after the accident is one of the most frustrating experiences in insurance. Discovering it before costs you nothing.

— Eumir

Protect your team with the right coverage from the start

Knowing the steps to claim coverage matters most when your plan actually covers what you need. Hmoplans, powered by Purple Cow, offers HMO plans built for Philippine SMEs that include life and accident insurance add-ons, out-of-network reimbursements, and dedicated member services to support you through the claims process.

When an accident happens, the last thing you want is to discover gaps in your coverage. Hmoplans gives your team access to the Big 9 Hospitals, Healthway Clinics, and 24/7 nationwide support, with 100% coverage up to the Maximum Benefit Limit for no-fault scenarios. Explore the full range of HMO plan features and see how Hmoplans makes accident coverage straightforward for your business. Visit Hmoplans to get started.

FAQ

What is the first step to claim accident coverage?

Report the accident to your insurer within 24 hours by phone, app, or online portal. Provide the date, time, location, police report number, and details of any other parties involved.

What documents do i need to file an accident insurance claim?

You need a finalized police report, photos of the accident, a physician’s statement, finalized hospital invoices, witness contact information, and your policy number. Some insurers also require diagnostic reports and third-party insurance details.

How long does an accident coverage claim take to process?

Adjusters typically contact claimants within 1–3 business days of notification. Full processing time depends on how quickly you submit complete documentation and respond to adjuster requests.

What is the difference between notifying and formally filing a claim?

Notification alerts your insurer that an accident occurred. Formal filing is a separate step that requires submitting completed claim forms and all supporting documents. Missing the formal filing deadline can result in denial even if you notified your insurer promptly.

Can a claim be denied if i report the accident late?

Yes. Most policies require reporting “as soon as reasonably possible,” and late reporting gives insurers grounds to question your account or deny the claim entirely. Filing within 24 hours gives you the strongest position.