Accident insurance options for Philippine SMEs explained

TL;DR:

- Many SMEs rely on HMO plans that often leave coverage gaps for accidents, leading to costly claim denials. Proper understanding, timely reporting, and tailored policies are essential for effective accident insurance protection in the Philippines. Regular policy reviews and employee training significantly improve claim success and workforce safety.

Most HR managers assume their existing HMO plan already handles accident scenarios well enough. That assumption is expensive. Coverage gaps and claim denials in accident-related insurance decisions frequently come from exclusions and the legal interpretation of what counts as an “accident” in the first place. The fine print can be the difference between a settled claim and a grieving family left without support. This guide breaks down accident insurance options available to Philippine SMEs, explains what is genuinely covered, and gives HR decision-makers a practical framework for choosing coverage that actually works when it matters most.

Table of Contents

- Why accident insurance matters for Philippine SMEs

- What accident insurance actually covers (and excludes)

- Comparing accident insurance options for SMEs

- Common pitfalls and how to avoid claim denials

- How to select and implement the right accident insurance

- The uncomfortable truth about accident insurance for SMEs

- Better protect your team with enhanced SME coverage

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Accident coverage is essential | Standard health or HMO plans often lack the full accident protection most SMEs require. |

| Understand exclusions | Exclusions like intoxication and high-risk activities are the top cause of claim denials. |

| Choose the right policy | Compare standalone and bundled options to match your team’s risk profile and needs. |

| Avoid common pitfalls | Clear claim processes and ongoing staff education prevent denied claims and frustration. |

| Review and communicate | Annual reviews and clear HR-led communication maximize value from your accident insurance investment. |

Why accident insurance matters for Philippine SMEs

Accident insurance is not just a nice-to-have. It is financial protection that activates when illness-based HMO coverage stops. A typical HMO plan covers hospitalization from sickness, but a construction supervisor who fractures a vertebra falling from scaffolding on a client site, or an account manager injured in a road accident during a company event, faces a very different claims process depending on whether accident coverage is in place.

The numbers tell a clear story. The accident insurance market in the Philippines grew by 40% in accident business as of 2025, yet insurance penetration remains below 1.9% of the population. That gap is widest among SMEs, where benefit packages are often built around the minimum requirements rather than actual workforce risk.

Common scenarios where accident coverage becomes critical include:

- Offsite workplace injuries during field visits, client calls, or travel between locations

- Commuting accidents where an employee is injured traveling to or from work

- Company events such as team building activities, client entertaining, or logistics work

- Accidental death or permanent disability affecting a primary breadwinner’s family

Many claims fail not because the incident is uncovered, but because HR teams and employees do not understand policy boundaries. Missing one form or filing two days late can result in a full denial.

“Understanding accident coverage basics before an incident occurs is what separates a company that supports its people from one that discovers the gaps too late.”

Pro Tip: Benchmark your current benefit package against competitors in your industry segment. With the accident insurance market growing this fast, employees are becoming more aware of what strong packages look like. Falling behind on coverage is a talent retention risk, not just a compliance issue. You can also review real examples of HMO coverage to understand where gaps commonly appear.

What accident insurance actually covers (and excludes)

Here is where most guides gloss over the most important part. Accident insurance sounds straightforward: if someone gets hurt, the policy pays out. But the legal definitions embedded in Philippine insurance contracts create a more complicated picture.

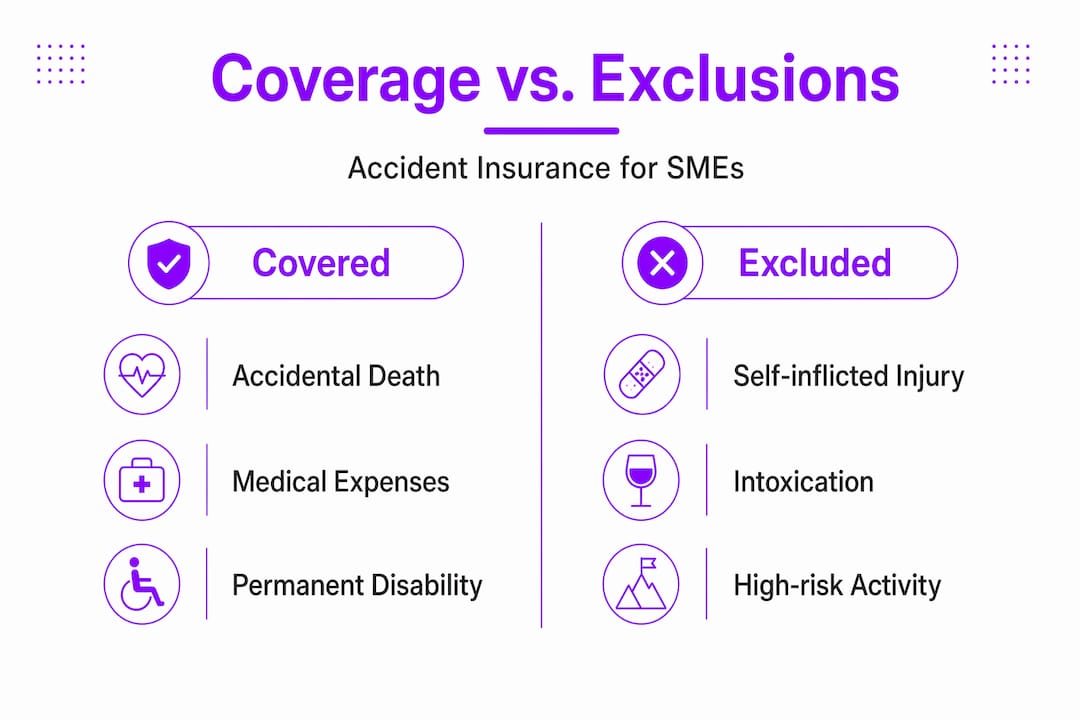

Standard accident policies in the Philippines typically cover the following inclusions and carry the following exclusions:

| Covered (Typical Inclusions) | Not Covered (Key Exclusions) |

|---|---|

| Accidental death | Self-inflicted injuries |

| Permanent total disability | Injuries while intoxicated |

| Permanent partial disability | High-risk pursuits (e.g., extreme sports) |

| Temporary total disability | War, terrorism, civil unrest |

| Medical reimbursement for accident injuries | Pre-existing musculoskeletal conditions |

| Accident-related emergency care | Late-reported incidents |

| Accidental dismemberment | Illegal activities at time of injury |

Legal exclusions such as self-inflicted injuries, intoxication, high-risk activities, and contractual requirements are the leading sources of claim denials in accident insurance cases across the Philippines.

Here is a real-world SME scenario. A logistics company filed a claim on behalf of a driver who was severely injured in a nighttime collision. The insurer denied it because the driver’s blood alcohol level was above the legal limit at the time of the accident. The company had never briefed employees on the intoxication clause. The family received nothing. That outcome was entirely preventable.

Common situations where coverage is lost include:

- Missing paperwork: No police report, medical certificate, or incident report submitted

- Late notification: Filing the claim after the policy’s notification window (often 30 to 60 days)

- Excluded circumstances: Injury occurred during an activity the policy specifically prohibits

- Incorrect classification: Insurer classifies the injury as illness-related rather than accidental

- No direct link: Medical records do not clearly connect the injury to the accident event

Use the insurance selection checklist as a starting point when reviewing your current or prospective accident policy in detail.

Pro Tip: If any of your employees do fieldwork, travel frequently, or handle physical operations, request written clarification from your insurer about exactly how those job functions are classified under the policy. Do not assume standard coverage extends to high-risk tasks without verification.

Comparing accident insurance options for SMEs

Market momentum in the accident insurance sector means Philippine SMEs now have more choices than before, but policy scope and exclusions vary widely across product types. Understanding the structural differences helps you make a smarter buying decision.

| Policy Type | Coverage Scope | Key Restrictions | Best For |

|---|---|---|---|

| Standalone accident policy | Broad accident coverage, lump sum or reimbursement | No illness coverage, separate claim process | High-risk industries |

| HMO accident rider | Accident add-on to existing HMO plan | Rider limits tied to MBL, must be active HMO member | SMEs with existing HMO |

| Group life with accident benefit | Life insurance with accidental death rider | Focuses on death/disability, not medical costs | Companies prioritizing income protection |

| Bundled group accident plan | Combined coverage for accident-related medical and disability | May have sub-limits per incident | Large SME workforces |

Each option fits a different risk profile and budget. Here is a step-by-step approach for evaluating suitability:

- Assess your workforce risk profile: Review job functions, travel requirements, and past incident history to determine where accidents are most likely.

- Review the scope of current coverage: Identify what your HMO or group life policy already covers so you avoid paying for overlapping benefits.

- Request a sample policy document: Never buy based on a brochure alone. Read the actual exclusions and definitions section carefully.

- Compare the claims process: Ask each provider how claims are filed, what documentation is required, and what their average processing time is.

- Seek advice from a local insurance specialist: Philippine regulations and insurer practices differ from international norms, and a local expert can flag issues a generic comparison tool will miss.

Accident riders bundled with HMO plans are often the most cost-effective entry point for SMEs. They piggyback on your existing claims infrastructure and administrative relationships, reducing friction when a claim needs to be filed quickly. Explore top health insurance providers to see what bundled solutions look like in practice, and consider how optimizing your SME healthcare budget can factor accident coverage into a broader cost strategy.

Common pitfalls and how to avoid claim denials

Knowing the policy is only half the battle. The other half is making sure your HR team and employees actually know how to use it. Most claim denials do not happen because of dishonest insurers. They happen because the people filing the claim did not follow the right steps at the right time.

The most common pitfalls include:

- Not knowing the notification deadline: Many employees assume they can file whenever they are ready. Most cannot.

- Incomplete medical documentation: Accident claims require a clear paper trail linking the event to the injury.

- No internal incident report: Without a company-side record, the insurer has no corroboration for the claim.

- Claiming for excluded activities: Employees injured during non-work personal activities expect coverage that the policy does not extend.

- Failure to disclose pre-existing conditions: If an insurer discovers undisclosed health history, they may void the entire claim.

Filing window reminder: Notification and settlement deadlines are typically 30 to 60 days after the accident, with proofs of loss. Missing this window is the single most avoidable reason SME claims get denied.

A practical SME claims checklist should include:

- Immediate internal incident report filed by employee or supervisor

- Police report obtained if the accident involved a vehicle or public space

- Medical certificate from the attending physician specifying the accidental cause

- Hospital admission records and billing statements if hospitalized

- Written notification to the insurer within the required timeframe

- Follow-up tracking with HR until claim is officially acknowledged

Pro Tip: Run a 30-minute claims orientation for all employees at onboarding and repeat it annually. Teach them exactly what to do in the first 24 hours after an accident. That single session could be the reason a claim gets paid instead of denied. You can also optimize your claims workflow with a structured internal process that keeps HR on top of deadlines.

How to select and implement the right accident insurance

Choosing the right policy is a decision. Implementing it well is a discipline. Many SMEs get the first part right and struggle with the second. Here is a structured plan that covers both.

SME benefit packages benefit from benchmarking and clear communication to close the insurance protection gap effectively.

- Evaluate key risks first: Map your workforce by job type and identify the highest-risk roles. Prioritize coverage design around those people.

- Shortlist credible providers: Focus on insurers with established accident claims track records in the Philippines, not just the lowest premium.

- Compare policy details side by side: Use the comparison table from the previous section as your framework. Focus on exclusions, not just inclusions.

- Negotiate group rates: SMEs often qualify for group pricing that individual employees cannot access. Even five to ten employees can unlock better rates.

- Implement and educate staff: Roll out the policy with a clear communication plan. Give employees a one-page summary of what they are covered for, what they are not, and what to do if they need to file a claim.

Reviewing your policy every 12 months is not optional. Workforce composition changes, new roles emerge, and insurer terms evolve. What fit your SME two years ago may leave gaps today.

Pro Tip: Schedule your annual policy review to coincide with your employee headcount review. If you added 10 people or launched a new operational division, your risk profile changed. Your coverage should change with it.

Building genuine employee buy-in requires transparency. Share the coverage details openly. When employees understand the protection they have, they value it. That makes accident insurance a real retention tool, not just a line item. Start by reviewing your comprehensive SME health cover options to understand how bundled solutions can bring it all together.

The uncomfortable truth about accident insurance for SMEs

Here is something most comparison guides will not tell you: buying accident insurance is the easy part. The hard part is making it work.

We see this pattern repeatedly. An SME invests in a solid policy. The premiums are paid on time. Then an accident happens, and the claim gets denied because no one told the supervisor to file an incident report within 24 hours. Or the employee assumed the company handled the paperwork. Or HR did not know the policy’s definition of “accident” excluded that specific type of activity.

The uncomfortable truth is that insurance is only as good as your HR team’s understanding of the rules. A policy sitting in a filing cabinet protects nobody.

Most guides stop at the comparison table. But the companies that actually protect their people go further. They train supervisors. They create clear internal protocols. They review the policy every year and update employee communication when terms change. They treat accident coverage as an ongoing HR process, not a one-time purchase decision.

There is a contrarian point worth making here: a smaller, well-understood policy with clear claims support will outperform a premium, feature-heavy policy that nobody in your company knows how to use. Complexity without clarity is liability.

The best move you can make after reading this article is not to immediately buy a new product. It is to audit what you already have, test whether your HR team can explain it accurately, and identify the gaps before an incident forces you to discover them. Explore employee health benefit alternatives if you find that your current setup is missing key components.

Implementation discipline is what saves lives and money. That is not a slogan. It is a pattern we see play out in real claims every year.

Better protect your team with enhanced SME coverage

For SMEs that want accident coverage built into a broader health protection strategy, HMO Plans powered by Purple Cow offers a practical, clearly structured solution. Their HMO plans include life and accident insurance as optional add-ons, so you can bundle coverage without managing multiple providers or navigating conflicting claims processes.

Purple Cow’s approach eliminates the fine-print confusion that trips up most SME benefit programs, with 100% coverage commitments up to the Maximum Benefit Limit for pre-existing conditions and no-fault scenarios. Explore Purple Cow’s SME HMO features to see exactly what is included, or check out SME member services for a clearer picture of the support your employees would receive. Upgrading your coverage does not have to be complicated.

Frequently asked questions

What is typically excluded from accident insurance for SMEs in the Philippines?

Excluded incidents often include self-inflicted injuries, intoxication at the time of the accident, high-risk activities such as extreme sports, and injuries resulting from war or terrorism. Always request the full exclusions list before purchasing any policy.

How soon must an accident claim be filed for SME policies?

Most insurers require claims to be filed within 30 to 60 days after the accident, along with complete proof of loss including medical records and incident documentation. Filing late is one of the most common and preventable reasons for denial.

Can accident insurance be added to an existing HMO for employees?

Yes, many providers offer accident insurance as an add-on rider to existing HMO plans, giving SMEs a convenient way to enhance employee protection without managing a completely separate policy and claims process.

What are the main benefits of offering accident insurance in SME benefit packages?

Accident insurance protects employees and their families from the unexpected financial burden of injuries, and it signals that the company takes employee welfare seriously, which strengthens retention and overall workplace trust.

How can we avoid the most common claim denials in practice?

Train employees and supervisors to report incidents immediately, gather required documentation on the day of the accident, and submit claims within the policy’s notification window. Most denials trace back to misunderstood exclusions or late and incomplete claim submissions, both of which are preventable with proper HR education.