Why Select Nationwide HMO Plans for Your Business

TL;DR:

- Many Filipino employers mistakenly assume all HMO plans offer equal nationwide coverage, which is often not the case. Genuine nationwide plans provide accredited provider networks across all regions, ensuring consistent, cashless care for employees regardless of location. Selecting a plan with true geographic reach enhances employee health outcomes, retention, and financial predictability while reducing legal and operational risks.

If you’ve ever watched a valued employee struggle to find an accredited doctor in their province while their Manila-based colleagues get same-day consultations, you already understand why selecting nationwide HMO plans is one of the most consequential decisions an HR team can make. The assumption that all HMO plans deliver equal coverage regardless of geography is one of the most common and costly mistakes Filipino employers make. This article breaks down what nationwide HMO coverage actually means, why it matters for dispersed workforces, and how to choose a plan that won’t let your team down when care is needed most.

Table of Contents

- Key takeaways

- Why select nationwide HMO plans: the core argument

- Why nationwide coverage delivers real business benefits

- Challenges in managing nationwide HMO plans

- How to evaluate and select the right plan

- My take on what most employers get wrong

- Finding the right nationwide plan for your SME

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Not all HMOs cover everywhere | Regional HMO plans often leave provincial employees without accredited providers near them. |

| Nationwide coverage reduces financial risk | Predictable costs and lower out-of-pocket expenses benefit both employer and employee budgets. |

| Network proximity beats network size | A plan with 5,000 providers means nothing if none are near your employees’ actual locations. |

| Switching providers carries legal risk | Changing HMO coverage without maintaining continuity can breach employee rights and invite disputes. |

| SME-specific plans exist and work well | Providers like Hmoplans offer full nationwide coverage designed specifically for smaller Philippine businesses. |

Why select nationwide HMO plans: the core argument

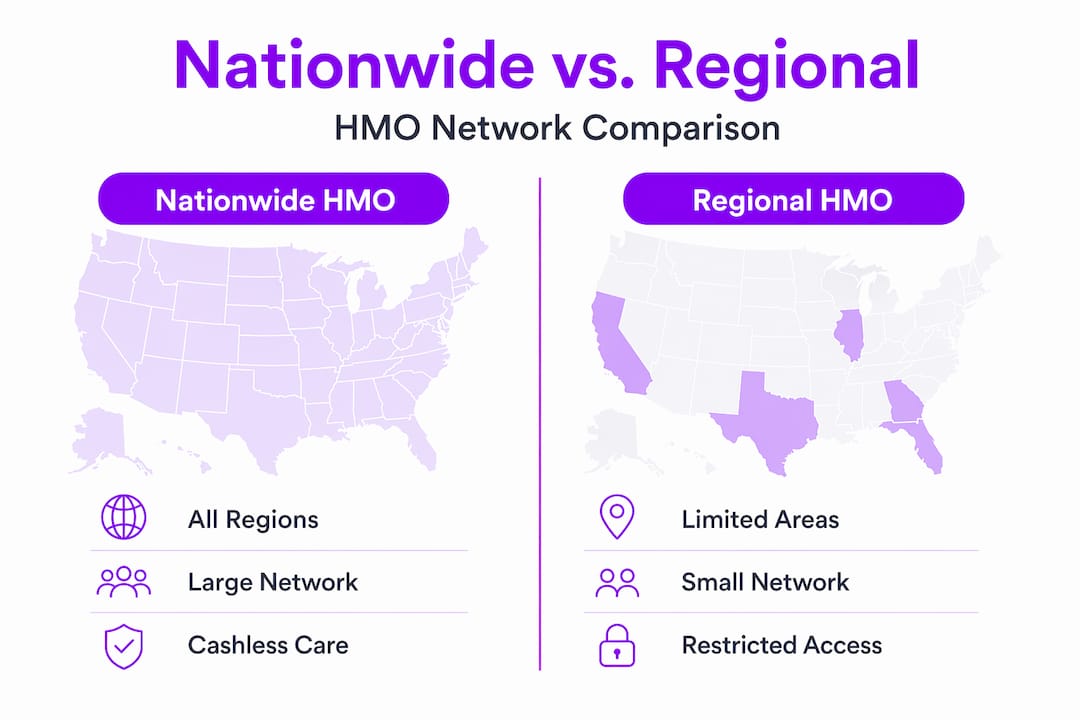

The term “nationwide HMO” gets used loosely in the Philippine market. Not every plan that claims nationwide reach actually delivers it. Understanding the structural difference matters before you sign anything.

A nationwide HMO plan maintains an accredited provider network across all major regions of the country, including Metro Manila, the Visayas, Mindanao, and provincial areas. Employees can access cashless care, primary care physicians (PCPs), and referral pathways regardless of where they live or are assigned. A regional plan, by contrast, concentrates its network in one metro area and offers limited or reimbursement-only access elsewhere.

HMO members choose a primary care physician who coordinates all specialist referrals and non-emergency care. That works well when the PCP is actually accessible. For an employee based in Davao or Cagayan de Oro, “accessible” requires a genuinely nationwide network, not a list of clinics padded with Metro Manila addresses.

Types of nationwide HMO coverage

Understanding the types of nationwide HMO coverage helps you match the right plan structure to your workforce profile.

| Coverage Type | Network Scope | Best For |

|---|---|---|

| Full Nationwide HMO | Broad accredited network across all regions | Companies with employees in multiple regions |

| Select HMO | Smaller networks with lower premiums | Budget-conscious firms with Metro-concentrated staff |

| Integrated/Supplemental Plan | Layers on top of PhilHealth | Companies wanting layered protection |

| PPO-style open access | Broader provider choice, higher cost | Executives or specialized medical needs |

When you compare HMO vs PPO plans, the core difference is cost predictability versus provider flexibility. HMO Silver-tier plans average $115 less per month compared to PPOs, but they require PCP referrals for specialists. For most Philippine SMEs managing tight benefit budgets, the HMO model wins on cost. The real question is which HMO structure gives your employees real access rather than nominal coverage.

Why nationwide coverage delivers real business benefits

Choosing HMO insurance with a genuine nationwide footprint is not about checking a compliance box. It directly affects how your employees experience work, how often they take unplanned sick days, and whether they stay with your company.

HMO packages improve healthcare accessibility nationwide, and Philippine employers with strong coverage see measurable gains in financial manageability and workforce productivity. That connection is direct. An employee who can see a doctor near their home without paying out of pocket is more likely to catch health problems early, recover faster, and return to work sooner.

Here is what nationwide coverage actually delivers for your business:

- Consistent care access across assignments. When you deploy staff to regional offices or project sites, a nationwide plan means they keep their benefits without gap periods or reimbursement paperwork.

- Lower absenteeism. Employees with reliable access to preventive care use emergency services less often and miss fewer days.

- Stronger retention. Employers with strong HMO packages see higher workforce engagement. Healthcare benefits consistently rank among the top reasons Filipino workers stay with an employer.

- Financial predictability. Fixed monthly premiums replace unpredictable out-of-pocket medical events for both the company and employee. That matters for budget planning.

- Regulatory compliance. Providing adequate healthcare benefits is not optional in the Philippines. A nationwide plan that covers employees wherever they work reduces the legal exposure that comes with inadequate coverage.

Pro Tip: Before finalizing any plan, map where your employees actually live and work, not just where your office is. A plan with strong Makati coverage and thin Cebu City access is a regional plan wearing a nationwide label.

Nationwide HMO plans are a strategic HR lever that builds a more resilient workforce. That is not an abstraction. It is the difference between an employee who addresses a health concern in week one and one who ignores it until week twelve when it becomes a serious, expensive problem for everyone.

Challenges in managing nationwide HMO plans

Knowing the benefits is only half the equation. HR professionals who have managed HMO transitions will tell you the operational challenges are where plans fall apart. Here is where the real work happens.

The most common failure points in nationwide HMO management:

-

Assuming network size equals network reach. A plan with 3,000 accredited providers might have 2,800 of them concentrated in NCR. Testing the employee care journey, including PCP access near worksites, referral turnaround, and consistent laboratory partners, tells you more than any provider count.

-

Neglecting referral process clarity. Employees often avoid specialist care not because they lack coverage but because the referral process feels complicated. Make sure your chosen plan has a clear, fast referral pathway and that your HR team can explain it in plain terms.

-

Switching providers without continuity protections. This is the most legally risky mistake. Changing an HMO provider without preserving network adequacy can breach contractual protections and expose the employer to employee relations disputes. If an employee is mid-treatment and you switch providers, their continuity of care is your responsibility.

-

Skipping employee orientation. Enrolling 50 employees in a plan and sending them a card is not implementation. Without orientation, employees default to using the plan incorrectly, generating out-of-pocket costs that fuel resentment.

-

Ignoring escalation paths. Every nationwide HMO plan should come with a clear escalation process for denied claims and service disputes. If the provider cannot tell you how disputes get resolved, treat that as a serious red flag.

Pro Tip: When reviewing plan contracts, look for an explicit continuity-of-care clause. If an employee is undergoing treatment when you switch providers, this clause obligates the new provider to maintain coverage through the completion of that treatment. Many employers discover this clause is missing only after a dispute has started.

Clear communication and continuity-of-care protocols are not just good HR practice. They are the legal defense against claims that your coverage became unusable.

How to evaluate and select the right plan

Here is the practical side of choosing HMO insurance that actually performs across regions. Use this as your evaluation framework when assessing affordable HMO options for your team.

Start with a coverage checklist. The HMO coverage checklist for Philippine SMEs is a good starting point, but your internal version should include your specific employee locations and known health utilization patterns.

Core features to verify before signing:

- Accredited hospitals and clinics in every city or municipality where you have employees

- Access to at least one major hospital within reasonable travel distance of each employee cluster

- Dental and outpatient care coverage included or available as add-ons

- Pre-existing condition coverage with clear terms around limits

- Out-of-network reimbursement for emergencies in uncovered areas

- Digital claims and consultation access for remote employees

Beyond the checklist, verifying provider networks requires more than reading a list. Call the accredited clinic nearest to your Cebu or Davao employees and confirm they are actively accepting new patients under the plan you are evaluating. A provider on a list who stopped accepting new patients six months ago is not part of your network in any practical sense.

On budget, the instinct to choose the lowest premium is understandable. Lower HMO costs reflect a tradeoff with network size and referral requirements, so verifying whether key providers are in-network is what protects the value of the plan. You can explore how SMEs cut costs without cutting coverage to find that balance without defaulting to the cheapest option on the table.

Finally, use employee feedback from your current plan. The most valuable data in HMO selection is what your own employees are already telling you. Long wait times for referrals, clinics that are hard to reach, or confusion about what is covered are all signals that your current plan is underperforming on nationwide health plan benefits.

My take on what most employers get wrong

I’ve worked with enough Philippine SMEs to see a consistent pattern. The businesses that end up in coverage disputes did not choose bad HMO plans on purpose. They chose plans the same way they buy office supplies: searching for the best price without a real quality benchmark.

What I’ve learned is that the hidden cost of an inadequate nationwide HMO plan is not measured in premiums. It shows up in turnover. An employee in Pampanga who cannot find an accredited doctor under their plan does not send a formal complaint. They update their resume. By the time HR notices the pattern, the company has already lost several good people to competitors with better benefits.

The other thing most employers overlook is the employee-relations legal risk. Maintaining network adequacy during provider changes is not just a compliance issue. It is the foundation of employee trust. When a worker is diagnosed with something serious and discovers their mid-treatment coverage just changed, the company is now the antagonist in that story. I’ve seen that scenario damage employer brands in ways that take years to repair.

The counterintuitive insight I always share: a nationwide HMO plan is not a cost. It is risk mitigation. The companies I’ve seen invest in HMO benefits that retain employees spend less on recruitment, onboarding, and operational disruption than the ones that cut premiums by ₱500 per head per month. The math is not close.

— Eumir

Finding the right nationwide plan for your SME

If you’ve been evaluating nationwide health plan benefits and keep running into providers that offer broad promises with complicated exclusions, Hmoplans was built specifically to solve that problem.

Hmoplans, powered by Purple Cow and underwritten by Etiqa, provides Philippine SMEs with 100% coverage up to the Maximum Benefit Limit, including pre-existing conditions, congenital conditions, and special procedures. That is not standard in this market. Their nationwide HMO plans for SMEs cover employees from Metro Manila to Mindanao, with access to the Big 9 Hospitals, Healthway Clinics, and a network built for real geographic reach. Optional add-ons include dental, annual physical exams, and life and accident insurance. Their member services platform handles claims and support so your HR team spends less time managing disputes and more time on actual people strategy.

FAQ

What makes a nationwide HMO different from a regional plan?

A nationwide HMO maintains accredited providers across all major Philippine regions, so employees get cashless access to care regardless of where they are assigned. A regional plan concentrates its network in one metro area, often leaving provincial employees with reimbursement-only access.

Why choose an HMO over a PPO for employee benefits?

HMO plans generally cost significantly less per month than PPO plans while still providing coordinated, cashless care through a network of accredited providers. For most Philippine SMEs, the cost predictability of an HMO outweighs the added provider flexibility of a PPO.

What are the main types of nationwide HMO coverage?

The primary types include full nationwide HMOs with broad regional networks, select HMOs with smaller networks at lower premiums, and integrated plans that supplement PhilHealth. The right type depends on your employee locations and budget.

What legal risks come with switching HMO providers?

Switching providers without continuity-of-care protections can breach employee contracts and trigger labor disputes, especially if workers are mid-treatment when coverage changes. Always negotiate continuity-of-care clauses before transitioning plans.

How can HR verify that a nationwide HMO actually covers employee locations?

Go beyond the provider list. Contact accredited clinics in your employees’ cities directly to confirm they are accepting new plan members, and test the referral pathway before committing. Network proximity to your worksites matters more than total provider count.