Optimize employee healthcare workflow for Philippine SMEs

TL;DR:

- Philippine SMEs must comply with mandatory contributions to SSS, PhilHealth, and Pag-IBIG for all employees.

- Automating healthcare workflows reduces errors, processing time, and administrative costs significantly.

- Supplementing PhilHealth with private HMO plans improves employee benefits, retention, and business competitiveness.

Healthcare administration quietly bleeds time, money, and talent from Philippine SMEs every single year. Missed PhilHealth deadlines trigger penalties. Manual payroll entries create errors that frustrate employees and auditors alike. And when benefits feel like a bureaucratic maze, your best people start exploring competitors who seem to have it figured out. This guide cuts through the noise with a practical, step-by-step roadmap built specifically for HR managers at Philippine small and medium enterprises. You’ll walk away with concrete strategies for compliance, automation, and insurance optimization that actually move the needle.

Table of Contents

- Understand mandatory healthcare requirements in the Philippines

- Assess your company’s current healthcare workflow

- Implementation: Automate and outsource key healthcare processes

- Optimize and expand health insurance: PhilHealth and HMO strategy

- Ensure ongoing compliance and troubleshooting for SME health benefits

- Why most Philippine SMEs underestimate the power of optimized healthcare workflows

- Take the next step: Modern SME HMO plans built for the Philippines

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your obligations | Understand PhilHealth, SSS, and Pag-IBIG contributions and compliance to avoid costly penalties. |

| Leverage automation | Use AI-powered HR tools and outsourcing to save time, reduce errors, and ensure full compliance. |

| Combine PhilHealth and HMO | Layering group HMO on top of PhilHealth provides cost-effective, cashless coverage that retains employees. |

| Review and adapt regularly | Regularly assess workflows, keep policies updated, and swiftly address compliance or coverage gaps. |

| SMEs gain from optimization | Streamlining healthcare benefits pays off through increased retention, productivity, and minimized risk. |

Understand mandatory healthcare requirements in the Philippines

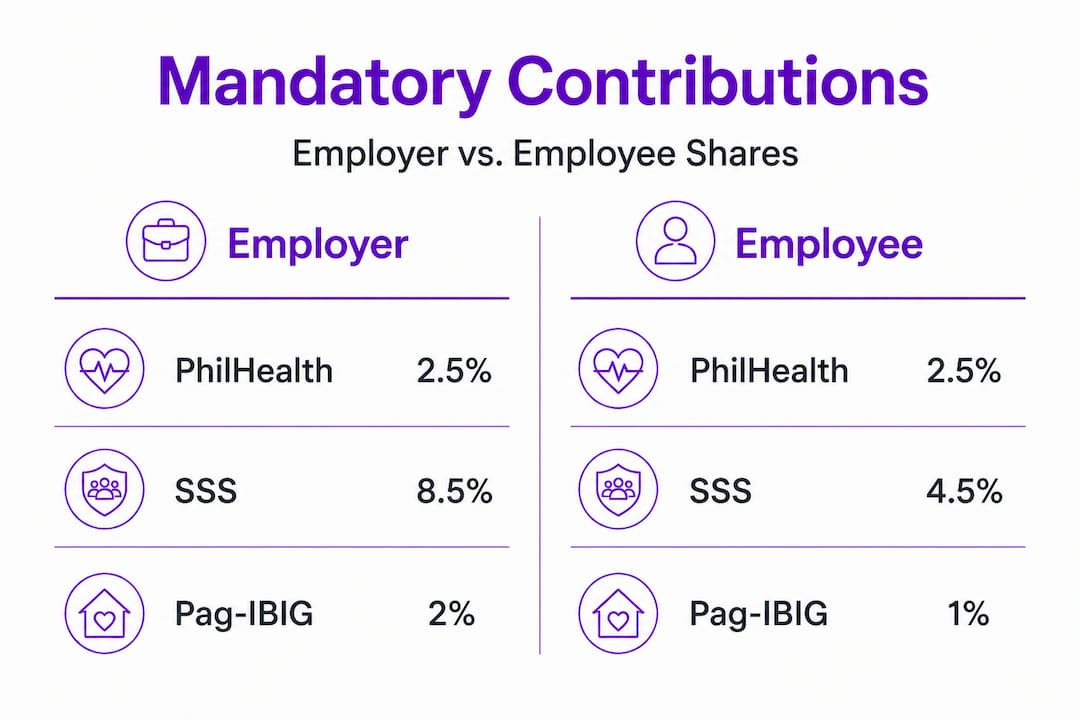

Before you can fix anything, you need to know exactly what the law requires. Philippine employers, regardless of company size, must enroll all employees in three mandatory programs: the Social Security System (SSS), PhilHealth, and the Home Development Mutual Fund (Pag-IBIG). Each has its own contribution schedule, employer-employee sharing rules, and submission deadlines.

PhilHealth contributions are mandatory for all Philippine employers including SMEs, with the rate set at 5% of monthly basic salary, split equally between employer and employee. As of recent updates, the minimum contribution is PHP 500 per month, while the maximum monthly contribution is capped based on the salary ceiling. SSS contributions follow a different bracket system, where employer shares are generally higher than employee shares. Pag-IBIG requires a minimum of PHP 100 per month from both sides, though employees can opt to contribute more.

Here is a quick reference for the three programs:

| Program | Employer share | Employee share | Key deadline |

|---|---|---|---|

| PhilHealth | 2.5% of salary | 2.5% of salary | Monthly, per SBN schedule |

| SSS | Varies by bracket | Varies by bracket | Monthly or quarterly |

| Pag-IBIG | PHP 100 minimum | PHP 100 minimum | Monthly |

Common misunderstandings cost SMEs real money. Many HR teams assume that part-time or project-based workers are exempt, but Philippine law is clear that regular employees must be covered from day one of employment. Another frequent mistake is missing the deadline for new employee enrollment, which can trigger back payments and surcharges.

A solid foundation in SME health benefit workflow helps you build compliance systems that run consistently, not just when someone remembers to check.

Pro Tip: Bookmark the official PhilHealth, SSS, and Pag-IBIG portals and set a quarterly calendar reminder to check for rate or policy updates. Regulatory changes often roll out with little advance notice, and being caught off guard is entirely avoidable.

Assess your company’s current healthcare workflow

With the basics and legalities covered, it’s time to look inward and evaluate your current workflow for potential improvements. Most HR teams are too busy running operations to step back and ask whether the process itself makes sense. That honest assessment is where transformation starts.

Start with a structured checklist. Review these areas carefully:

- Payroll processing: Are contributions calculated automatically, or does someone manually look up brackets each month?

- Enrollment management: Do new hires get enrolled in SSS, PhilHealth, and Pag-IBIG within the required window?

- Leave management: Is sick leave tracked separately from HMO claims, and are those records reconciled?

- Document storage: Are government receipts and proof-of-payment documents saved in an organized, accessible system?

- Benefit communication: Do employees actually know how to use their HMO card or file a PhilHealth claim?

Signs of a broken workflow are usually obvious once you look for them. Missed contributions that pile up, late payslips that frustrate employees, and manual data entry that results in name mismatches with government records are all red flags.

The data on this is striking. HR automation reduces HR processing time by 50 to 60%, cuts errors to below 0.05%, and can lower administrative costs by 74% through outsourcing. That is not a marginal improvement. That is a fundamental shift in how much time your team spends on healthcare admin versus strategic work.

Compare the two approaches side by side:

| Workflow type | Processing time | Error rate | Monthly cost | Compliance risk |

|---|---|---|---|---|

| Manual | High (3-5 days) | 2-5% | High | Significant |

| Automated/HRIS | Low (under 1 day) | Below 0.05% | Reduced by up to 74% | Minimal |

Thinking through optimizing healthcare costs and improving benefits utilization together gives you the full picture: you are not just saving admin hours. You are directly protecting your bottom line.

Implementation: Automate and outsource key healthcare processes

After identifying weak spots, the next move is to overhaul inefficient areas with smarter technology and outsourcing. This is where HR managers often hesitate, worried about disruption or steep learning curves. The good news is that a phased rollout removes both concerns.

Here is a practical implementation sequence:

- Audit your current tools. Identify what software, if any, you already use for payroll and HR. Many SMEs use basic spreadsheets, which works until it really does not.

- Select an HRIS platform. Look for a Human Resource Information System (HRIS) built for Philippine compliance requirements, including automatic SSS, PhilHealth, and Pag-IBIG computation.

- Migrate payroll data. Move employee records, salary data, and contribution histories into the new system. Do this carefully, verifying each record before going live.

- Automate statutory reports. Set the system to generate 13th-month pay reports, BIR forms, and monthly contribution schedules automatically.

- Train your team. Even a 2-hour orientation session for HR and payroll staff dramatically reduces adoption friction.

- Evaluate outsourcing options. For teams with under five HR staff, outsourcing payroll processing and compliance filing may be more cost-effective than managing it in-house.

The numbers are compelling. HRIS adoption benchmarks show payroll processing time dropping from 3 to 5 days down to a single day, saving a 200-employee firm approximately PHP 400,000 per year. Outsourced payslip costs fall from $18.50 to $4.85 per employee. Time-to-hire compresses from 22 days to just 6.

Beyond efficiency, there is the compliance angle. AI-powered HRIS tools ensure 100% compliance with DOLE, BIR, and SSS regulatory changes by automatically updating tax tables and statutory formulas. That eliminates the single biggest source of accidental non-compliance for most Philippine SMEs.

You can also reference SME benefits solutions and how HMOs support SME benefits to understand how to extend this automation advantage into your insurance administration as well.

Pro Tip: Structure your automation rollout in phases. Start with payroll and statutory contributions in month one, add leave management in month two, and integrate HMO billing reconciliation in month three. Trying to do everything at once creates chaos. Phased deployment keeps your team confident and your data clean.

Optimize and expand health insurance: PhilHealth and HMO strategy

Once your processes are running efficiently, focus turns to maximizing the benefits themselves, ensuring holistic coverage for employees and better ROI for your business. PhilHealth is your foundation, but it was never designed to be the whole structure.

Start by using PhilHealth correctly. Many employees and even HR managers do not know that PhilHealth operates on a case-rate system, meaning it pays a fixed amount per diagnosis rather than covering actual hospital costs. Keeping employee and dependent records updated is essential, and using PhilHealth-accredited facilities ensures claims are processed without complications.

Supplementing PhilHealth with a private group HMO plan changes the equation entirely. Private HMO coverage for SMEs enhances overall benefits, reduces employee out-of-pocket expenses, and significantly improves retention. The logic is straightforward: when an employee gets hospitalized, PhilHealth pays a fixed case rate. A group HMO covers the remaining balance cashlessly, eliminating the financial stress that sends employees to competing employers who offer better benefits.

The PhilHealth-first, HMO-balance approach boosts employee productivity, cuts absenteeism, and reduces turnover. Those are measurable business outcomes, not just feel-good HR initiatives.

When evaluating group HMO plans, look for these features:

- Cashless access to a broad hospital network including major tertiary facilities

- Teleconsultation services so employees can consult doctors without taking half a day off

- Wellness programs that encourage preventive care and reduce hospitalizations

- Mental health support, which has become a non-negotiable benefit for talent-competitive companies

- Annual physical exams that catch conditions early before they become expensive claims

- Dental coverage as an optional add-on that employees genuinely value

One mistake SMEs commonly make is not reviewing benefit limits annually. A Maximum Benefit Limit (MBL) that was adequate three years ago may no longer cover current hospital costs. Another overlooked opportunity is the de minimis tax benefit. Group health insurance premiums up to a certain threshold are tax-exempt, meaning both employer and employee save on their tax exposure.

Personalized wellness care is also emerging as a meaningful add-on that forward-thinking SMEs integrate alongside traditional HMO benefits, offering employees more than just sick-care coverage.

Choosing between health benefit options does not have to be a complex decision. When you layer PhilHealth as the base and HMO as the enhancement, you create a coverage system that is both cost-efficient and genuinely attractive to employees.

Pro Tip: Ask your HMO provider to run a utilization report after the first 6 months. This report shows which benefits employees actually use, helping you reallocate spend toward the features that matter most to your team.

Ensure ongoing compliance and troubleshooting for SME health benefits

With the right structures in place, your final step is maintaining your system to avoid costly compliance gaps and ensure lasting success. Building a great workflow is half the work. Keeping it compliant and functional is the other half.

Here is a practical troubleshooting checklist for HR managers:

- Run monthly compliance audits. Verify that all employee contributions were remitted on time and that receipts are documented and stored.

- Cross-check employee records quarterly. Catch name discrepancies, missing SSS or PhilHealth numbers, and unenrolled dependents before they become claims problems.

- Monitor DOLE advisories. The Department of Labor and Employment (DOLE) issues updates on labor standards. Your HRIS should flag these automatically, but a monthly manual review adds a safety net.

- Review HMO accreditation lists annually. Hospital and clinic accreditations change. Employees need current lists so they do not accidentally visit out-of-network facilities.

- Document every policy change. When you update contribution rates, benefit limits, or coverage providers, send written notifications to all employees and keep signed acknowledgments on file.

The risks of getting this wrong are significant. DOLE non-compliance penalties range from PHP 30,000 to PHP 100,000. Beyond fines, there is the risk of labor disputes and reputational damage that makes recruitment harder.

Two specific edge cases deserve attention. First, labor-only contracting: if you outsource payroll or HR functions, ensure the arrangement does not inadvertently shift statutory contribution responsibility away from your company. Labor-only contracting violations carry serious penalties. Second, the non-diminution principle: once you offer an HMO benefit voluntarily, you generally cannot remove or reduce it without employee consent. Plan your benefit rollouts with this in mind.

Staying ahead of health benefits trends in the Philippines helps you anticipate regulatory shifts before they become urgent problems.

Why most Philippine SMEs underestimate the power of optimized healthcare workflows

Here is the uncomfortable truth: most SMEs treat healthcare compliance as a box-checking exercise. File the contributions, keep the receipts, move on. And technically, that keeps you out of trouble. But it also keeps you exactly where your competitors are, fighting for talent with a bare-minimum benefits package in a labor market where employees increasingly know their worth.

The data point that should change how you think about this: mandatory benefits basics are considered sufficient for compliance but inadequate for competitive talent attraction. Experts consistently recommend supplemental HMO or private insurance as the deciding factor in talent wars, particularly in industries like tech, hospitality, and healthcare where skilled workers have real choices.

We have seen this play out across our own client portfolio. Companies that treat healthcare workflow optimization as a business strategy, not just an HR task, experience measurably better outcomes. Lower turnover means lower hiring costs. Faster claims processing means employees trust the system. Clear benefit communication means people actually use their coverage, which reinforces the value of working for your company.

The real leverage point is this: the same effort required to manage a manual, reactive healthcare workflow is roughly equivalent to the effort needed to implement and maintain an automated, proactive one. The difference is that one system creates compliance anxiety every month, while the other runs quietly in the background and makes your business more competitive.

Think about your SME benefits workflow strategy as a high-return investment, not an administrative burden. The companies winning at talent retention are not always paying the highest salaries. They are offering benefits that feel real, accessible, and valuable. That starts with getting the workflow right.

Take the next step: Modern SME HMO plans built for the Philippines

Ready to upgrade your SME’s approach to healthcare benefits? Here’s how you can get started, risk-free.

Everything covered in this guide, from layering PhilHealth with supplemental HMO coverage to ensuring 100% coverage for pre-existing conditions and simplifying your benefits administration, is exactly what HMO Plans was built to support. Partnered with Purple Cow and Etiqa, we provide SME-focused group HMO plans with cashless access to the Big 9 Hospitals, Healthway Clinics, 24/7 nationwide coverage, and digital healthcare platforms that make claims and consultations effortless.

Explore our HMO plan features to see how straightforward benefits administration can be. Check out SME member services to understand the support your team would receive from day one. And when you are ready to find the right plan, HMO Plans for SMEs is your starting point. No complicated terms. No coverage surprises. Just real, reliable healthcare for your people.

Frequently asked questions

What are the minimum legal healthcare contributions required for SMEs in the Philippines?

SMEs must make mandatory contributions to SSS, PhilHealth, and Pag-IBIG for all regular employees. PhilHealth requires 5% of monthly basic salary, split equally between employer and employee.

Why supplement PhilHealth coverage with an HMO plan?

PhilHealth only covers fixed case rates, often leaving large out-of-pocket gaps. Supplemental group HMO plans cover remaining balances cashlessly, reduce employee financial stress, and significantly improve retention.

Is automating employee healthcare workflows worth the investment?

Yes, and the numbers are clear. HRIS automation cuts processing time by 50 to 60%, reduces errors to below 0.05%, and can lower administrative costs by up to 74% through outsourcing.

How can SMEs maximize the ROI from insurance benefits?

Start by fully optimizing PhilHealth usage and updating dependent records, then add de minimis tax-exempt perks before scaling to a full group HMO. This stepwise approach, as Richest PH notes, minimizes cost while reducing turnover.

What’s the risk if SMEs fail to comply with health benefit laws?

DOLE non-compliance can result in penalties from PHP 30,000 to PHP 100,000, plus exposure to labor disputes and lasting reputational damage that makes future hiring harder.