Premium health coverage explained for Philippine SMEs

TL;DR:

- Many Philippine SMEs mistakenly view PhilHealth as comprehensive health coverage, but premium plans from private HMOs offer significantly broader benefits. Offering higher benefit limits, private rooms, specialist access, and coverage for pre-existing conditions helps attract and retain skilled employees. Proper evaluation of plan details, PEC handling, and aligning coverage with business goals are essential for choosing truly premium health solutions.

Many Philippine SMEs still treat PhilHealth as a complete health benefits solution, but the reality is that top-performing companies in tech, hospitality, and healthcare are quietly pulling talent away by offering something more. Premium health coverage is no longer a perk reserved for large corporations. It has become a competitive necessity for SMEs that want to attract skilled workers and actually protect them when it matters most. This guide breaks down exactly what premium health coverage means, how it works alongside PhilHealth, and what HR managers and SME owners need to know before choosing a plan.

Table of Contents

- Understanding the basics: PhilHealth and private health plans

- What makes health coverage ‘premium’? Key features and tiers

- Handling pre-existing conditions: What SMEs need to know

- How premium plans complement PhilHealth in real-world SME settings

- Why redefining “premium” matters for SMEs and what most get wrong

- Explore premium HMO options for your SME

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Premium means more than price | Premium health coverage includes broader benefits, higher limits, and specialized care beyond the basics. |

| PhilHealth is always required | Employers must provide PhilHealth contributions even when offering private or premium coverage. |

| Pre-existing conditions need scrutiny | Coverage for pre-existing conditions varies; always check waiting periods and benefit caps before choosing a plan. |

| Supplemental plans boost competitiveness | Premium coverage helps attract and retain employees by filling gaps left by public insurance alone. |

Understanding the basics: PhilHealth and private health plans

Before you can evaluate premium coverage, you need a clear picture of what already exists in the Philippine health landscape and where it falls short.

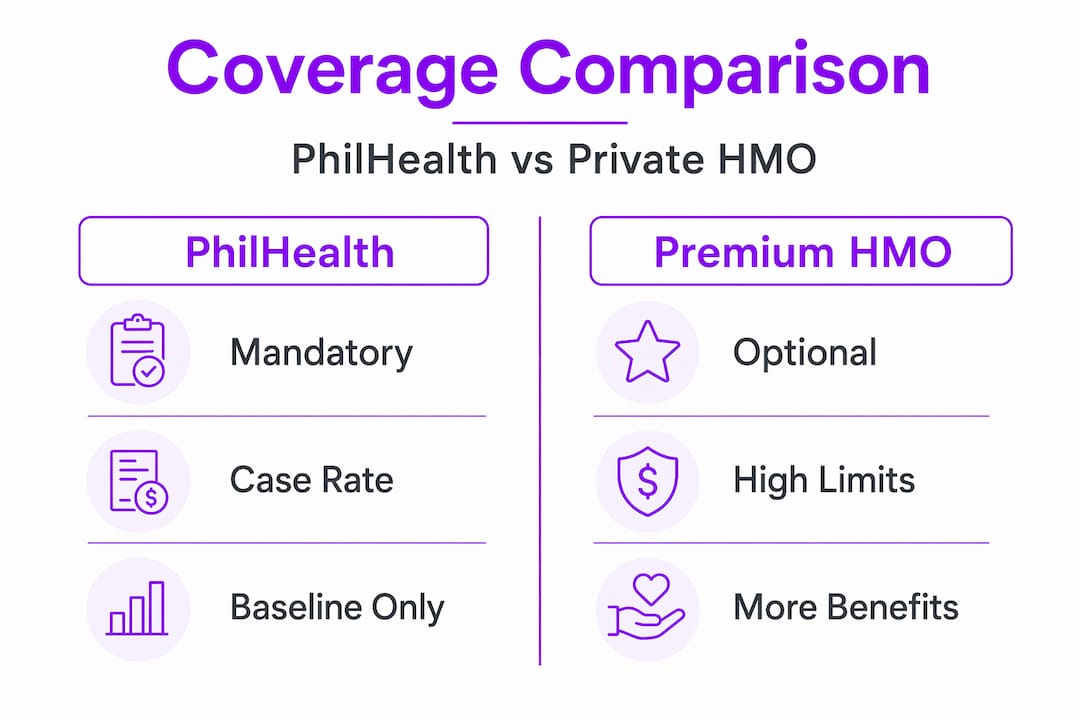

PhilHealth as the mandatory baseline

PhilHealth is the government-provided baseline, funded via mandatory contributions split between employer and employee. As of 2026, the rate sits at 5% of the employee’s basic monthly salary, with a minimum contribution of ₱500 and a ceiling of ₱5,000 per month. Both employer and employee shoulder half of that amount. No matter what other benefits you offer, this contribution is legally required.

PhilHealth covers inpatient hospitalization through a case rate system, meaning it pays a fixed amount per diagnosis rather than a percentage of the actual bill. It also covers certain outpatient services, Z-benefits for catastrophic illnesses, and maternity care. But here is where many SMEs miscalculate: PhilHealth case rates are set by the government and have not always kept pace with the actual costs at private hospitals. A cholecystectomy (gallbladder removal), for example, may have a PhilHealth case rate that covers only a fraction of what a private hospital charges.

| Coverage type | PhilHealth | Basic private HMO | Premium private HMO |

|---|---|---|---|

| Inpatient care | Case rate system | Full room and board up to limit | Higher room and board allowance |

| Outpatient care | Limited | Standard consultations | Specialists, diagnostics, preventive |

| Annual benefit limit | Per case rate | ₱100,000 to ₱200,000 typical | ₱500,000 and above |

| Pre-existing conditions | Generally covered | Waiting periods or exclusions | Varies; some cover up to MBL |

| Hospital access | Accredited gov’t and private | Accredited network | Big hospitals + broader network |

Where private HMOs and insurance enter the picture

Private health plans, whether structured as Health Maintenance Organization (HMO) plans or traditional health insurance, serve as supplemental or standalone premium coverage on top of PhilHealth. An HMO specifically works through a network of accredited hospitals, clinics, and doctors, usually offering cashless access, meaning employees present their HMO card and the provider bills the HMO directly. This eliminates the need to pay out of pocket and file for reimbursement afterward.

For a quick breakdown of how PhilHealth vs HMO SME options differ in real-world scenarios, the distinction often comes down to this: PhilHealth handles the statutory portion, while private HMO or insurance absorbs the balance, the room upgrades, the specialist fees, and the outpatient bills that PhilHealth simply does not cover.

Key differences to keep in mind:

- PhilHealth uses a case rate model; HMOs typically use an annual maximum benefit limit (MBL)

- HMOs provide cashless transactions at accredited facilities; PhilHealth requires reimbursement processes

- Private HMOs offer dedicated account managers and 24/7 assistance lines

- Examples of HMO coverage often include preventive care and wellness programs not available under PhilHealth

“Think of PhilHealth as the floor, not the ceiling. It keeps your employees from hitting zero, but premium coverage is what stops them from falling into financial hardship when a serious illness strikes.”

What makes health coverage ‘premium’? Key features and tiers

Distinguishing PhilHealth from private options raises the question: what qualifies a plan as truly “premium”?

“Premium health coverage” generally refers to higher-tier private HMO or insurance with larger benefit limits and more extensive services than basic plans. But the word “premium” gets misused constantly in marketing materials. Understanding what it actually means in practice will save you from overpaying for something that underdelivers.

The defining features of a premium plan

The most important factor is the annual or maximum benefit limit (MBL). A basic HMO might offer ₱100,000 to ₱200,000 per year. A premium plan typically starts at ₱500,000 and can go well above ₱1,000,000. When an employee requires surgery, extended hospitalization, or cancer treatment, that difference is life-changing.

Beyond the MBL, premium plans offer:

- Private room accommodation in accredited hospitals, not just ward or semi-private

- Specialist access without the need for lengthy referral chains

- Expanded outpatient benefits including diagnostic tests, imaging, and specialist consultations

- Direct hospital admission without pre-authorization delays in emergencies

- Preventive care programs like annual physical exams and health risk assessments

- Access to premier facilities such as the Big 9 Hospitals and Healthway Clinics across the Philippines

| Feature | Basic HMO | Premium HMO |

|---|---|---|

| Annual benefit limit | ₱100,000 to ₱200,000 | ₱500,000 and above |

| Room type | Ward or semi-private | Private room standard |

| Outpatient consultations | General practitioners | Specialists included |

| Hospital network | Regional accredited only | National including top-tier hospitals |

| Emergency coverage | Local network | 24/7 nationwide + out-of-network reimbursement |

| Pre-existing conditions | Often excluded or limited | Can be covered up to MBL with right provider |

Pro Tip: When comparing HMO coverage options, do not just look at the premium price. Calculate the actual out-of-pocket exposure your employees face if the plan’s MBL is too low. A plan that costs ₱500 more per month but provides ₱300,000 additional coverage is almost always the better financial decision.

Why SMEs should care about tiering

For SMEs competing for talent against larger corporations, offering a premium tier signals that the company values employee wellbeing beyond compliance. It is a concrete, visible benefit that candidates notice and remember. When you explore top health insurance providers in the Philippines, you will find that the best plans for SMEs balance cost with meaningful access, not just headline benefit numbers.

Handling pre-existing conditions: What SMEs need to know

One of the most important factors for SMEs in choosing premium health coverage is how pre-existing conditions are handled.

What counts as a pre-existing condition?

A pre-existing condition (PEC) is any illness, injury, or health issue that existed before the policy start date, whether diagnosed or not. Common examples include diabetes, hypertension, asthma, thyroid disorders, and heart conditions. When an employee discloses these at enrollment, the insurer or HMO evaluates how to handle coverage.

For pre-existing conditions, private health and HMO plans often impose waiting periods, exclusions, or partial coverage based on underwriting and the details disclosed. This is the single biggest area where SMEs get surprised after a claim is filed.

The three common approaches insurers use

- Waiting periods: The PEC is covered after a defined period, commonly one year from the policy start date. During this time, claims related to the condition are not processed.

- Benefit caps: The PEC is covered from day one but only up to a sub-limit, for example ₱50,000 per year regardless of the overall MBL.

- Full exclusion: The PEC is permanently excluded from coverage. The employee can claim for everything else but not for that specific condition.

Some HMOs cover PECs only after a year and up to a capped limit, subject to proper disclosure at enrollment. This is why the disclosure process is not just a formality. It directly determines what an employee can and cannot claim.

“A PEC that is not properly disclosed at enrollment may result in a denied claim at the worst possible moment. Always review the PEC schedule in writing before signing any group plan contract.”

What to look for when evaluating PEC policies

- Ask for a written PEC schedule that lists conditions and their treatment under the plan

- Confirm whether waiting periods apply per condition or across the board

- Check if there is a maximum benefit for PECs separate from the overall MBL

- Look for plans that cover PECs up to the full MBL, especially for employees with common chronic conditions

Pro Tip: Review the supplemental health benefits guide for Filipino SMEs to understand how layering PhilHealth with a PEC-friendly premium plan can reduce out-of-pocket exposure for employees with chronic conditions.

How premium plans complement PhilHealth in real-world SME settings

After examining what “premium” means and the importance of handling PECs, let’s see why supplementing PhilHealth with premium plans is becoming standard among SMEs.

Why PhilHealth alone leaves gaps

Employers often add private plans since PhilHealth case rates and outpatient scope may not fully cover real costs, especially in private hospital settings. A single hospitalization for appendicitis in a private Manila hospital can cost ₱80,000 to ₱150,000. PhilHealth’s case rate for appendectomy covers a fraction of that. The balance falls on the employee, which can be financially devastating for middle-income earners.

The gaps show up across multiple scenarios:

- Specialist consultations: PhilHealth rarely covers outpatient specialist visits, and most Filipinos go to specialists for managing chronic conditions

- Diagnostic imaging: MRI scans, CT scans, and specialized blood panels are often only partially reimbursed or not covered at all

- Medicines: Outpatient prescriptions are generally not covered by PhilHealth

- Room and board: The PhilHealth accommodation benefit is minimal compared to private hospital billing rates

Talent attraction and retention as a business case

Skilled employees weigh health benefits carefully when choosing employers. A premium HMO plan, especially one that covers dependents, is one of the top three factors Filipino workers consider alongside salary and job security. SMEs that offer only the statutory minimum find themselves at a disadvantage when recruiting experienced professionals who have enjoyed premium coverage at previous employers.

Employers must still remit PhilHealth contributions correctly even when supplemental health benefits are provided. This is a non-negotiable compliance point. Adding private HMO does not replace PhilHealth; it layers on top of it. Failure to remit PhilHealth contributions on time results in penalties and potential issues with employee benefits eligibility.

Practical steps for offering premium coverage as an SME

- Confirm all employees are registered with PhilHealth and contributions are current

- Decide on the benefit tier based on your workforce’s demographics and typical health risks

- Request a group quote that includes PEC schedules and lists any exclusions in plain language

- Evaluate add-ons: dental, annual physical exams, and life and accident insurance can be bundled for cost efficiency

- Communicate the new benefit clearly so employees understand what is covered and how to use it

Pro Tip: Explore supplemental employee coverage structures that let you layer premium HMO on top of PhilHealth without duplicating costs or creating compliance gaps.

Why redefining “premium” matters for SMEs and what most get wrong

Now, with context and practical options clear, here is an expert perspective on how SME leaders can avoid common mistakes with premium health coverage.

The most persistent mistake we see among SME owners is treating “premium” as a synonym for “expensive.” This misreads the market entirely. A plan with a high monthly premium but a low MBL and a long list of PEC exclusions is not premium coverage. It is an expensive basic plan dressed up in better branding. True premium coverage is defined by what happens when an employee actually needs it, not by what it costs before anyone gets sick.

The cheapest plan on the market often turns out to be the most expensive one. Here is why: when a claim is denied due to an undisclosed PEC, or when an employee exhausts a ₱150,000 benefit limit after just four days in a private hospital, the company absorbs reputational damage and loses employee trust. Some SMEs we have worked with had to pay out-of-pocket to help employees cover hospital bills because their plan was woefully underpowered. That is not a savings strategy. That is deferred spending with interest.

The right approach is to go beyond marketing labels. Always request the actual policy schedule in writing. Ask for real-world examples of what a claim looks like for a common scenario, such as dengue hospitalization or an emergency appendectomy. Find out the exact PEC clause wording, not the sales summary version. And when evaluating alternatives to basic platforms, look specifically at MBL, hospital network quality, and PEC treatment.

There is also a mindset shift worth making. Premium coverage is not a cost center for SMEs. It is a retention tool, a productivity investment, and a risk management strategy all in one. Employees who have access to quality care use it proactively, which means fewer sick days, earlier diagnosis of serious conditions, and lower long-term absenteeism. The ROI on well-structured health coverage is real, even if it does not appear in a single line on your income statement.

Explore premium HMO options for your SME

Having understood the key factors behind premium health coverage, here is how you can take the next step for your business.

At HMO Plans, we work specifically with Philippine SMEs to build group health plans that actually deliver when claims arise. Our plans through Purple Cow and Etiqa offer 100% coverage for pre-existing conditions, congenital conditions, and special procedures, all up to the Maximum Benefit Limit. That means no fine-print surprises when your employee needs care most.

We give you access to premier facilities including the Big 9 Hospitals and Healthway Clinics, cashless transactions, 24/7 nationwide coverage, and a full digital healthcare platform. You can also customize with dental, annual physical exams, and life and accident add-ons. Explore the full range of premium HMO features for SMEs and see how straightforward this process can be. Our team is ready to walk you through a plan that fits your headcount, budget, and workforce needs. Visit our SME member services page to get started today.

Frequently asked questions

Do premium health plans in the Philippines always include coverage for pre-existing conditions?

No, most require a waiting period or set limits for pre-existing conditions. Pre-existing conditions may have waiting periods, caps, or exclusions depending on the specific plan, so always review the policy schedule before signing.

Can an SME offer only private HMO without PhilHealth for employees in the Philippines?

No. Employers are required to remit PhilHealth contributions regardless of any extra private coverage provided, as PhilHealth registration and remittance are mandated by law.

What is the main advantage of premium coverage compared to basic HMO plans?

Premium health coverage features higher benefit limits and broader care access, including private hospital accommodation, specialist consultations, and expanded outpatient benefits not typically found in basic plans.

How are PhilHealth contributions calculated for SME employers in 2026?

PhilHealth rate is 5% of salary, shared equally between employer and employee, with a minimum monthly contribution of ₱500 and a maximum of ₱5,000, regardless of any supplemental health coverage offered.