Nationwide health coverage in the Philippines: A guide for SMEs

TL;DR:

- PhilHealth offers limited coverage with fixed case-rates, often leaving employees to pay the balance.

- Private HMO plans provide customizable coverage, including broader benefits and pre-existing condition options.

- Combining PhilHealth and HMO plans is essential for comprehensive employee health protection and minimized out-of-pocket costs.

Many SME owners assume that once their employees are under the Philippine government’s health program, they are fully protected from major medical bills. That assumption is costly. Nationwide health coverage in the Philippines is built on the National Health Insurance Program (NHIP), commonly known as PhilHealth, under the Universal Health Care (UHC) framework. But “covered” does not mean “fully paid for.” Understanding the actual scope, the real gaps, and the best supplemental strategies is what separates an SME that protects its team from one that leaves employees with surprise hospital bills.

Table of Contents

- What does nationwide health coverage really mean in the Philippines?

- PhilHealth vs private health insurance: Key differences for SMEs

- How pre-existing conditions are handled: PhilHealth vs private plans

- How employers can maximize health coverage for their teams

- Our take: The real-world gap and what smart SMEs do differently

- Need custom health coverage for your team?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| PhilHealth foundations | Nationwide health coverage is primarily delivered through PhilHealth under the Universal Health Care law in the Philippines. |

| Coverage gaps exist | PhilHealth uses case-rate packages, so employees may face significant out-of-pocket costs for care not fully covered. |

| Private plans add value | SMEs can enhance protection for employees by combining PhilHealth with private HMO coverage tailored to their needs. |

| Pre-existing condition rules | Private health plans often limit coverage for pre-existing conditions, so review policy details before enrolling your team. |

| Maximize smartly | Review and customize coverage options each year to ensure your employees are fully protected and your investment counts. |

What does nationwide health coverage really mean in the Philippines?

Building on that reality check, let’s clarify what “nationwide health coverage” truly offers for SMEs and their employees.

The UHC framework was signed into law in 2019 through Republic Act 11223. Its goal is to ensure that every Filipino has access to quality health services without suffering financial hardship. In practice, PhilHealth acts as the country’s social health insurance administrator. All formal employees, including those working in registered SMEs, are automatically enrolled as members. Their dependents, such as spouses and children, are also covered under the same membership.

What PhilHealth covers:

- Inpatient hospitalization via a case-rate system

- Selected outpatient procedures and day surgeries

- Maternity care and newborn packages

- Z-benefit packages for catastrophic illnesses like cancer and end-stage renal disease

- Selected primary care benefits through primary care benefit (PCB) packages

The critical word in that list is “selected.” PhilHealth does not operate like a blanket insurance policy. Instead, it uses a package and case-rate system where a fixed peso amount is assigned per diagnosis or procedure. If a patient is admitted for pneumonia, PhilHealth releases a predetermined benefit amount to the hospital. If the actual bill is higher than that fixed amount, the employee pays the difference out of pocket.

Here is a simplified view of how this works:

| Condition | Estimated hospital bill | PhilHealth case-rate | Potential out-of-pocket cost |

|---|---|---|---|

| Pneumonia (simple) | PHP 25,000 | PHP 15,000 | PHP 10,000 |

| Appendectomy | PHP 60,000 | PHP 22,000 | PHP 38,000 |

| Normal delivery | PHP 18,000 | PHP 8,000 | PHP 10,000 |

| Dengue (moderate) | PHP 35,000 | PHP 16,000 | PHP 19,000 |

These are rough estimates, but the pattern is consistent: the case-rate covers a portion, not the whole bill. This gap is where employees and employers get caught off guard.

For SME owners specifically, understanding this structure matters because it determines how much financial risk your employees actually carry. A workforce that gets sick and faces large out-of-pocket bills is a workforce dealing with financial stress, and that stress affects productivity, morale, and retention.

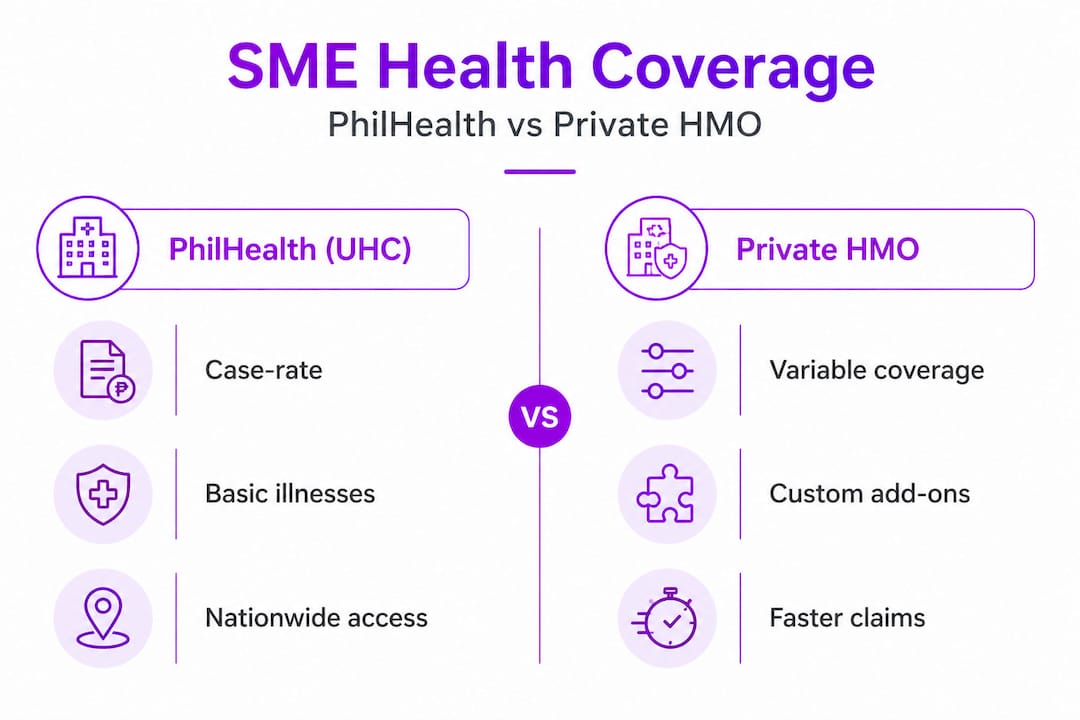

PhilHealth vs private health insurance: Key differences for SMEs

Now that we understand what the standard coverage entails, here is how it measures up against private options that SMEs often consider.

The core distinction between PhilHealth and private health plans is structural. PhilHealth benefits are not identical to private health insurance because PhilHealth uses a package and case-rate system with fixed limits, meaning employees may still pay significant amounts for bills that exceed those rates. Private HMOs, on the other hand, work on a Maximum Benefit Limit (MBL) system where the plan covers costs up to the total limit set for the coverage year.

Here is a side-by-side comparison:

| Feature | PhilHealth (UHC) | Private HMO plan |

|---|---|---|

| Benefit structure | Fixed case-rate per diagnosis | MBL per member per year |

| Cashless access | In accredited public hospitals | In accredited hospitals and clinics |

| Outpatient coverage | Limited | Included in most packages |

| Dental coverage | Not covered | Available as add-on |

| Annual physical exam | Not included | Available as add-on |

| Customization | No | Yes, by group size and industry |

| Dependent flexibility | Yes (automatic) | Configurable |

| Out-of-network options | No | Reimbursement available |

For an SME owner reviewing PhilHealth vs HMO options, the most important column is customization. A private plan can be shaped around your team’s demographics, health risks, and company budget. PhilHealth cannot.

Consider a practical scenario: one of your employees has an emergency appendectomy. The hospital bill comes to PHP 65,000. PhilHealth releases PHP 22,000. Without an HMO top-up, your employee pays PHP 43,000 out of pocket. With a group HMO plan that covers up to PHP 100,000 per year, that remaining balance can be settled cashlessly without the employee touching their savings.

You should also consider supplemental services that private plans cover. For example, physiotherapy coverage in insurance is rarely part of basic government programs but matters significantly for employees recovering from musculoskeletal injuries or post-surgical rehabilitation. Many HMO packages can include this type of care.

Steps to map benefit gaps quickly:

- List the most common health conditions in your industry (e.g., back problems for logistics, stress-related illness for tech).

- Look up the PhilHealth case-rate for each of those conditions.

- Compare that rate to the average market cost from local hospitals.

- The difference is your employees’ out-of-pocket exposure without supplemental coverage.

- Use that exposure number to justify and right-size an HMO plan.

Pro Tip: Run this gap analysis before your next budget cycle. Even a small supplemental HMO plan covering the top five health risks for your team can dramatically reduce financial stress for your employees and reduce absenteeism for your business.

How pre-existing conditions are handled: PhilHealth vs private plans

One key challenge for companies is how employees with pre-existing conditions are treated under each system.

This is where many SME owners get blindsided. PhilHealth, as a government program, does not underwrite coverage the same way private insurers do. There are no medical questionnaires, no contract-based exclusion riders, and no waiting periods applied to specific diagnoses before enrollment. If your employee has hypertension and gets admitted for a related condition, PhilHealth will still apply the relevant case-rate benefit.

Private HMOs and health insurance policies operate very differently. According to Philippine legal commentary on pre-existing conditions, private plans may impose waiting periods or define pre-existing conditions contractually, while PhilHealth coverage is not framed as excluding pre-existing conditions in the same underwriting sense. In plain terms: PhilHealth treats everyone the same, but a private HMO has the right to exclude or limit coverage for conditions that existed before enrollment.

Typical pre-existing condition (PEC) handling in private plans:

- A waiting period of 6 to 12 months before PEC-related claims are accepted

- A contractual exclusion where certain diagnosed conditions are permanently excluded from coverage

- A sub-limit where PEC claims are only covered up to a lower benefit ceiling than the full MBL

- A declarations requirement at enrollment, where undisclosed conditions may later cause claim denials

This is a real risk for SMEs. If you enroll a team of 30 people and several employees have diabetes, hypertension, or a history of asthma, standard private HMO plans may restrict coverage for exactly the conditions those employees are most likely to claim on. That defeats the purpose of offering coverage in the first place.

The good news is that not all private plans work this way. Some providers, including pre-existing condition plans built specifically for SMEs, offer 100% PEC coverage up to the MBL. That means even employees with known conditions can access cashless care without worrying about exclusion riders.

Before enrolling your team in any private plan, you should confirm HMO eligibility for SMEs including how each provider defines and handles pre-existing conditions. Do not assume inclusion. Ask directly, and get the answer in writing.

Pro Tip: Always request the policy schedule (also called the Certificate of Coverage or policy jacket) before signing any group contract. Look specifically for the PEC definition, the waiting period clause, and whether a PEC rider or endorsement is available to waive exclusions.

How employers can maximize health coverage for their teams

With the mechanics explained, here is a practical playbook you can use to boost your employees’ actual health protection.

The most effective SME benefits strategies layer PhilHealth and private HMO coverage together. PhilHealth handles the baseline, and a well-selected HMO plan fills the gaps. Here is a structured approach:

Step-by-step checklist for combining PhilHealth and HMO coverage:

- Confirm that your business is registered with PhilHealth and contributions are up to date for all employees.

- Identify your team’s demographic profile: average age, family status, and industry-specific health risks.

- Request quotes from HMO providers for group plans that match your headcount (most require a minimum of five to ten employees).

- Compare the MBL, cashless network, outpatient benefits, and PEC policies across at least three providers.

- Look for plans that include supplemental PhilHealth coordination so claims are processed in the right order without delays.

- Add optional benefits such as dental, annual physical exams (APE), and life insurance if the budget allows.

- Educate employees on their benefits: what is covered, how to use cashless access, and what requires reimbursement.

As one practical principle states, before enrolling employees in any private plan, you should request the exact policy schedule to check PEC definitions, waiting periods, maximum benefit limits, and claim requirements. This step alone can prevent major disputes down the line.

“The difference between a good health plan and a useless one often comes down to a single page in the policy document: the PEC clause. Read it before you sign.”

Consider a real design scenario. An SME with 20 employees, a mix of young and senior staff, and a tech-sector profile might structure benefits this way:

- Base layer: PhilHealth for all employees (mandatory, funded by shared contributions)

- Core layer: Group HMO plan with PHP 150,000 MBL, cashless access to major hospitals, and full PEC coverage

- Add-on layer: Annual physical exam package for early detection, dental HMO for routine care

- Optional layer: Group life and accident insurance for dependents and trauma coverage

This layered design means a hospitalized employee rarely pays anything out of pocket. And for conditions like hypertension, diabetes, or asthma, the PEC-inclusive plan ensures they are not hit with denials at the worst possible moment.

You can also see how this works in practice by reviewing HMO coverage examples from actual SME scenarios.

Pro Tip: Review your plan’s utilization data annually. If certain benefits are underused, your broker can help you redirect that budget toward riders or limits that actually match what your team needs. Treating benefits as a static enrollment exercise wastes money.

For a more detailed walkthrough, check out this guide on HMO enrollment for SMEs, which covers everything from documentation to onboarding employees into a new plan.

You can also explore specific tactics on optimizing employee benefits to make sure your investment in coverage actually translates into meaningful protection.

Our take: The real-world gap and what smart SMEs do differently

Here is an opinion shaped by years working in the SME employee benefits space in the Philippines.

PhilHealth is not a problem. It is a foundational safety net, and every employer should take their contribution obligations seriously. The problem is when business owners treat PhilHealth as their full benefits solution and stop there. That is where employees get hurt, financially and physically.

The most overlooked risk is not catastrophic illness. It is common hospitalization. Dengue fever. Pneumonia. An infected appendix. These are not rare events. They happen regularly across Filipino workforces, and they generate bills of PHP 30,000 to PHP 80,000 that PhilHealth partially covers. Without an HMO, the employee absorbs that balance. For a rank-and-file worker earning PHP 20,000 a month, a PHP 40,000 out-of-pocket bill is a financial crisis.

What we have seen consistently is that SMEs who treat health coverage as a strategic investment, not a compliance checkbox, retain better talent and have more productive teams. When employees know their health is genuinely covered, including for pre-existing conditions, they focus on their work instead of worrying about what happens if they get sick. That is a real competitive advantage.

The second lesson is about plan review. Most SMEs enroll in a plan once and forget it for three years. Meanwhile, their team grows, employees age, and risk profiles change. The right approach for SMEs is to treat the annual plan review as a strategic session, not just paperwork. Adjust MBLs as salaries grow. Add PEC riders if employees disclose new conditions. Drop underused benefits and reinvest that budget into gaps that matter.

The SMEs that do this well tend to spend no more per head than those who do not. They just spend more intelligently.

Need custom health coverage for your team?

If you want to offer your employees real peace of mind and a genuine hiring advantage, here is where you can start.

At HMO Plans, we work exclusively with SMEs across the Philippines to design group health plans that go beyond PhilHealth. Our plans, underwritten by Etiqa through Purple Cow, include 100% coverage for pre-existing conditions up to the Maximum Benefit Limit, cashless access to the Big 9 Hospitals and Healthway Clinics, and flexible add-ons like dental, annual physical exams, and life insurance. No complicated terms. No hidden exclusion traps. Just straightforward coverage your employees can actually use. Get a custom quote today and find out what comprehensive SME coverage looks like for your team size and budget.

Frequently asked questions

Does PhilHealth cover all medical expenses for employees?

No. PhilHealth applies a fixed amount per condition using a case-rate system with limits, so employees often pay the remaining balance directly to the hospital.

Are pre-existing conditions covered by nationwide health insurance?

PhilHealth does not contractually exclude pre-existing conditions like private insurers do, but most HMO plans may impose waiting periods or exclusions for conditions diagnosed before enrollment.

Can SME owners customize employee health coverage?

Yes. SMEs can layer a private HMO plan on top of PhilHealth to fill coverage gaps, add optional benefits like dental and APE, and adjust the Maximum Benefit Limit based on company budget and team profile.

How do I make sure my employees are protected from gaps in coverage?

Before signing any group contract, request the exact policy schedule and review the PEC definitions, waiting periods, and claim requirements to prevent denied claims later.