Dental insurance for your team: A guide for Philippine SMEs

TL;DR:

- Most HR managers in the Philippines mistakenly believe that PhilHealth adequately covers dental benefits, but it only provides a PHP 1,000 preventive package that barely covers a routine cleaning. To offer meaningful dental coverage, SMEs must layer employer-sponsored HMO plans on top of PhilHealth, clearly defining each benefit’s scope and costs. Effective dental benefits improve employee satisfaction, reduce sick days, and are a crucial part of comprehensive wellness strategies for businesses.

Most HR managers in the Philippines assume PhilHealth handles dental for their teams. It doesn’t, not really. PhilHealth’s dental benefit is capped at a preventive package worth PHP 1,000 per year per employee, which barely covers one routine cleaning. For SMEs building a competitive benefits package, that gap is significant, and closing it requires a clear understanding of how employer-sponsored dental coverage actually works, what options are available, and how to structure a plan your team will genuinely use.

Table of Contents

- Understanding dental coverage: PhilHealth versus employer-sponsored plans

- How SMEs typically structure dental insurance for teams

- Designing an effective dental insurance package for your team

- Why dental benefits matter for your team and your business

- The uncomfortable truth most SMEs miss about dental insurance

- Make your team’s dental benefits work: Next steps with Purple Cow

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| PhilHealth covers basics only | PhilHealth provides limited preventive dental benefits, not full coverage for most team needs. |

| Layered approach works best | Combining PhilHealth with an HMO dental plan maximizes dental coverage for teams. |

| Review contract details | Always clarify limits, waiting periods, and exclusions before finalizing dental insurance for your SME. |

| Dental benefits drive results | Teams with dental coverage see higher utilization, better wellness, and improved job satisfaction. |

Understanding dental coverage: PhilHealth versus employer-sponsored plans

Before you can design better coverage, you need to know exactly what PhilHealth provides and where it stops.

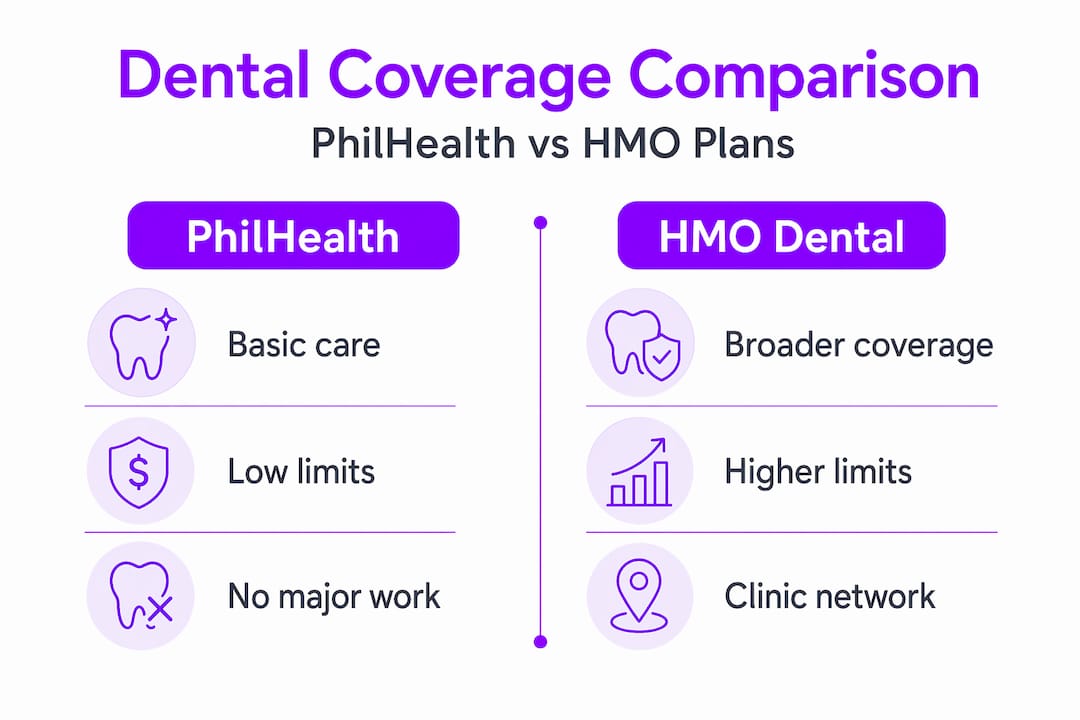

PhilHealth’s preventive oral health package covers a specific list of services each year. According to the Philippine News Agency, this package includes mouth examinations, oral prophylaxis (cleaning), fluoride varnish, pit and fissure sealants, Class V procedures for up to two teeth per year, and emergency tooth extractions, all subject to a maximum payout of PHP 1,000 per patient per year. That is the entire scope of PhilHealth dental coverage for most employees.

The provider access rules matter too. Employees can use public providers without co-payments, but private dentists involve maximum co-payment caps per visit for certain covered services. For employees who rely on private clinics, out-of-pocket costs can mount quickly even within that limited scope.

What PhilHealth dental coverage cannot do for your team:

- Cover restorations like fillings, crowns, or bridges

- Fund orthodontic treatment

- Pay for implants or major oral surgery beyond emergency extractions

- Provide meaningful coverage beyond PHP 1,000 annually per person

- Guarantee private dental access without co-payments

Now compare that to what a dental HMO benefits package for SMEs typically provides:

| Feature | PhilHealth | Employer HMO with dental add-on |

|---|---|---|

| Annual benefit limit | PHP 1,000 | PHP 5,000 to PHP 15,000+ |

| Preventive services | Yes | Yes |

| Basic restorations (fillings) | No | Often included |

| Major services (crowns, bridges) | No | Selected plans |

| Orthodontics | No | Usually excluded |

| Private clinic access | Limited, co-pays apply | Broad network, cashless |

| Emergency extractions | Yes | Yes |

| Out-of-pocket exposure | High | Significantly reduced |

The contrast is stark. For a team of 30 employees, relying only on PhilHealth dental coverage means each person faces nearly all their actual dental costs out of pocket. That is not a dental benefit, it is a symbolic gesture. SMEs that want dental coverage with real impact need to layer employer-sponsored options on top of PhilHealth, not substitute one for the other.

How SMEs typically structure dental insurance for teams

The most practical approach most Philippine SMEs use is called the layering method: combine PhilHealth’s preventive coverage as the base layer, add an employer HMO dental plan as the second layer, and acknowledge that some procedures will still require out-of-pocket payment. The key is knowing exactly what each layer handles.

Here’s how the layered approach works in practice for a typical SME team:

- Employee registers with a PhilHealth-accredited dental provider to use the annual preventive benefit, specifically for cleaning and oral examination.

- Employee accesses the HMO-accredited dental clinic for procedures outside PhilHealth’s scope such as fillings, tooth extractions beyond emergencies, or minor oral surgery.

- Employee pays out of pocket for excluded services like orthodontics, cosmetic work, or treatments above the HMO’s maximum annual dental benefit.

- HR communicates both benefit layers clearly at onboarding and during annual enrollment so employees know which plan to use and when.

- HR tracks utilization patterns annually to evaluate whether benefit caps are realistic for the team’s actual dental needs.

To see how the cost breakdown plays out in practice, here’s a sample scenario for one employee over a year:

| Service | Estimated cost (PHP) | PhilHealth pays | HMO pays | Employee pays |

|---|---|---|---|---|

| Oral examination + cleaning | 800 | Up to 800 | 0 | 0 |

| Filling (2 teeth) | 4,000 | 0 | 3,500 | 500 |

| Tooth extraction | 2,500 | Partial (emergency only) | 2,000 | 500 |

| Dental crown | 12,000 | 0 | 6,000 | 6,000 |

| Orthodontic consultation | 3,000 | 0 | 0 | 3,000 |

For basic to moderate dental care, the layered plan reduces employee out-of-pocket costs considerably. But for major work like crowns or orthodontics, the gap remains real. HR teams should set honest expectations with employees rather than overpromising what the benefits cover.

Pro Tip: During onboarding, give every employee a one-page “dental benefits cheat sheet” that shows which services PhilHealth covers, which their HMO dental coverage for SMEs handles, and which will cost them out of pocket. Eliminating confusion at the start prevents frustration later.

One thing worth noting: most employer dental plans through an HMO also include an accredited network of dental clinics. Confirm that the network has enough clinics near your offices or where your remote employees live. A benefit with no accessible clinic nearby is a benefit your team won’t use. Check the clinic finder through your dental HMO services platform before signing any contract.

Designing an effective dental insurance package for your team

Understanding the structure is one thing. Making smart decisions as an HR manager during plan selection is another. Here is where most SMEs make avoidable mistakes, usually because they accept the first plan offered without reviewing the fine print.

When evaluating SME dental plans, benefit tiers and optional dental features are typically packaged under SME-oriented programs with constraints like minimum number of principals and capped enrollee counts. HR should always verify waiting periods, maximum benefit limits, and exclusions in the actual policy or Health Care Agreement before signing.

Essential questions to ask any dental plan provider before you commit:

- What is the annual maximum dental benefit per employee?

- Is there a waiting period before dental benefits activate, and how long?

- Are pre-existing dental conditions covered or excluded?

- Which specific procedures are excluded from coverage?

- How many accredited dental clinics are within 5 km of your offices?

- Can employees access dental benefits from day one of enrollment?

- Is dental coverage a rider (add-on) or integrated into the main HMO plan?

- What happens if an employee needs a procedure not on the covered list?

Pro Tip: Watch for dental allowance caps that reset annually versus those that accumulate or carry over. A plan with a PHP 7,000 annual cap sounds reasonable, but if it resets every January regardless of what was used, employees who need major work mid-year can hit the cap fast. Ask if there’s a rollover or supplemental allowance option.

Industry insight: Companies that invest in dental benefits see measurable improvements in employee satisfaction scores, particularly among mid-level staff who value practical day-to-day benefits over abstract insurance coverage. Dental is one of the most tangible, frequently used benefits in any health package.

For plan design, think about your team’s demographics too. A younger team might use dental benefits heavily for preventive care and minor work. An older workforce might face higher demand for restorations and major procedures. Review your team’s past claims data if available, or survey employees anonymously about their dental needs before locking in a plan tier. This kind of informed decision-making is exactly what best insurance tips for SMEs consistently recommend.

Also consider how dental benefits interact with your broader health plan structure. Coordinating maximizing healthcare coverage for employees means dental should not be an afterthought bolted onto the main plan. It should be part of a cohesive benefits strategy that employees understand and trust. Review your full benefits architecture at least once a year, using SME health insurance concepts as a reference when evaluating plan language.

Why dental benefits matter for your team and your business

The business case for dental benefits extends beyond keeping teeth healthy. It directly affects your company’s ability to attract and retain good people, and it shows up in productivity and culture too.

Here’s a striking data point: people with dental benefits are 73% more likely to visit the dentist at least once a year compared to those without coverage. That is not a minor difference. Regular dental visits catch oral health problems early, which means fewer emergency situations, fewer unexpected sick days, and fewer costly treatments that could have been prevented.

Direct business benefits of providing dental coverage to your team:

- Fewer sick days tied to dental emergencies like infections, abscesses, or severe pain

- Stronger recruitment appeal especially for candidates comparing offers from multiple employers

- Higher retention rates among staff who feel their health needs are genuinely covered

- Improved team morale from knowing the company invests in everyday wellness, not just hospitalization

- Reduced presenteeism (working while sick or in pain) which hurts productivity more than absenteeism

- Tax-deductible benefit costs that make the investment financially attractive for SMEs

For SMEs competing with larger corporations for talent, employee dental wellness is one of the most cost-effective differentiators available. A robust dental plan costs a fraction of what turnover costs, and employees remember that their company covers their dentist visits far longer than they remember a one-time bonus.

The wellness argument is equally compelling. Oral health is directly linked to systemic conditions like cardiovascular disease, diabetes complications, and respiratory infections. Employees who receive regular dental care are likely to have better overall health outcomes, which reduces claims on the main HMO plan over time. Dental coverage, done right, is preventive healthcare investment.

The uncomfortable truth most SMEs miss about dental insurance

Here is something most articles won’t say directly: adding a “dental” line item to your benefits package does not mean your team has meaningful dental coverage. Not even close.

We see this pattern repeatedly. An SME signs a plan that includes a dental add-on, announces it to employees, and then discovers six months later that the benefit only covers two cleanings per year and one extraction. Staff members who needed fillings, root canals, or crowns found themselves paying out of pocket anyway, and their trust in the benefits package eroded quickly.

The reality is that dental needs often extend well beyond PhilHealth’s preventive scope. Fillings, restorations, orthodontics, and complex treatments require an HMO plan’s full dental benefit scope or a meaningful dental rider, not just a token add-on. When HR teams treat dental as a checkbox rather than a genuine benefit, it does more harm than good.

The lesson here is simple but demanding: review every line of coverage depth before you announce any benefit. Know which procedures are included, what the annual cap covers in realistic terms, and where employees will face out-of-pocket costs. Then communicate that honestly.

Equally critical is ongoing employee education. A benefit no one fully understands is a benefit no one fully uses. Plan a short annual briefing, a FAQ document, and a point of contact for questions. When employees know exactly how their dental coverage works, utilization goes up, satisfaction improves, and the company gets visible ROI from the investment. This is especially important when customizing SME health plans that include multiple add-ons like dental, annual physical exams, and life insurance.

The hard truth is that comprehensive dental coverage for teams is achievable, but only when HR treats it with the same rigor as the main HMO plan. It deserves a real evaluation process, honest communication, and annual review.

Make your team’s dental benefits work: Next steps with Purple Cow

Dental benefits that actually work for your team come down to one thing: clarity before commitment. You now have the framework to evaluate PhilHealth’s limits, structure a layered plan, ask the right contract questions, and make the business case internally.

HMO Plans powered by Purple Cow is built specifically for Philippine SMEs that want straightforward, flexible health coverage without complicated terms. Our SME HMO features include optional dental HMO add-ons that integrate cleanly into your core plan, giving your team cashless access to accredited dental clinics without the guesswork. Whether you’re setting up dental coverage for the first time or upgrading a plan that’s underdelivering, our member dental services team can walk you through your options and help you design a package your employees will actually use. Reach out for a consultation and let’s build a plan that fits your team.

Frequently asked questions

What dental services does PhilHealth actually cover for employees?

PhilHealth covers a preventive oral health package that includes mouth examinations, cleanings, fluoride varnish, sealants, and certain extractions, up to a maximum of PHP 1,000 per employee per year. This package does not cover restorations, orthodontics, or major dental work.

How do I coordinate PhilHealth coverage with an HMO’s dental plan for my team?

Employees use PhilHealth for its annual preventive services, then rely on the HMO plan for broader treatments like fillings or extractions. HR should brief staff at onboarding with a clear explanation of which plan covers which procedures and what remains out of pocket.

What contract points should SMEs look for in dental insurance plans?

Always review waiting periods, maximum benefit limits, annual caps, covered procedure lists, and minimum group size requirements before signing any dental plan. Exclusions buried in the contract are where most surprises happen.

Are there dental treatments that neither PhilHealth nor most HMOs cover?

Yes. Orthodontic treatment, cosmetic procedures, and certain complex restorations often fall outside standard dental coverage under both PhilHealth and typical HMO dental riders. Employees needing these treatments should expect to pay out of pocket or negotiate supplemental coverage.