The essential guide to corporate HMO benefits for Philippine SMEs

TL;DR:

- HMO benefits help SMEs improve employee retention, reduce absenteeism, and attract talent.

- A typical Philippines corporate HMO includes inpatient, outpatient, emergency, preventive care, and optional dental coverage.

- Proper legal compliance and effective communication are essential for maximizing HMO benefits and avoiding penalty risks.

Corporate HMO benefits are no longer a perk reserved for large enterprises with deep pockets. For small and medium enterprises (SMEs) across the Philippines, offering health coverage has become a direct competitive advantage in attracting and keeping skilled workers. HMO benefits improve retention, reduce unplanned absences, and give employees the financial security they need to show up and perform at their best. This guide breaks down everything your HR team needs to know, from plan inclusions and legal compliance to PhilHealth integration and strategic communication, so you can make smarter decisions for your workforce.

Table of Contents

- Why HMO benefits matter for Philippine SMEs

- What does a typical corporate HMO package include?

- Key legal guidelines and compliance: What HR must get right

- Integrating HMO with PhilHealth for maximum value

- A fresh perspective: What most SME HR teams miss about HMO strategies

- Partner with the right HMO: Next steps for Philippine SMEs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| HMO boosts retention | Corporate HMO plans help Philippine SMEs reduce turnover and attract talent. |

| Dependent coverage matters | Including family members boosts satisfaction but requires proper consent and documentation. |

| Legal compliance is critical | Reducing or changing HMO benefits without legal process leads to risks and penalties. |

| Maximize with PhilHealth | Integrate HMO with PhilHealth for layered employee protection and lower costs. |

| Proactive HR practices | Annual reviews, digital enrollment, and transparent communication maximize HMO impact. |

Why HMO benefits matter for Philippine SMEs

Many SME owners still treat health insurance as a “nice to have,” something to revisit once headcount hits 50 or the business hits a certain revenue milestone. That mindset is costly. The reality is that Philippine SME turnover rates sit between 15% and 20% annually, and in sectors like BPO, attrition exceeds 50%. Every time a skilled employee walks out, you’re absorbing recruitment fees, onboarding time, and productivity losses, often running three to six months of that person’s salary.

“HMO is not an expense line. For SMEs competing against bigger employers, it’s one of the most cost-effective tools available to reduce turnover and attract talent.”

Financial wellness programs, which include health coverage as a core pillar, are directly linked to lower attrition. When employees know a medical emergency won’t wipe out their savings, they’re less distracted, more present, and more loyal. This is exactly why SME health benefits in 2026 have become central to workforce strategy rather than an afterthought.

Here are the key advantages that corporate HMO plans deliver for SMEs:

- Higher retention rates. Employees who feel protected stay longer. Health benefits consistently rank among the top three reasons workers choose or leave a job.

- Reduced absenteeism. When employees have easy access to outpatient care, they catch health issues early instead of waiting until they become serious emergencies requiring extended leave.

- Stronger recruitment positioning. Candidates, especially those choosing between a large corporation and an SME, will factor in health coverage heavily when comparing offers.

- Improved productivity. Healthy employees simply perform better. Fewer sick days and lower stress about medical costs translate directly into output quality.

- Employer brand differentiation. In a market where salary differences between employers are sometimes marginal, benefits packages become the deciding factor.

For a deeper look at how HMO insurance for SMEs compares across plan structures and provider options, it’s worth exploring your options thoroughly before selecting a provider. The right plan shapes your entire benefits program going forward.

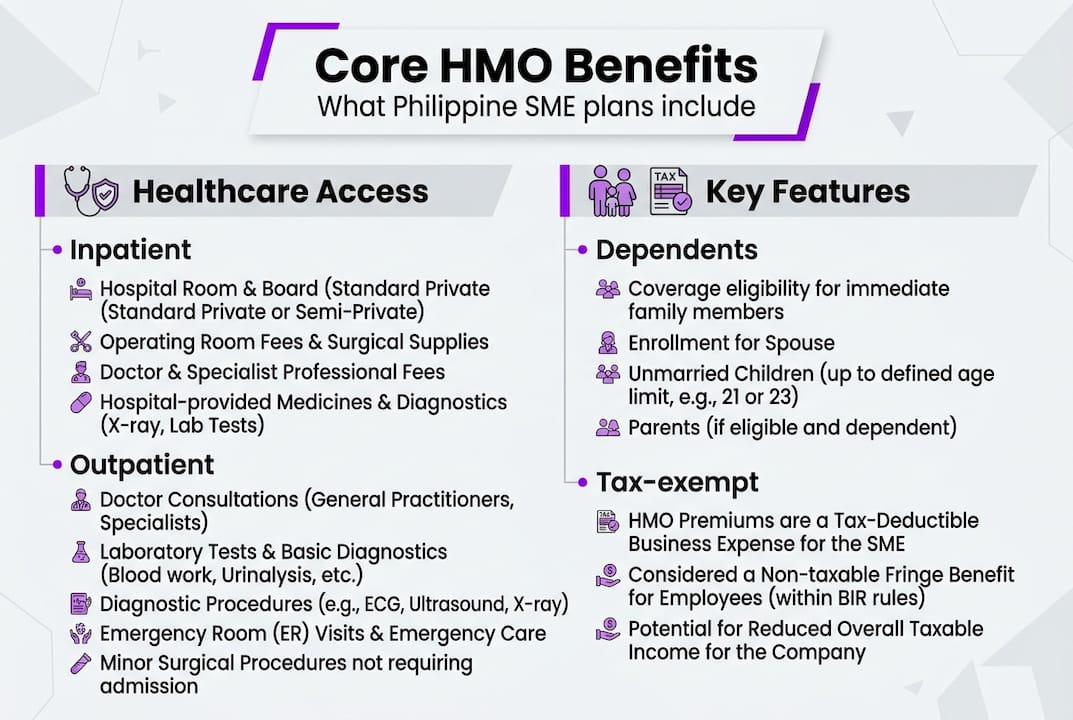

What does a typical corporate HMO package include?

Understanding what’s in a plan is just as important as knowing why you need one. Many HR managers sign contracts without fully grasping what their employees can actually use day to day, and that gap leads to frustration during claims.

Core inclusions in a standard Philippine corporate HMO plan:

| Benefit type | Typical coverage |

|---|---|

| Inpatient care | Room and board, surgeon fees, medicines, lab tests |

| Outpatient care | Consultations, diagnostics, minor procedures |

| Emergency care | ER treatment, stabilization, ambulance in some plans |

| Annual physical exam | Basic labs, chest X-ray, ECG depending on plan tier |

| Preventive care | Vaccinations, wellness consultations |

| Dental (add-on) | Extractions, cleanings, fillings when bundled |

The Maximum Benefit Limit (MBL) is the ceiling amount the HMO will pay per covered member per year. Plans typically range from PHP 100,000 to PHP 200,000 or more depending on the tier. Employees should understand that once the MBL is reached, out-of-pocket expenses begin.

Common exclusions and limitations you must communicate clearly:

- Pre-existing conditions are often excluded or subject to a waiting period ranging from three months to one year

- Congenital conditions may not be covered under standard plans

- Cosmetic procedures, fertility treatments, and elective surgeries are almost universally excluded

- Mental health coverage varies widely and is often limited or absent in basic plans

Pro Tip: Always request the full schedule of benefits and exclusions in writing before finalizing any HMO contract. Review sample corporate HMO coverages from different providers so you can compare apples to apples.

Dependent coverage is another area where HR teams frequently encounter confusion. Dependent coverage typically includes a spouse, children under 21 years old, and in some plans, parents. When employees choose to enroll dependents, the corresponding premium is typically deducted from their salary, and this deduction requires written consent. Failing to secure that consent creates payroll disputes down the line.

Importantly, HMO benefits are tax-exempt for rank-and-file employees when properly structured as part of a company benefits program. This is a meaningful advantage that HR teams should highlight when communicating the value of the benefits package to staff.

Also critical to understand: coverage ends at termination, and premiums are typically non-refundable if stipulated in the policy. Any remaining balance of the annual premium at the time an employee exits may be deducted from final pay, provided this is clearly documented in your employment terms and the HMO agreement. Use our HMO eligibility guide to understand who qualifies for enrollment under different plan structures.

Key legal guidelines and compliance: What HR must get right

Benefits compliance in the Philippines is not optional, and the consequences of getting it wrong can be severe. The most important rule is simple but frequently misunderstood: once you grant HMO benefits to employees, you generally cannot take them away.

Under Labor Code Art. 100, the “non-diminution of benefits” principle applies. This means that if your company has been providing HMO coverage as a company practice, reducing or removing that coverage unilaterally is illegal. Violations expose the company to NLRC (National Labor Relations Commission) complaints and monetary fines. This rule catches many SME owners off guard, particularly those who assumed that since the benefit wasn’t in the employment contract, it could be adjusted freely.

The only legitimate pathways to modifying existing HMO benefits are:

- Mutual agreement documented in writing, ideally through a memorandum of agreement signed by affected employees

- Collective Bargaining Agreement (CBA) negotiations if employees are unionized

- Proof of error showing that the benefit was granted through a clear mistake, not intentional policy, though this is difficult to establish

- Business distress situations where the company can demonstrate financial inability, supported by audited financial statements

Here’s a practical HR compliance checklist to protect your organization:

- Secure written consent from employees for any salary deductions related to dependent HMO enrollment

- Maintain enrollment records for all covered members, including effective dates and benefit levels

- Document all changes to HMO plans with supporting rationale and employee notification

- Schedule an annual review of your HMO contract before renewal to identify any plan changes that could trigger compliance issues

- Align HMO terms with your employee handbook and employment contracts to ensure consistency

- Consult with labor counsel before adjusting any benefit that has been consistently provided for more than one year

“The safest compliance posture for any SME is to treat HMO benefits like wages. Once they’re established, any reduction needs clear legal justification and thorough documentation.”

For a step-by-step walkthrough of enrolling your team, the HMO enrollment steps guide covers the entire process from initial documentation to employee onboarding under a corporate plan.

Integrating HMO with PhilHealth for maximum value

PhilHealth is the mandatory baseline. Every employed Filipino contributes to it, and it covers basic inpatient care, certain surgeries, and selected outpatient services. But PhilHealth’s coverage limits are modest, and for many serious medical conditions, the shortfall between what PhilHealth pays and what hospitals charge is significant.

This is where corporate HMO plans step in to fill the gap. When properly integrated, HMO coverage kicks in to cover what PhilHealth doesn’t, dramatically reducing out-of-pocket costs for employees. In practice, this means employees go to an accredited hospital, PhilHealth covers its applicable portion, and the HMO covers the remainder up to the MBL. The employee often pays very little to nothing.

Here’s how smart PhilHealth and HMO integration works for SMEs:

- Dual-filing claims: Employees submit PhilHealth claims for applicable procedures first, then file for HMO reimbursement for the balance

- Cashless processing: At accredited hospitals, this happens automatically, meaning employees rarely need to pay upfront

- Gap coverage: HMO takes care of room upgrades, specialist fees, and medicines that fall outside PhilHealth’s coverage

- Faster claims processing: Digital HMO platforms allow employees to track and manage claims without waiting in long queues

For SMEs exploring more flexible arrangements, PhilHealth independence options allow companies to structure their HMO plans without PhilHealth dependency under certain conditions. And for a direct comparison of costs and coverage depth, reviewing PhilHealth vs HMO helps HR managers explain the value proposition clearly to employees.

Pro Tip: When evaluating HMO providers, always verify that they are licensed by the Insurance Commission (IC) of the Philippines. IC-licensed HMOs like Maxicare or Medicard maintain strong hospital networks and are held to stricter service standards, which directly affects how smoothly your employees’ claims are processed.

Common integration pitfalls to avoid include failing to inform employees how dual-filing works, which leads to unnecessary out-of-pocket payments that damage trust in the benefits program. Another frequent mistake is choosing an HMO with a limited network that doesn’t include hospitals your employees actually use. Always check network coverage in the specific cities or regions where your team lives and works, not just in Metro Manila.

A fresh perspective: What most SME HR teams miss about HMO strategies

Here’s what separates the SMEs whose HMO programs genuinely retain people from those where the coverage sits unused and unappreciated: communication and administration discipline.

Most HR teams spend months choosing the right plan and almost no time teaching employees how to use it. The HMO card gets issued during onboarding, a pamphlet gets handed over, and that’s it. Six months later, employees still don’t know which hospitals are covered, how to file an outpatient claim, or that their dental add-on even exists. That’s a retention investment that’s not delivering its return.

Digital enrollment and claims portals have changed this equation significantly. Modern HMO platforms allow employees to book teleconsultations, check their MBL balance, find accredited clinics, and submit claims from a smartphone. For HMO for e-commerce teams and other digital-first organizations, this kind of access isn’t a bonus feature, it’s a baseline expectation. HR teams that actively train employees on these digital tools see far higher benefit utilization rates and, as a result, far better retention outcomes.

The second overlooked leverage point is the annual benefits review. Most SMEs sign a contract, auto-renew it every year, and never reassess whether the plan still fits the team. As your workforce grows, ages, or shifts geographically, the right plan changes too. A team that was mostly young and single three years ago might now have several employees with dependents and growing medical needs. An annual review ensures your HMO keeps pace.

Third, and perhaps most underrated, is making HMO benefits visible in retention conversations. During exit interviews, healthcare coverage often emerges as a factor employees considered when deciding whether to leave. If your employees don’t perceive the value of what they’re receiving, the benefit is doing zero retention work even if the coverage is excellent. Mention the benefits package explicitly during onboarding, during annual performance reviews, and in any total compensation discussions. When employees understand what they have, they’re far more likely to factor it into their decision to stay.

Partner with the right HMO: Next steps for Philippine SMEs

Your team’s health coverage should be as thoughtfully chosen as your hiring strategy. If you’re ready to move from generic plans to a solution built for SMEs, you’re in the right place.

At HMO Plans, we work with Philippine SMEs to design coverage that actually fits their teams, not a one-size-fits-all policy built for corporations. Our partnership with Purple Cow and Etiqa means your employees get 100% coverage for pre-existing conditions, congenital conditions, and special procedures up to the MBL, with no complicated fine print. Explore the best HMO plans for SMEs on our website, review our full plan features including dental add-ons and life insurance bundles, and connect with our team through member services for a fast, tailored quote. Smarter coverage starts here.

Frequently asked questions

What makes HMO benefits tax-exempt for employees in the Philippines?

HMO benefits are tax-exempt for rank-and-file employees when the coverage is structured as a formal part of the company’s benefits program rather than as additional compensation. Supervisory and managerial employees may have different tax treatment depending on how benefits are classified.

Can HMO coverage for employees be changed or removed?

Benefits cannot be diminished unilaterally once established as company practice under Labor Code Art. 100. Any reduction requires written mutual agreement, CBA negotiation, or documented proof that the benefit was granted in error.

Who is typically eligible as a dependent under a corporate HMO plan?

Dependent eligibility typically covers a spouse, unmarried children under 21, and in some plans, parents. Any salary deduction for dependent premiums requires the employee’s written consent before processing.

Is a final pay deduction for HMO premiums allowed when an employee leaves?

Yes, final pay deductions for unpaid HMO premiums are lawful when the policy clearly stipulates this and the terms are reflected in the employment agreement. Premiums are generally non-refundable once the coverage period has begun.

What is the key advantage of integrating HMO with PhilHealth for SMEs?

Integration maximizes employee coverage by using PhilHealth as the base layer and HMO as the supplemental tier, significantly reducing out-of-pocket costs and closing gaps that either program alone cannot cover.