Why Choose Tailor-Fit Health Plans for Your Team

TL;DR:

- Customized health plans reduce employee turnover significantly and better address individual healthcare needs. They also ensure compliance with Filipino tax laws while enhancing utilization through digital tools and employee education. Implementing flexible, data-driven, multi-tiered plans helps Philippine SMEs improve employee retention, satisfaction, and financial efficiency.

Standard group health insurance looks good on paper. In practice, it often leaves your employees underprotected, your budget strained, and your HR team fielding complaints. Understanding why choose tailor-fit health plans is not just an academic exercise for Philippine business owners. It is a decision that directly shapes whether your people stay, thrive, and actually use the benefits you are paying for. This article breaks down the real advantages, compliance realities, and practical steps to get customized health coverage working for your business.

Table of Contents

- Key takeaways

- Why choose tailor-fit health plans over standard coverage

- Compliance and operational realities you need to know

- Digital tools and employee education that make plans actually work

- Tailor-fit vs. standard plans: what the comparison actually shows

- How to design and implement a tailor-fit plan for your workforce

- My honest take on tailor-fit plans in the Philippine SME context

- Get a plan that actually fits your team

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Customization drives retention | Tailor-fit plans reduce turnover by nearly 25%, giving you a measurable edge in talent competition. |

| Financial protection matters most | Most Filipino workers cannot absorb a Php 10,000 hospital bill, making benefit design a workforce stability issue. |

| Compliance is non-negotiable | Benefits exceeding de minimis limits create tax exposure; plan design must stay within legal ceilings. |

| Digital tools multiply plan value | Employee confusion about coverage erodes utilization; mobile apps and virtual assistants fix this. |

| One size genuinely fails most teams | Standard plans create coverage gaps and unsustainable premiums that hurt both employees and employers. |

Why choose tailor-fit health plans over standard coverage

The numbers tell a story that should concern every Filipino business owner. Six out of ten Filipino families cannot cover a Php 10,000 hospital bill without borrowing money or relying on an HMO. That is not a fringe scenario. That is the financial reality of most of your employees, and a standard group plan that does not account for this vulnerability is not neutral. It is a liability.

The benefits of custom health plans go well beyond good intentions. Research shows that customizable plans reduce turnover by nearly 25% and that 46% of job seekers rank health benefits above salary when evaluating employers. If your current plan does not let employees adjust coverage to their life stage, family size, or medical history, you are losing ground to competitors who do.

Here is what tailor-fit coverage actually delivers:

- Predictable costs for employees. A striking 72% of employees prefer higher premiums if it means lower, predictable out-of-pocket expenses. Tailor-made health insurance options let you align the cost structure to what your team actually values.

- Life-stage flexibility. A 28-year-old single employee has different health priorities than a 45-year-old parent of three. Customized health programs give each group coverage that feels relevant, not generic.

- Financial risk protection for both sides. When benefit limits match actual medical needs, employees avoid catastrophic out-of-pocket expenses and employers avoid the productivity drain that follows a health crisis. Exploring HMO plans for SMEs shows how these protections translate into real numbers.

- Stronger engagement and productivity. A well-designed HMO package improves employee engagement by making healthcare accessible and financially manageable, two things standard plans frequently fail to deliver together.

Pro Tip: Before selecting any plan, survey your employees on their top three health concerns. The answers will almost always reveal that a single standard plan cannot satisfy even half the room.

Compliance and operational realities you need to know

Customization does not mean anything goes. Philippine tax law draws clear lines around employee benefits, and crossing them creates real liability. The good news is that staying compliant and maximizing benefit value are not mutually exclusive. They just require intentional design.

Here is the compliance framework you need to work within:

- Understand de minimis benefit ceilings. Medical cash allowance to dependents is tax-exempt up to Php 2,000 per semester per employee. Amounts above this ceiling are taxable compensation, which changes both your payroll obligation and the employee’s take-home math.

- Watch the Php 90,000 annual benefit cap. Payroll tax compliance requires careful structuring of total benefit amounts against this ceiling. Exceeding it without proper documentation triggers withholding tax issues.

- Involve your payroll team early. This is not an HR decision in isolation. When benefit design crosses into taxable territory, payroll needs to adjust withholding calculations before the plan launches, not after.

- Get a tax advisor to review the plan structure. Managers frequently underestimate the compliance risk when benefits exceed de minimis limits. A single review session with a qualified advisor can prevent months of correction work.

- Avoid substituting cash for structured benefits. Cash allowances feel flexible but are harder to protect from taxation and easier to miscategorize. Structured HMO benefits stay cleaner from a compliance standpoint.

The advantages of personalized health coverage only hold up when the plan is legally sound. A tailor-fit plan designed without compliance guardrails is not customization. It is a deferred tax problem.

Pro Tip: When structuring any supplemental health benefit, document the business purpose explicitly in your HR policy. This creates a compliance paper trail that protects both the company and the employee during a tax audit.

Digital tools and employee education that make plans actually work

You can design the best tailor-fit health plan in your industry and still watch it underperform. The reason is almost always the same: employees do not understand their coverage, so they do not use it.

56% of employees are dissatisfied when insurance information is hard to understand. More than half of your team may be frustrated with a benefit you are paying for, simply because no one made it navigable. That is a solvable problem, and the tools to solve it are better than ever.

What actually improves employee navigation and utilization:

- Mobile apps with benefit summaries. Employees should be able to check their coverage, find accredited hospitals, and submit claims from their phone. If they have to call HR for basic questions, the plan is already failing the usability test.

- Virtual assistants and 24/7 chat support. Digital assistance tools reduce confusion and help employees take confident next steps when they need care. This directly reduces benefit churn and improves plan satisfaction scores.

- Clear, jargon-free benefit summaries. Every employee should receive a one-page summary in plain language explaining what is covered, what requires pre-authorization, and where to go for emergencies. Not the full policy document. A readable summary.

- Ongoing education beyond open enrollment. Most companies educate employees once a year and call it done. Monthly benefit reminders, short video explainers, and manager talking points keep utilization high throughout the year.

The importance of tailored health solutions extends to the communication layer. A plan that is technically customized but experientially confusing defeats its own purpose. Pair your benefit design with the education infrastructure to make it real for your team. For a practical look at how to optimize healthcare workflows in your organization, the operational side of digital health support is worth exploring.

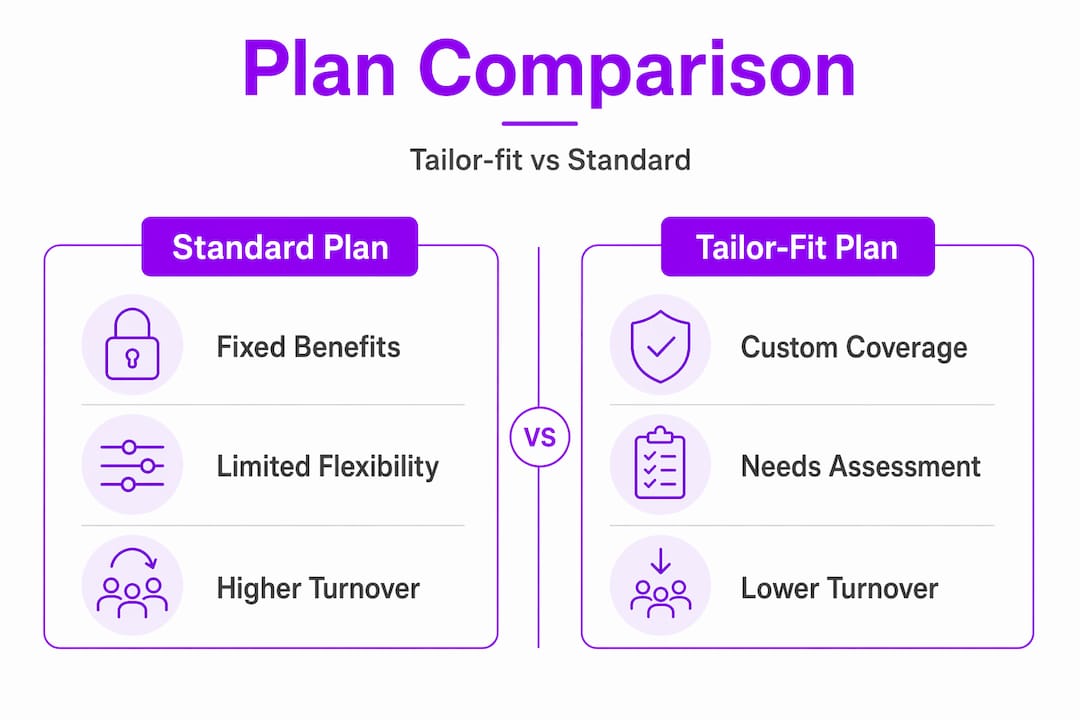

Tailor-fit vs. standard plans: what the comparison actually shows

The difference between a tailor-fit plan and a standard group plan is not just philosophical. It shows up in measurable outcomes across cost, coverage quality, and employee experience.

A one-size-fits-all approach creates coverage gaps and generates premiums that are hard to sustain because the plan is trying to serve everyone and ends up fully serving no one. Here is how the two models compare side by side:

| Feature | Standard group plan | Tailor-fit health plan |

|---|---|---|

| Coverage flexibility | Fixed for all employees | Adjustable by employee tier or need |

| Pre-existing conditions | Often excluded or limited | Can include 100% coverage up to MBL |

| Cost-sharing structure | Uniform co-pays and deductibles | Configurable based on employee preference |

| Dental and wellness add-ons | Rarely included | Optional and stackable |

| Generational relevance | Low for mixed-age workforce | High, with life-stage appropriate options |

| Compliance alignment | Standardized, may not optimize tax efficiency | Structured for de minimis and payroll compliance |

| Employee satisfaction | Moderate at best | Significantly higher with proper design |

The financial efficiency angle is also worth noting. Employers who structure benefits correctly through health reimbursement models can save 7.65% on payroll taxes, and employees may save 20 to 40% on income taxes depending on how the plan is structured. Tailor-made health insurance options are not just better coverage. They are smarter financial planning. You can go deeper on the cost optimization side if the financial case matters to your budget planning.

How to design and implement a tailor-fit plan for your workforce

Knowing why personalized health plans matter is one thing. Building one that works for your specific team is another. Here is a practical sequence that works in the Philippine SME context:

- Survey your employees before you design anything. Ask about current pain points, preferred hospitals, family coverage needs, and whether they prioritize low premiums or low out-of-pocket costs. This data shapes everything that follows.

- Offer at least two plan tiers. Multiple tiers with aligned cost-sharing prevent dissatisfaction across employee segments. A base tier and a premium tier with optional dental and annual physical exam add-ons cover most workforce profiles.

- Use claims data to drive decisions. Effective plan customization requires data-driven engineering built around actual utilization patterns, not assumptions. If you are renewing a plan, pull the prior year’s claims data and redesign around it.

- Partner with a provider that understands SME needs. Not every HMO is equipped to handle the flexibility and compliance nuances that small and medium businesses need. Your provider should offer configurability, not just a product catalog.

- Measure utilization, not just enrollment. A high enrollment rate with low utilization signals an education or access problem. Track claims frequency, digital platform logins, and employee satisfaction scores quarterly.

Pro Tip: Send a short benefit usage email to all employees in the third month after enrollment. Include a reminder of covered services, a link to the digital portal, and one specific benefit they may not know they have. Utilization typically spikes after this touchpoint.

For a fuller view of healthcare best practices for SMEs, the resources are worth bookmarking as you build your plan design process.

My honest take on tailor-fit plans in the Philippine SME context

I have worked with enough Filipino SMEs to say this plainly: the standard group plan is a relic. It was designed for a workforce that was more homogeneous, less mobile, and far less informed about benefits than today’s employees. Sticking with it in 2026 is not playing it safe. It is falling behind.

That said, I have also seen tailor-fit plans fail. Not because the coverage was wrong, but because no one invested in helping employees understand or use it. The compliance piece is equally underappreciated. I have watched HR managers enthusiastically design supplemental cash benefits that looked great on the offer letter and created a payroll tax mess six months later.

My take is this: the importance of tailored health solutions is real, but it only delivers if you treat plan design as an ongoing process, not a one-time decision. Review utilization data. Talk to your employees. Adjust. And when you are not sure about the compliance boundaries, get a tax professional in the room before the plan launches. The upside of getting this right is significant. The cost of getting it wrong compounds quietly until it is not quiet anymore.

— Eumir

Get a plan that actually fits your team

If you are ready to move beyond standard coverage, Hmoplans’ Purple Cow HMO plans are built specifically for Philippine SMEs that want flexibility without the fine print. Purple Cow covers pre-existing conditions, congenital conditions, and special procedures at 100% up to the Maximum Benefit Limit, with optional add-ons for dental, annual physical exams, and life insurance. The platform is digital-first, compliance-conscious, and designed to scale with your workforce. Explore the full Purple Cow plan features to see how customization works in practice, or review the member services options to understand the support your team will have from day one.

FAQ

Why do tailor-fit health plans reduce employee turnover?

Customizable health plans reduce turnover by nearly 25% because employees feel their specific needs are recognized and covered. When health benefits align with personal priorities, people are significantly less motivated to look elsewhere for work.

What is the tax ceiling for employee health benefits in the Philippines?

Medical cash allowances to employee dependents are tax-exempt up to Php 2,000 per semester, and total non-taxable benefits must stay within the Php 90,000 annual cap. Exceeding these limits creates taxable compensation that requires payroll adjustment.

How do digital tools improve tailor-fit health plan outcomes?

Mobile apps and virtual assistants reduce the confusion that leads 56% of employees to express dissatisfaction with their benefits. Better navigation directly increases utilization, which is the clearest measure of whether a health plan is actually working.

When does a tailor-fit plan make more financial sense than a standard plan?

Tailor-fit plans show the most financial advantage for mixed-age or mixed-family-status workforces where a single plan design leaves significant groups underserved. Properly structured plans can also generate payroll tax savings of 7.65% for employers and 20 to 40% income tax savings for employees.

How many tiers should a customized employee health plan include?

Most Philippine SMEs find that two tiers work well: a base plan covering core HMO benefits and a premium tier with add-ons like dental and annual physical exams. Offering more than three tiers typically creates decision fatigue without proportional improvement in satisfaction.