How to enroll your SME in health insurance: A step-by-step guide

TL;DR:

- Many SME owners in the Philippines discover health insurance compliance issues only after facing penalties, audits, or employee health crises.

- Meeting PhilHealth’s legal requirements and supplementing with private HMO plans ensures comprehensive protection, attracting and retaining staff.

- Regular verification of enrollment, remittances, and coverage helps SMEs avoid costly penalties and improves overall business resilience.

Many SME owners in the Philippines discover gaps in their health insurance compliance only after something goes wrong — an audit, a sick employee, or a penalty notice. Getting it right from the start protects your business, your people, and your bottom line. This guide walks you through everything: your legal obligations, the documents you need, the exact PhilHealth enrollment steps, how to add private HMO coverage, and how to verify that your business is fully compliant before problems surface.

Table of Contents

- Understanding SME health insurance obligations in the Philippines

- What you need before enrolling employees

- Step-by-step process: PhilHealth SME enrollment

- Enrolling in private HMO plans: Going beyond the minimum

- Verifying compliance and avoiding penalties

- Why investing in both PhilHealth and HMO is smart risk management for SMEs

- Ready to streamline your SME health insurance enrollment?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Mandatory coverage | All SMEs must register employees for PhilHealth within 30 days of operations or hiring. |

| Supplement with HMO | Private HMO plans are not required but highly recommended to cover gaps in PhilHealth coverage. |

| Stay compliant | Accurate and timely remittance of contributions avoids steep penalties and legal issues. |

| Verify enrollment | Regularly check EPRS status and HMO confirmations to ensure all employees are covered. |

| Plan ahead for edge cases | Part-time staff and freelancers have special rules—review requirements before hiring. |

Understanding SME health insurance obligations in the Philippines

Let’s start by clarifying what you legally must provide versus what’s recommended for comprehensive employee health protection.

Many business owners treat health insurance as optional or something to figure out later. That mindset is costly. In the Philippines, PhilHealth is mandatory basic health insurance for all employees, including those in small and medium enterprises. Enrolling your staff is not a benefit you offer — it’s a legal obligation from the day you hire your first employee.

But PhilHealth alone isn’t enough for real health protection. Think of it as a foundation, not a complete house. PhilHealth vs HMO differences matter because HMO plans cover outpatient visits, specialist consultations, dental care, and emergency services at a much broader range of facilities than PhilHealth typically allows. Many employees face significant out-of-pocket costs for routine care even when their employer is fully PhilHealth-compliant.

Here’s a quick look at what each type covers:

PhilHealth: Government-mandated, covers basic inpatient care, some outpatient procedures, and maternity benefits. Contribution amounts are fixed by law.

Private HMO: Voluntary but strongly recommended. Covers outpatient, inpatient, emergency, specialist, and sometimes dental care. Provider networks are typically wider. Supplemental HMO coverage fills the gaps PhilHealth leaves open.

The stakes for non-compliance are serious. Penalties for non-registration include a 2% monthly interest charge on unpaid contributions, fines ranging from P500 to P100,000 per violation, and possible imprisonment of six months to six years for employers who willfully fail to comply.

Key takeaway: Health insurance compliance is both a legal floor and a strategic ceiling. Meeting the minimum keeps you legal. Going beyond it helps you attract and keep good people.

Beyond compliance, offering comprehensive health coverage tells employees that your company is stable and invested in their wellbeing. In competitive hiring markets, that message matters more than a title or a slight salary bump.

What you need before enrolling employees

With the legal context clear, gather all documents and system access you’ll need for a smooth enrollment process.

Before you log in to any government portal or fill out a single form, you need to assemble the right materials. Missing even one piece of information can stall the entire process, sometimes for weeks.

Documents and information you’ll need:

- Business registration documents (DTI or SEC registration, BIR Certificate of Registration)

- Employer Information: legal business name, address, contact details, and authorized signatory

- Employee list: full legal names, birthdates, and TIN numbers

- Employee salary data (needed to calculate contribution amounts)

- PhilHealth Employer Number (PEN) — if you don’t have one yet, this is your first task

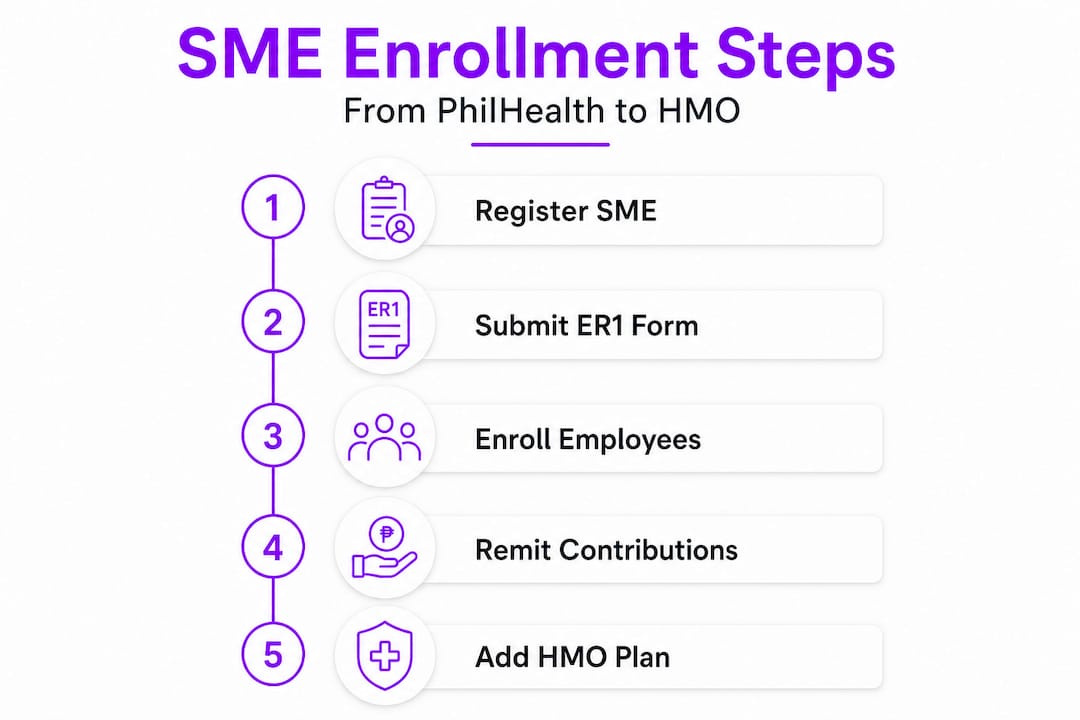

You cannot proceed without a PEN. SME employers must register as PhilHealth employers using the ER1 form within 30 days of starting operations or hiring their first employee. Submit the ER1 to the nearest PhilHealth branch or through the online portal.

Here’s a simple reference table for what’s needed at each stage:

| Stage | Document or Info Required |

|---|---|

| Employer registration | ER1 form, business registration docs |

| Employee reporting | ER2 form, employee full names and PINs |

| New employee without PIN | PMRF (PhilHealth Member Registration Form) |

| Contribution remittance | EPRS access, SPA (Statement of Premium Account) |

| HMO enrollment | Company profile, employee census, salary data |

Part-time employees are a common sticking point. Part-time employees must be registered from day one, even if they work just a few hours a week. There is no minimum hours threshold that exempts an employee from PhilHealth registration. Freelancers, however, must enroll themselves as voluntary members since they are not covered under employer-based registration.

Pro Tip: Create a standard onboarding checklist that includes PhilHealth PIN verification on the employee’s first day. This prevents the common situation where months pass before you realize a new hire was never properly registered.

When preparing for a private HMO plan, requirements vary by provider but typically include a complete employee census (name, age, gender, salary band), your preferred coverage tier, and sometimes a brief company profile. Check out HMO health insurance needs for an SME-specific breakdown of what to expect.

Step-by-step process: PhilHealth SME enrollment

Once you’re prepared, here’s how to complete each step of SME health insurance enrollment through PhilHealth.

Follow these steps in order. Skipping ahead often creates problems that are harder to fix than simply doing things right the first time.

-

Register your business as a PhilHealth employer. Submit the ER1 form either at a PhilHealth branch or online. You’ll receive your PEN, which is the key to everything that follows. Do this within 30 days of hiring your first employee.

-

Report all employees using the ER2 form. The ER2 is the employer’s report of employees. After employer registration, use the ER2 form to report each employee, along with their PhilHealth Identification Number (PIN). For new employees who don’t yet have a PIN, they must complete a PMRF so PhilHealth can generate one.

-

Set up your EPRS account. The Electronic Premium Remittance System (EPRS) is how you remit contributions online. Register for EPRS using your PEN and a POAF (PhilHealth Online Access Form). Once registered, you generate an SPA (Statement of Premium Account) before payment is due.

-

Calculate contributions correctly. Contributions are shared 50/50 between employer and employee, based on monthly salary. The current contribution rate is 5% of the monthly basic salary, with a ceiling and floor set by PhilHealth. Both the employer and employee each pay 2.5%.

-

Remit payments by the 10th. Premium contributions must be remitted by the 10th day of the following month for employers with a PEN ending in 0-4, or by the 15th for those ending in 5-9 (check current PhilHealth guidelines as these dates can shift). You can pay via accredited banks, payment centers, or online through your EPRS dashboard.

Here’s a quick comparison to help you understand what happens when you follow the process versus when you don’t:

| Action | When done correctly | When skipped or delayed |

|---|---|---|

| ER1 submission | PEN issued, enrollment begins | Cannot register employees legally |

| ER2 and PMRF filing | Employees properly on record | Benefits denied when employees need care |

| Monthly SPA generation | Clean contribution record | Penalties and interest accumulate |

| EPRS remittance | Compliance maintained | Fines, possible audit, legal liability |

Important: Check your HMO eligibility for SMEs early in the process, because some private HMO providers require PhilHealth enrollment as a prerequisite or factor it into their pricing models.

Pro Tip: Set a recurring calendar reminder on the 5th of every month to generate your SPA and confirm the payment amount before the deadline. A five-minute task done consistently prevents a much bigger headache later. Also check comprehensive HMO benefits to understand how your private coverage can align with what PhilHealth already provides.

Enrolling in private HMO plans: Going beyond the minimum

With PhilHealth in place, SMEs can maximize employee protection and retention by enrolling in private HMO plans — here’s how to do so and what to consider.

PhilHealth handles the basics. But “basic” has real limits. If your employee needs a specialist consultation, an MRI, or a routine annual checkup, PhilHealth often covers little to nothing for those services. That’s where private HMO plans step in.

For comprehensive coverage beyond PhilHealth, SMEs can enroll in private HMO plans on a fully voluntary basis. There’s no government-mandated enrollment process for HMOs, which means each provider has its own workflow. But the general process typically looks like this:

- Step 1: Request a proposal from one or more HMO providers. Provide your company size, employee demographics, and budget range.

- Step 2: Submit a company and employee census (names, ages, genders, employment status, and sometimes salaries).

- Step 3: Review coverage options. Evaluate provider networks, annual limits, covered services, exclusions, and add-ons.

- Step 4: Finalize the service agreement and pay the premium. HMOs usually bill annually for groups.

- Step 5: Employees receive HMO cards and can begin accessing covered services.

When comparing HMO providers, look beyond the monthly or annual price. Here’s what actually matters:

- Network size: Can your employees access a clinic or hospital near their home or workplace? Does the network include the Big 9 Hospitals?

- Coverage scope: Is outpatient included? Are pre-existing conditions covered? What’s the annual benefit limit per member?

- Exclusions and limitations: Some plans quietly exclude common conditions. Make sure you understand what won’t be covered before you sign.

- Claims process: Is it cashless at most facilities, or does your employee need to pay upfront and wait for reimbursement?

- Add-ons available: Dental, annual physical exams, and life and accident insurance can all be layered on for additional value.

Pro Tip: When reviewing how HMO plans bolster SME benefits, pay attention to whether the plan covers pre-existing conditions from day one. Some plans impose waiting periods of up to 12 months, which leaves new employees exposed exactly when they may need care most.

The business case for strong HMO coverage goes beyond employee health. Studies on employee engagement consistently show that health benefits rank among the top factors in job acceptance and retention decisions. Companies that offer top tips for choosing HMO plans aligned with their workforce needs see measurably lower turnover. For SMEs where losing one key person can disrupt an entire team, that matters enormously. Look into flexible HMO plans that can scale as your team grows.

Verifying compliance and avoiding penalties

The final step is to verify compliance — checking that you’ve hit every legal mark and can prove coverage for every employee.

Many SMEs complete the enrollment process and never look back. That’s a mistake. Compliance isn’t a one-time event; it’s an ongoing practice. Errors in employee data, missed remittances, or system issues can quietly create liability long after enrollment.

Here’s your compliance verification checklist:

- Log in to EPRS and confirm payment history for the current and past three months

- Cross-check the employee list in EPRS against your current HR records

- Verify that every employee’s full name, PIN, and salary grade are correct in the system

- Confirm new hires were added within the required timeframe

- For HMOs, request updated member IDs and confirm all employees are active in the system

Online systems like EPRS for employers streamline compliance tracking, but they require accurate data to function properly. A common mistake is letting employee records fall out of sync — for example, a promoted employee whose salary bracket wasn’t updated, leading to underpayment of contributions.

Compliance reminder: Late remittance penalties include a 2% monthly interest charge, fines of P500 to P100,000 per violation, and for willful non-compliance, possible imprisonment of six months to six years. These are not abstract risks — PhilHealth actively audits employers.

For HMO plans, ask your provider for a formal confirmation of enrollment and keep a copy in your HR files. Review your HMO coverage annually before renewal to check whether your employee count, salary bands, or coverage needs have changed. Don’t wait for the renewal letter — be proactive.

Why investing in both PhilHealth and HMO is smart risk management for SMEs

Here’s the part most articles on this topic skip entirely: compliance is not strategy.

Meeting PhilHealth requirements keeps you out of trouble. It does not make you a competitive employer. It does not protect your employees from major medical expenses. And it certainly doesn’t prevent the business disruption that follows when a key employee faces a serious illness with no real coverage.

The SMEs we’ve worked with across tech, hospitality, and healthcare share a common story: they initially enrolled in PhilHealth to stay compliant, then added HMO coverage after a painful incident. A hospitalized employee couldn’t cover their ICU bill. A department head resigned for a competitor who offered better benefits. A labor complaint surfaced over an employee who never received proper coverage. These stories are avoidable.

HMO benefits for SMEs aren’t just about healthcare access. They’re about risk management. When an employee faces a P200,000 surgery, PhilHealth might cover P20,000. The HMO covers the rest. That gap, left unaddressed, often falls on the employee personally or triggers financial hardship that affects their performance and loyalty. Some employees quietly leave rather than admit they can’t afford healthcare under their current plan.

Our opinion, built on real client experience, is this: the cost difference between basic PhilHealth compliance and a solid HMO plan for a small team is rarely as large as owners expect. The cost of not having it — in turnover, morale, legal exposure, and reputation — almost always ends up higher. SMEs that position themselves as employers who genuinely care about their people’s health attract better candidates and retain them longer. That’s not idealism. It’s practical business math.

Ready to streamline your SME health insurance enrollment?

Enrolling your team in the right health coverage doesn’t have to feel overwhelming. The steps are clear, the rules are knowable, and the right partner makes all of it manageable.

HMO Plans, powered by Purple Cow and underwritten by Etiqa, specializes in exactly this: giving Philippine SMEs access to HMO plan features that go beyond the basics, including 100% coverage for pre-existing conditions up to the Maximum Benefit Limit, cashless access to the Big 9 Hospitals, and flexible add-ons like dental and annual physical exams. Our team handles the complexity so you don’t have to. Explore member services tailored for SME teams, or compare top HMO plans to find the right fit for your business today.

Frequently asked questions

What is the difference between PhilHealth and HMO for Philippine SMEs?

PhilHealth is mandatory government health insurance, while HMOs offer private, broader coverage including outpatient care, specialist visits, and access to wider hospital networks.

When must an SME register with PhilHealth?

SME employers must register using the ER1 form within 30 days of starting business operations or hiring their first employee, whichever comes first.

What are the penalties for failing to register or remit PhilHealth contributions?

Penalties include 2% monthly interest, fines from P500 to P100,000 per violation, and possible imprisonment ranging from six months to six years for willful non-compliance.

Are SMEs required to provide HMO coverage in the Philippines?

No, private HMO enrollment is voluntary but strongly recommended to supplement PhilHealth’s limited coverage, especially for outpatient and specialist care.

How do I check if an employee is successfully enrolled in PhilHealth?

Log in to your EPRS dashboard to verify payment history and confirm that the employee’s records are active and accurate in the system.